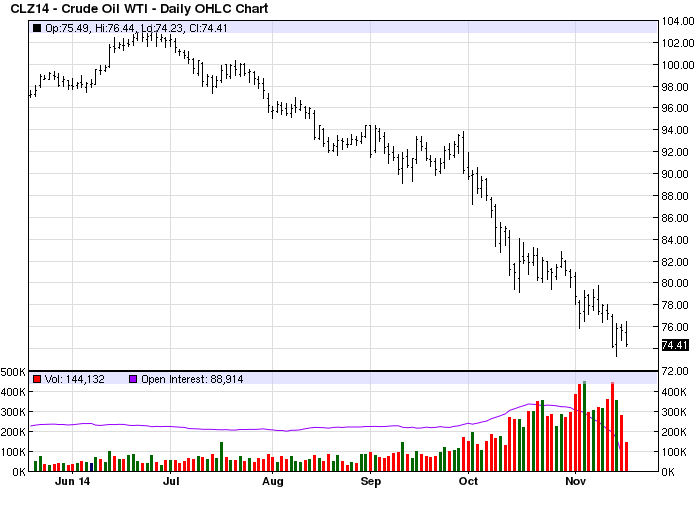

While everyone is focused on the iron ore crash, an equally large mauling is taking place in LNG markets. Overnight, the oil price sank again well over 1% and is trading at $74. 37 as I speak:

Unless OPEC cuts deeply, it’s going to get worse, from Bloomie:

Shale drillers are planning on production growth with fewer rigs despite a worldwide glut that has sent crude prices to a four-year low.