Outgoing Secretary of the Australian Treasury, Dr Martin Parkinson, has given his final speech to the Committee for Economic Development of Australia (CEDA), in which he

Below are the key extracts.

First, Dr Parkinson outlines the conundrum facing the Australian economy, whereby GDP growth will be supported by rapidly rising mineral export volumes, given a reasonable “headline figure”, but national income and employment growth will be anaemic due to falling commodity prices (terms-of-trade) and declining mining investment:

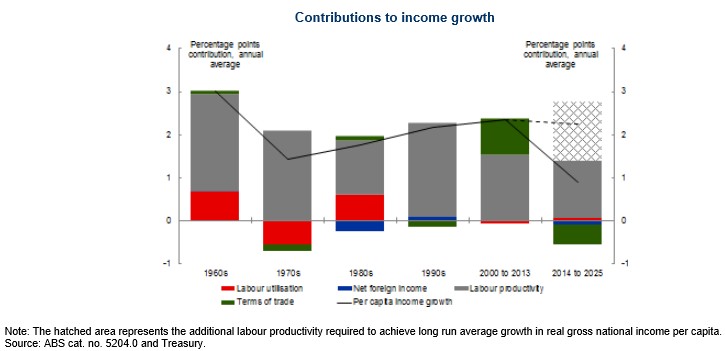

Australia’s growth over the past decade has largely been driven by a boom in demand for our commodity exports, which led to significant increases in resource sector investment and boosted our terms of trade, contributing to higher average incomes.

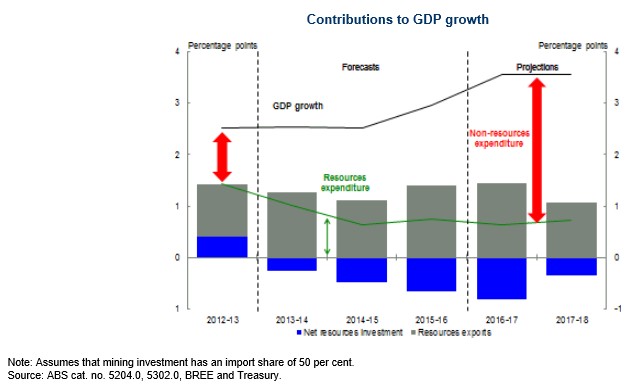

The resources boom is now shifting from an investment phase to production, and this adjustment is being borne out in two interrelated ways: in the adjustment in the real economy as resources investment declines, and in a weakening of national income growth as the terms of trade declines.

The economy needs to shift to broader sources of growth in the economy. As I have noted many times, this will not be seamless.

The mining sector has doubled as a share of GDP in the past decade. Investment in the resources sector as a share of GDP quadrupled over the past decade.

By the end of this financial year, the stock of capital in the resources sector is expected to be four times higher than it was at the start of the mining boom. That investment has, in turn, fuelled a rapid growth in output, the result being that the sector has been the key driver of growth for some years now. But that momentum is rapidly diminishing…

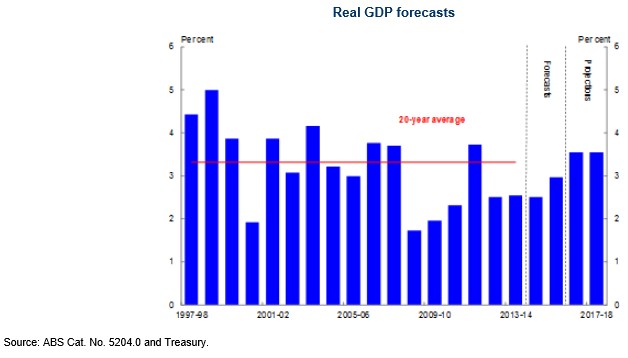

Recent domestic economic developments indicate that the economy will continue to grow at a below-trend pace in the near term before growth in the non-mining sectors starts to significantly pick up. If this were to eventuate, GDP would have grown below trend for 7 of the 8 years to 2015-16, resulting in the creation of a sizeable output gap.

While the economy performs below its potential, a key risk is that the economy will not generate enough jobs growth to absorb new entrants to the labour market.

The risk in this scenario is not so much that the unemployment rate rises – this has largely already occurred. We want to avoid the risk that cyclical unemployment develops into structural unemployment, which would create significant social and economic costs, were this to eventuate.

The flipside is that wages growth has been moderate, which will help with the transition to non-mining sources of growth and is a sign that the labour market is adjusting flexibly, although it is also likely to be dampening consumption.

Dr Parkinson then calls for a real exchange rate depreciation to assist the economy’s transition to non-mining led growth:

Advertisement

Further depreciation, together with low interest rates and slow wages growth, will provide conditions overall that are supportive of growth.

He then notes that, unlike with commodities, Australia has no competitive advantage in services and will need to work hard if it is to secure a growing share of Asian services trade:

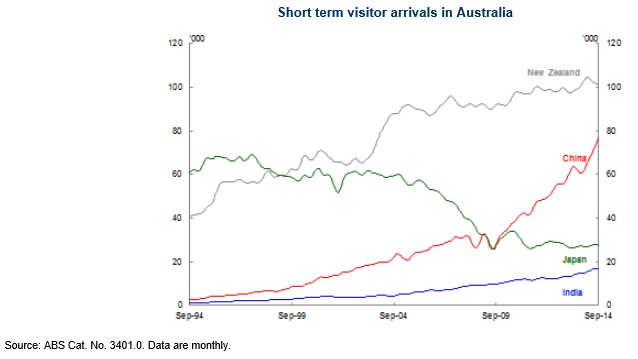

China has become our largest source of overseas students (around 150,000 enrolments in 2013) and our second-largest source of tourists (almost 760,000 in 2013-14). Economic growth in Asia is also likely to continue driving demand for Australia’s resources and agricultural commodities.

