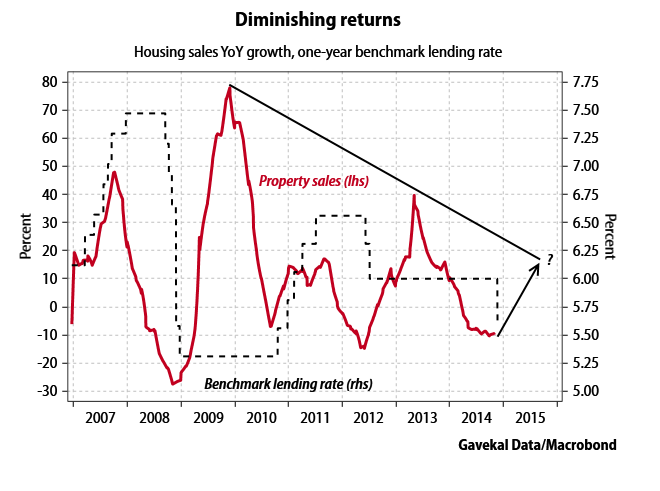

The crucial question is how the new easing cycle will affect credit growth and economic growth. In both 2009 and 2012-13, credit growth surged following rate cuts. In 2009, total credit growth leaped to 36% as new bank loans doubled the target official target. In response GDP growth rebounded to 12% and property prices skyrocketed. In 2012-13, YoY loan growth bounced modestly to 16%, but total credit growth rebounded to 22% in early 2013 as shadow financing exploded. The credit easing ignited another property boom, but the impact on the real economy was limited as real GDP growth only recovered to 7.9%.

This time around the effects will be even more modest. Although credit growth is likely to recover from its current level of 14%, several constraints will hinder a vigorous rebound. First, in past easing cycles the strongest demand for loans came from local governments. Today the Ministry of Finance is cracking down on borrowing by local government-backed projects in an attempt to reduce debt levels. Second, with non-performing loan ratios rising, Chinese banks have become more cautious about counterparty risk and are unwilling to lend as crazily as in the past. Third, because of the strong US dollar capital inflows have abated, limiting the scope for domestic liquidity creation. Fourth, in recent months the PBOC and the China Banking Regulatory Commission have considerably tightened the rules governing the shadow financing market which, far from expanding explosively as in the past, is now actually shrinking.

Finally, with China’s total debt-to-GDP ratio having climbed almost to 250%, it would be extremely difficult—indeed it would be courting disaster—for leverage to expand as quickly as before. As a result, we expect a marginal rebound in credit growth, which will benefit the property market and boost sentiment towards China’s equity market. Shanghai A-shares have climbed 2.2% on Monday morning, with the promise of further rate cuts set to lift property stocks by the most, followed by big state-owned companies, which enjoy the easiest access to bank loans. However the impact on China’s overall economic growth will be limited.

That’s a reasonable base case. What concerns me is credit demand, if the Chinese punter gets it in his head that the structural oversupply in many markets is going prevent much of recovery in prices they may just sit it out.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.