The Final Report of the Murray Financial System Inquiry (FSI), released to the public yesterday, has taken direct aim at the efficiency, equity and sustainability of Australia’s superannuation system.

As expected, the first target is superannuation fees, which the FSI believes are far too high by global standards and are an unnecessary drain on Australia’s retirement savings:

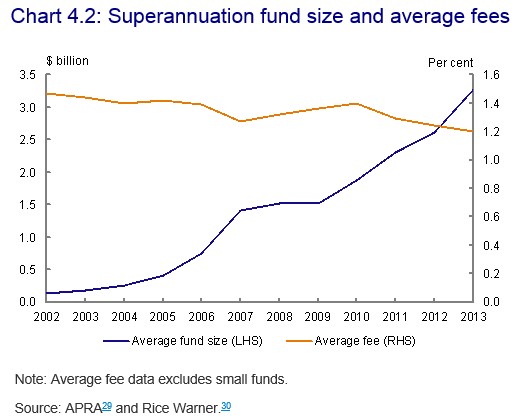

The superannuation system is not operationally efficient due to a lack of strong price-based competition and, as a result, the benefits of its scale are not being fully realised. Substantially higher superannuation balances and fund consolidation over the past decade have not delivered the benefits that would have been expected; these benefits have been offset by higher costs elsewhere in the system rather than being reflected in lower fees. Other design features also contribute to inefficiencies leading to higher costs and sub-optimal outcomes for members, such as the proliferation of multiple accounts…

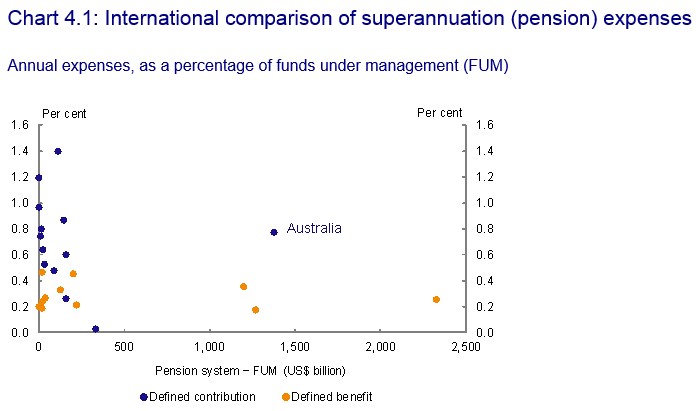

Readers will recall the FSI Draft Report, which included the below chart showing that Australian superannuation fees are high by global standards:

Advertisement

And that super fees had not fallen in line with what could have been expected given the substantial increase in scale:

Advertisement

All of which suggests that Australia’s superannuation funds are not just inefficient, but are gouging members – helped along of course by our system of compulsory contributions, which has provided the industry with a “sheltered workshop” within which to operate.

To overcome these efficiency concerns, the Final Report recommends introducing greater transparency into the superannuation system:

Recommendation 9

Seek broad political agreement for, and enshrine in legislation, the objectives of the superannuation system and report publicly on how policy proposals are consistent with achieving these objectives over the long term…

Advertisement

It also recommends implementing a competitive tender process to select the default superannuation funds for workers, in order to force down fees:

Recommendation 10

Introduce a formal competitive process to allocate new default fund members to MySuper products, unless a review by 2020 concludes that the Stronger Super reforms have been effective in significantly improving competition and efficiency in the superannuation system.

The Final Report also targets leverage by Australia’s self-managed superannuation funds (SMSFs), recommending that rules be amended to prevent SMSFs from borrowing for investment purposes:

Advertisement

Recommendation 8

Remove the exception to the general prohibition on direct borrowing for limited recourse borrowing arrangements by superannuation funds…

Further growth in superannuation funds’ direct borrowing would, over time, increase risk in the financial system… In addition, borrowing by superannuation funds implicitly transfers some of the downside risk to taxpayers, who underwrite adverse outcomes in the superannuation system through the provision of the Age Pension…

As discussed in the Interim Report, the Inquiry notes an emerging trend of superannuation funds using LRBAs to purchase assets.75 Over the past five years, the amount of funds borrowed using LRBAs increased almost 18 times, from $497 million in June 2009 to $8.7 billion in June 2014…

The GFC highlighted the benefits of Australia’s largely unleveraged superannuation system. The absence of leverage in superannuation funds meant that rapid falls in asset prices and losses in funds were neither amplified nor forced to be realised. The absence of borrowing benefited superannuation fund members and enabled the superannuation system to have a stabilising influence on the broader financial system and the economy during the GFC. Although the level of borrowing is currently relatively small, if direct borrowing by funds continues to grow at high rates, it could, over time, pose a risk to the financial system…

Borrowing by superannuation funds also allows members to circumvent contribution caps and accrue larger assets in the superannuation system in the long run…

It is also inconsistent with the objectives of superannuation to be a savings vehicle for retirement income. Restoring the original prohibition on direct borrowing by superannuation funds would preserve the strengths and benefits the superannuation system has delivered to individuals, the financial system and the economy, and limit the risks to taxpayers.

