From Westpac’s fantastic Red Book of consumer attitudes:

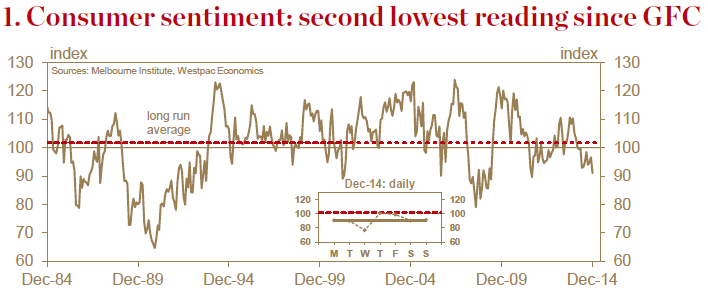

― The Westpac–Melbourne Institute Index of Consumer Sentiment fell 5.7% in Dec from96.6 in Nov to 91.1. The fall takes the Index to its lowest level since Aug 2011 when it briefly slipped below 90, and prior to that, since the tail-end of the GFC.

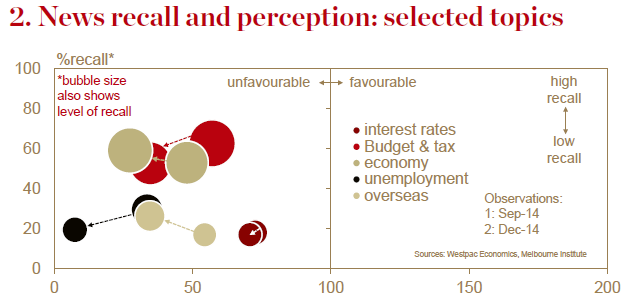

― Daily responses indicate the surprisingly weak Q3 national accounts was the main negative infl uence in the month. However, disillusionment about the Budget and a continued sharp slide in Australia’s commodity prices and the AUD would also have weighed on sentiment.

― These themes were apparent in responses to additional questions on news recall, which showed very high recall on these topics which were viewed as overwhelmingly unfavourable.

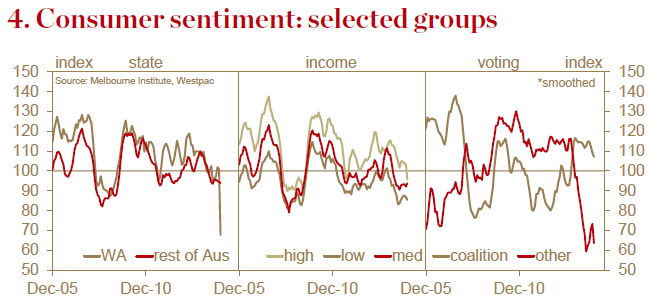

― The survey detail showed sharp declines in consumers’ near term expectations for the economy, their own family finances and assessments of ‘time to buy’. Consumers in WA reported a particularly spectacular sentiment plunge.

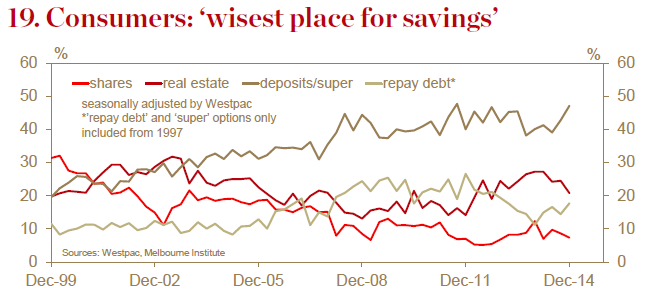

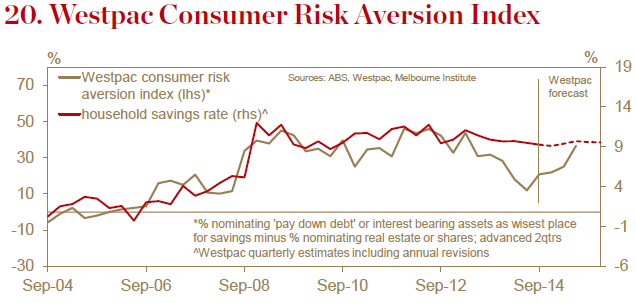

― Updates on the ‘wisest place for savings’ question show how a significant further shift back towards risk aversion with 64.8% nominate ‘deposits/super’ or ‘pay down debt’ vs 51.3% this time last year. The mix resulted in an 11.5ppt rise in the Westpac Risk Aversion Index – our measure that combines these responses into a single gauge of risk aversion – taking it to the highest level since Mar 2013.