But unlike in resources and commodities, Australia has no inherent comparative advantage in the services sector writ large. As I have noted before, Beijing is closer to Berlin than Brisbane. If we are to grasp these opportunities, we will need to work for them, and work hard. There are no grounds for complacency.

Advertisement

Dr Parkinson then argues that Australia needs to undertake ‘root-and-branch’ reform across a broad range of areas in order to maintain competitiveness:

We have the opportunity with the reviews of our tax system, our workplace relations system, the ‘root and branch’ reviews of our financial markets and competition framework, and the review of the functioning of our federation, to make decisions that improve our productivity growth and to position ourselves to reap the most from future prospects.

Public sector reform will also be important. Increasingly, with the ageing of the population and the growing size of our services industries as a proportion of the economy, how well the public sector delivers or contracts services like health and aged care will have a bearing on budget outcomes, as well as the productivity of the economy as a whole.

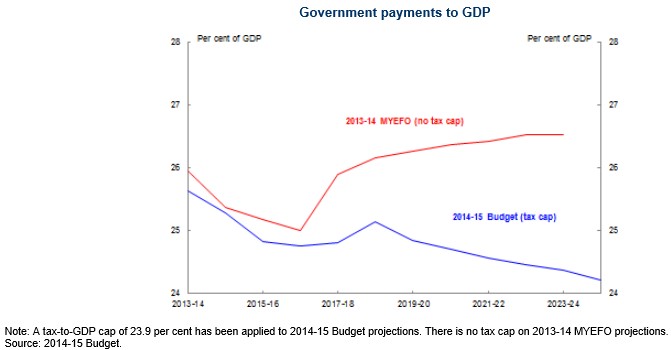

Achieving a more sustainable fiscal position is also critical.

As I have said before, Australia has a structural budget problem that requires a sustained and measured response…

… it is important that we start the process of fiscal consolidation now.

Australia has recorded 23 years of consecutive growth and the budget projections are based on an assumption that this will continue for a further decade. Such an outcome – 33 years of uninterrupted growth – would be without precedent, domestically or globally.

Yet even on this assumption, we know the Budget is likely to remain in deficit in each and every one of the next 10 years unless we take action…

Dr Parkinson then reiterates that without reform, the tax burden will shift overwhelmingly to Australia’s shrinking (in a relative sense) cohort of workers, who will be forced to endure regressive rises in tax rates:

Advertisement

The implications for fiscal sustainability of failing to take action seem to have been lost in the public debate, as if this does not matter to Australia’s future prosperity.

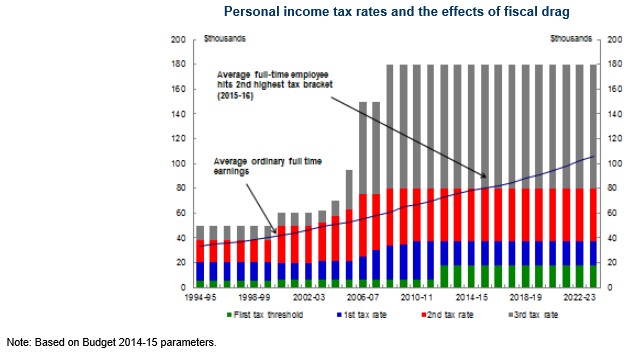

Moreover, fiscal drag, which helps improve fiscal outcomes in the pre-Budget line of this chart, is regressive yet gets little attention. As I have noted elsewhere, allowing fiscal drag to continue will result in someone on average full-time earnings moving into the second-highest tax bracket from 2015-16 and, over the decade ahead, experiencing a rise in their average tax rate of over 20 per cent.

In contrast to the focus of our public debate, comparator countries are lowering personal and corporate income taxes, and shifting the tax mix in favour of more efficient tax bases, in order to better compete globally. The consequence for Australia of maintaining a 1950s tax mix in the 21st century should be self-evident.

Obviously, I agree with the thrust of Dr Parkinson’s speech. After the biggest commodity boom in the nation’s history, Australians have become complacent. And without reform across a broad range of areas, Australia’s global competitiveness will continue to slide, dragging down living standards over time.

With regards to tax reform – arguably Dr Parkinson’s pet area of interest (and the focus of many of his speeches) – there is a clear need to broaden the tax base and build it around more efficient and equitable sources. This requires a shift in sources from productive effort (e.g labour and corporations) towards taxes on land, resources, and consumption, which are far more efficient and more difficult to avoid.

Advertisement

Simply relying on never-ending increases in personal income tax via bracket creep, while the base of workers shrinks as the population ages and the proportion of retirees rises, is neither efficient, equitable or sustainable in the long-term.

There is also a desperate need to reform Australia’s world-beating tax concessions (e.g.superannuation and negative gearing), which cost the Budget many billions of dollars in foregone revenue and are skewed towards the wealthy and high income earners. Fundamental reform in these areas would dramatically improve the progressiveness of the tax system and would also counter concerns that the Budget is fundamentally unfair and places the burden of adjustment unfairly on lower income households.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.