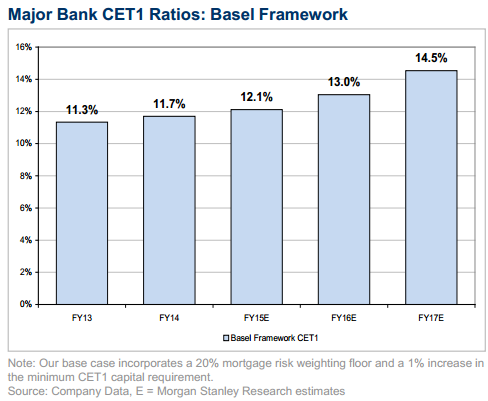

The Financial System Inquiry has recommended a “baseline target in the top quartile of internationally active banks” so that Australian bank capital ratios are “unquestionably strong”. It concluded that the major banks’ ratios are currently above the global median, but below the top quartile, implying a Basel CET1 ratio of ~11.4%. This equates to a capital shortfall of ~A$12bn vs the ~12.2% ratio for the 75th percentile of global banks at December 2013. However, the FSI notes that “the global distribution of capital levels will continue to rise for some time yet”. With this in mind, we forecast the major banks to raise ~A$38bn of common equity via a combination of DRP, share placements and asset sales over the next three years. Our Chart of the Week shows their Basel CET1 ratios would reach ~14.5% under this scenario. However, it’s not clear whether this would place them in the top quartile of global banks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.