Compared to the Power of Siberia, Altai benefits from existing Western Siberian production and a shorter pipeline route making this a significantly cheaper and faster development – cost estimates vary from $US14-$US18bn (v $US75bn for Power of Siberia) with first gas expected in 2020.

30bcm/yr is ~23mtpa in LNG equivalent terms (equal to Australia’s current production) and equates to ~19% of current Chinese gas demand. While there has been no mention of price, we expect the ~$US9.8/mmBtu agreed on the Power of Siberia to set a strong precedent. Notably this is a significant discount to the ~$US16/mmBtu China currently pays for its LNG (excluding the Guangdong contract with the North West Shelf).

China is looking increasingly well supplied over the medium term. Consequently China may look to LNG more for short term flexibility rather than the longer term contractual commitments required by Australian producers to underwrite expensive projects.

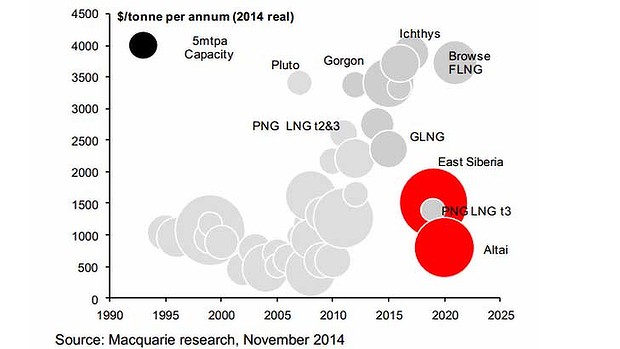

Only the fittest to survive: With ~80mtpa of US LNG exports and up to 68bcm/yr (~50mtpa) of Russian pipeline exports expected by 2025, unsanctioned Australian projects are being pushed up the cost curve at an alarming rate. Indeed, our demand/supply forecasts suggest that only 1-in-20 unsanctioned projects targeting the 2020 market will be required (although this rises to 1-in-5 by 2025 and 1-in-3 by 2030).

Accelerating drift to marginal cost: With too many projects targeting finite (albeit growing) demand, we continue to believe LNG prices will ultimately be determined by the marginal cost of supply. Incorporating this new pipeline supply would see our 2025 LNG demand forecast fall by ~3% to 445mtpa lowering the marginal cost of supply by 4% to ~U$11.40/mmBtu (DES).

Australia’s market window firmly closed: Along with US exports, Russian pipeline volumes will compete with unsanctioned Australian LNG projects further supporting our view that Australia’s market window has closed. This suggests new local projects will be undercut by international competitors while existing projects will see downward pricing pressure at re-negotiation time.

It’s a bad day for Aussie commodities, unless you’re Adam Carr.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.