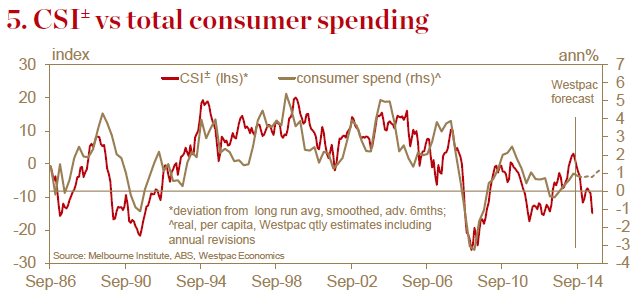

― CSI±, our modified sentiment indicator that we favour as a guide to actual spending, also fell heavily in Dec, down 5.6%. Current levels of the CSI± point to per capita spending falling at –1%yr, implying growth of just over 0.5%yr in aggregate consumer spending.

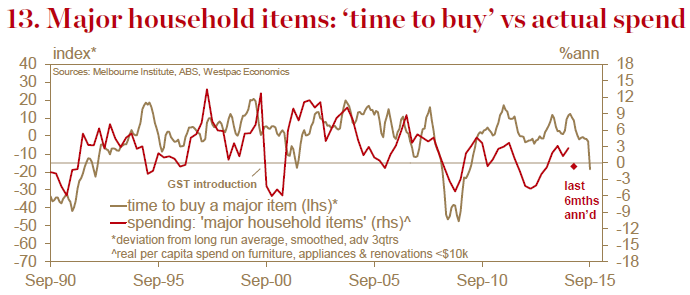

― The sub-index on ‘time to buy a major item’ fell steeply, down 11.8% to be well below its long run average. The fall is disturbing given that this component is typically quite stable and has a close link with actual spending. That said, the Dec decline may be partly due to the falling AUD rather than a sharp shift in buyer attitudes.

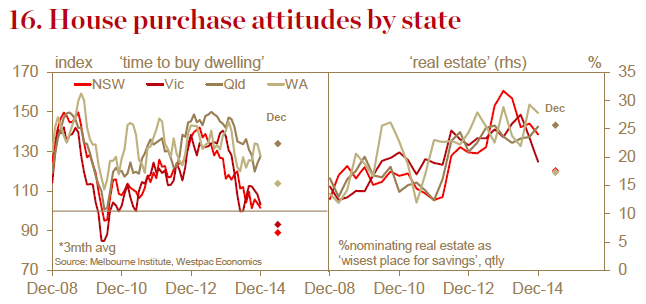

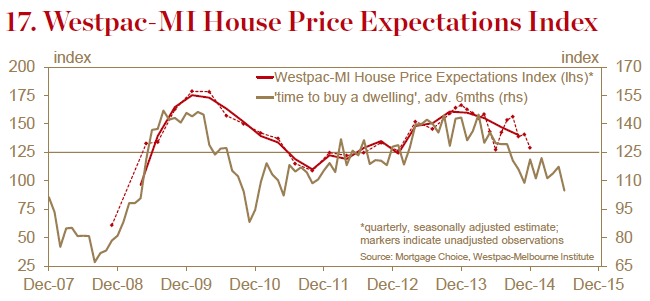

― Consumers’ optimism around the housing market continues to evaporate. The index tracking assessments of ‘time to buy a dwelling’ fell 10.8% to the lowest reading since Nov 2010. This marks a notable break lower from the 110-120 range that has prevailed through most of the year. Readings for NSW and Vic were particularly weak.

― The Westpac-Melbourne Institute Consumer House Price Expectations Index fell 8.3% to be down 22.5%yr. Despite this clear shift, expectations are still positive overall, meaning more consumers expect house prices to rise than fall over the next 12mths. The index is also still comfortably above its low in Jun this year and well above the lows recorded in 2011-12.

― The Westpac-Melbourne Institute Unemployment Expectations Index increased 4.4% to 159.5 (a higher level indicates more consumers expect unemployment to rise). This is the second highest read since the GFC and just shy of the 160 mark – over the last 40yrs, reads above 160 have only been seen in the GFC and during the recessions in the early 90s and early 80s.

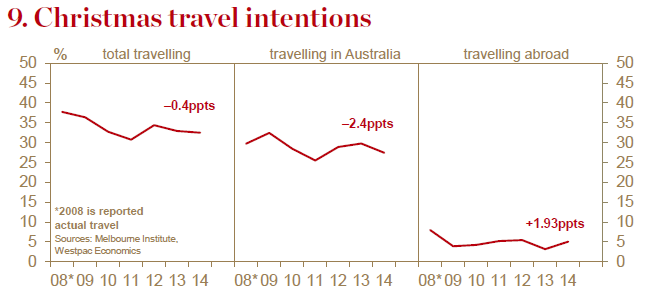

― The Dec survey included extra questions on holiday travel plans. The results show slightly fewer Australians expect to travel these holidays: 32.5% vs 32.9% this time last year.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.