Global credit ratings agency, Fitch, has labelled Australia’s big four banks’ capital profiles as “about average” and claimed that they could be forced to increase their capital buffers by up to $53 billion – equivalent to nearly two year’s combined profits – if the Murray financial system inquiry takes aggressive action to bolster the banking system:

Australia’s Financial System Inquiry (FSI), due to report by end-2014, is likely to recommend higher capital requirements for the large banks, says Fitch Ratings. A higher capital charge and/or a rise to the mortgage risk-weighting floor for the four domestic systemically important banks (D-SIBs) are the most likely ways in which this will be implemented. In either case, Fitch maintains that Australia’s banks are well positioned to meet the additional buffers though internal capital generation.

Australia’s bank capital profiles have strengthened since 2008, though they are about average relative to their international peers. Fitch maintains that additional capital requirements for the four D-SIBs – ANZ, CBA, NAB and Westpac – would be credit positive.

The FSI, led by Chairman David Murray, is expected to push for regulatory changes that would reinforce the improvements in recent years. The gap between Australia’s banks and global peers in terms of capital strength has closed, though an objective of the FSI is to bring the largest banks back into the upper quartile. Increasing the D-SIB capital buffer requirement from the current 1ppt, as well as implementing a mortgage risk-weight floor for banks using advanced models to calculate regulatory capital, are likely to be two areas of focus for the Murray report.

A number of global initiatives are addressing the wide discrepancy in risk weights based on banks’ internal models, including a Basel Committee project. Risk-weights for residential mortgages have been a particular focus because they can be very low. In Sweden, the risk-weight floor for residential mortgages was raised to 25% from 15% this year, while Norway is raising its floor to 20%-25% from 10%-20%. In Switzerland, the authorities are reviewing the differences between risk-weights based on banks’ internal models and those based on the standard approach used by domestic and regional banks.

Taking the global context into account, there is the potential for the FSI to recommend raising Australia’s mortgage risk-weight floor to 25%, which would result in capital shortfalls for each of the four major banks – AUD2.9bn for ANZ (the lowest) to in excess of AUD4.6bn for Westpac, based on FY14 numbers and assuming the banks maintain an internal buffer of 1ppt over the fully loaded regulatory requirements. Under a more aggressive scenario, where the risk-weight floor is increased to 30%, the D-SIB charge also raised 2ppt to 3ppt, and a 1ppt internal buffer maintained, the capital shortfalls would be between AUD12bn-15bn for each of the Big 4, and total around AUD53bn. With combined profits for the four banks of around AUD29bn in FY14, the capital shortfall under this scenario would be just less than twice annual profit before dividend.

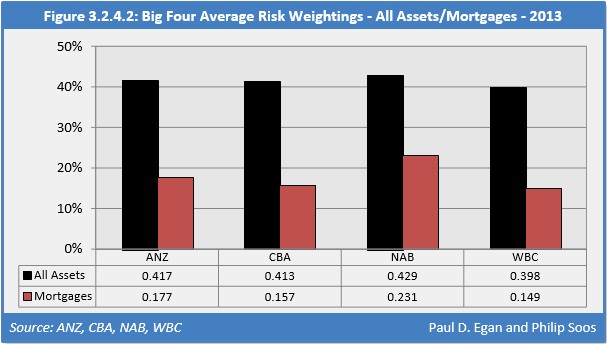

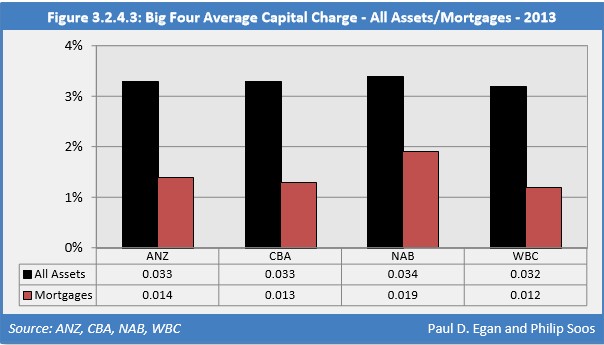

Raising the risk-floor on residential mortgages to 25% or preferably 30%, along with increasing capital requirements on systemically important banks, would be a great move. As noted previously, the average risk-weight applied to the big four’s mortgages currently ranges from just 15% to 23%, with the average capital charge against mortgages a meager 1.2% to 1.9% (see below charts).

More broadly, raising the banks’ capital is absolutely vital in order to safeguard the safety and stability of the financial system, along with Australian taxpayers, who would ultimately be called upon to bail-out the banks if there was a financial crisis.