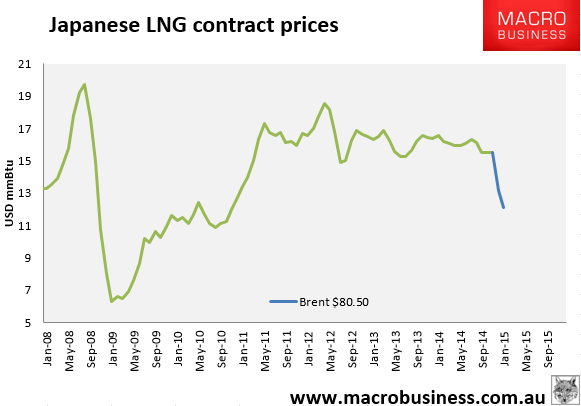

The Brent oil benchmark was more or less stable overnight. That should have left the contract LNG price where it was. However, I shifted from WTI to Brent yesterday in my charting the Japanese Crude cocktail (JCC), which is the underlying price used for LNG, and in the process discovered a glitch in my old calculations. I’ve been far too generous in filling in some of the gaps in the JCC formula and it turns out that I’ve overestimated LNG contract prices by roughly $1mmBtu.

So, here is the new LNG contract chart, based upon Brent oil, today around $12mmBtu:

You’ll have to forgive me, the JCC is a pain the proverbial. In the wider oil market, the news is all about OPEC, from the FT:

Advertisement