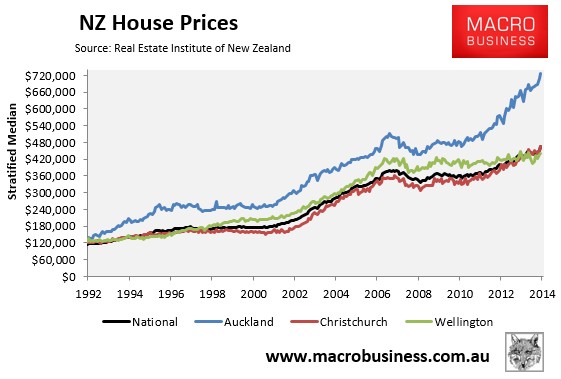

The Real Estate Institute of New Zealand (REINZ) has released its November house price results, which registered a strong monthly rise in values and an acceleration in annual growth.

In the month of November, the national stratified median price rose by 3.3% to nearly $464,000. Prices rose by 2.5% in Auckland, 3.5% in Christchurch and 0.3% in Wellington. Over the quarter, prices rose by 4.9% nationally, with increases recorded in each of the major capitals.