This is a sound observation and a worthwhile reform from the FSI. Superannuation is supposed to be a retirement savings system, not a speculative vehicle. And funds should not be allowed to gear-up into assets.

Finally, the FSI also rightly questions the sustainability and equity of superannuation concessions, which are becoming an increasing drain on the Budget over time, and recommends that they be addressed in the Abbott Government’s upcoming Tax White Paper:

Advertisement

Superannuation taxation arrangements should be reformed to place policy settings on a more sustainable footing over the long term. Superannuation tax arrangements should be targeted to achieve the objectives of the superannuation system, reduce the cost of the retirement income system to Government, better position Australia to meet the fiscal challenges of an ageing population and reduce funding distortions in the economy…

Tax concessions in the superannuation system are not well targeted to achieve provision of retirement incomes. This increases the cost of the superannuation system to taxpayers and increases inefficiencies arising from higher taxation elsewhere in the economy, and the distortions arising from the differences in the tax treatment of savings. It also contributes to the broader problem of policy instability, which imposes unnecessary costs on superannuation funds and their members and undermines long-term confidence in the system…

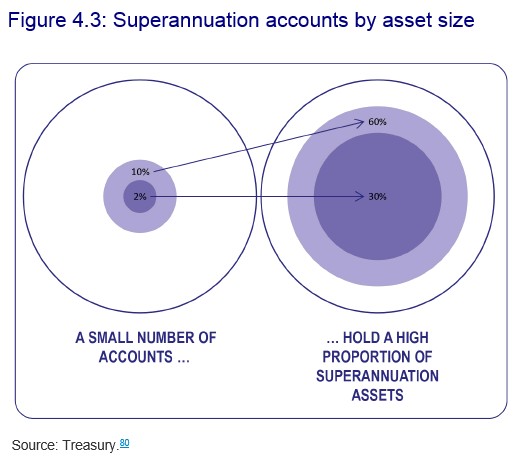

As illustrated in Figure 4.3 of the Interim Report [below], a small minority of members hold a high proportion of superannuation assets. Individuals with very large superannuation balances are able to benefit from tax concessions on funds that are likely to be used for purposes other than providing retirement income, such as tax-effective wealth management and estate planning…

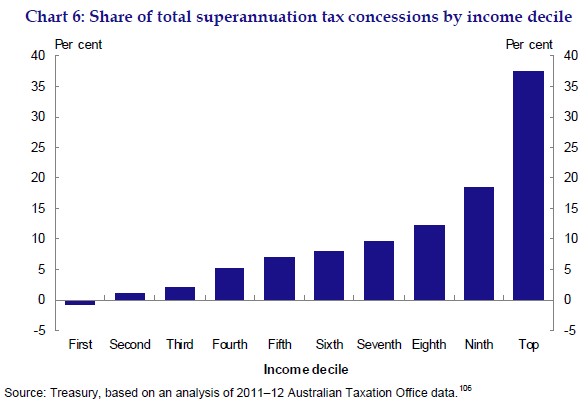

As a result, the majority of tax concessions accrue to the top 20 per cent of income earners (Chart 6). These tax concessions are unlikely to reduce future Age Pension expenditure significantly…

Poorly targeted tax concessions increase the cost of the superannuation system to Government. In turn, this increases the fiscal pressures on Government from an ageing population. Giving high-income individuals larger concessions than are required to achieve the objectives of the system also increases the inefficiencies that arise from higher taxation elsewhere in the economy, including differences in the tax treatment of savings…

The Final Report also recommends that the exemption from tax on super earnings provided to those aged over-60 should be removed:

Earnings are taxed at 15 per cent in the accumulation phase, but are untaxed in the retirement phase. This can act as a barrier to funds offering ‘whole-of-life’ superannuation products and increases costs in the superannuation system.

Aligning the earnings tax rate between accumulation and retirement would reduce costs for funds, help to foster innovation in whole-of-life superannuation products, facilitate a seamless transition to retirement and reduce opportunities for tax arbitrage…

Advertisement

Again, these are very sensible recommendations. Superannuation concessions in their current form are both highly inequitable and inefficient, costing the Federal Budget billions in foregone revenue whilst reducing the progressiveness of the tax system.

Overall, the FSI Final Report has provided a number of sensible observations and recommendations pertaining to Australia’s superannuation system. Let’s hope the Abbott Government and opposition parties embrace them with open arms.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.