From the AFR:

An analysis published this week by Citigroup put rates of return at Santos’s $US18.5 billion GLNG venture in Queensland down at just 4.4 per cent under a $US60 a barrel oil price, and at 4.7 per cent for Origin Energy’s Australia Pacific LNG project next door. That compares with 8.4 per cent and 8.5 per cent at $US90 a barrel for oil – still rather skinny compared with over 17 per cent for a third train at ExxonMobil’s project in Papua New Guinea.

Even so, these projects have life spans of 30 or 40 years, so the Armageddon scenarios being put about by some look far-fetched. They will still get built, start production and spew off cash – just not as much as under a higher oil price. One project debt lender to one of the Queensland LNG projects says oil prices are still well off the $US40 a barrel or so that might start to cause some nervousness among financiers.

Meanwhile, the decision on Thursday by Malaysia’s national oil company Petronas to defer the long-awaited go-ahead for its $C36 billion LNG export project in western Canada points to a likely stalling of additional new supply in a market where low prices should further stimulate demand.

I haven’t seen any “Armageddon scenarios” being put about for QLD LNG. Those mythical doomsayers do get around!

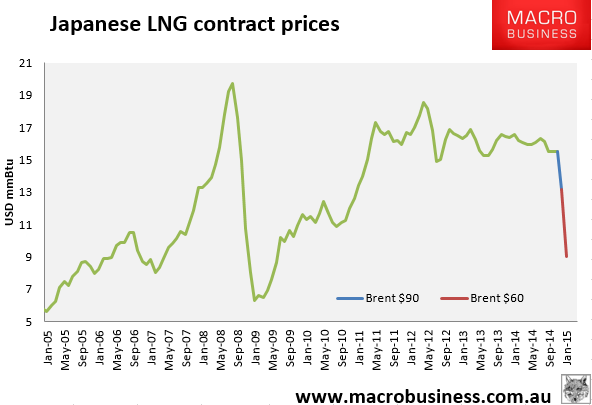

What I do see, here, however are extraordinarily hopeful numbers. At $90 Brent, the LNG contract price is $13mmBtu and at $60 it is $9mmBtu:

So, how can $90 per barrel deliver 8% return when that’s an LNG price of $13, implying a breakeven of $12mmBtu. But if you cut Brent to $60, which is $9mmBtu equivalent, the return only falls to 4%? That makes absolutely no sense.

According to my figures the QLD three can’t make money at $9mmBtu at all if you include capital costs (that is, the cost of building the plants). Their breakeven cash costs (that is, with no cost of building the thing) are around $6-7 so the only way to get to any returns at all is to use an absurdly small figure for your cost of capital.

As for Petronas, that is good news!