From Society Generale’s Wei Yao via FTAlphaville on the Chinese rate cut:

…due to the further rate liberalisation announced at the same time, there is actually no de facto rate cut.

The PBoC surprisingly lowered the benchmark deposit rates by 25bp and the benchmark lending rates by 40bp. After the change, the 1-year benchmark deposit rate is 2.75% and the 1-year benchmark lending rate is 5.6%. We did not see this coming, but we are not wrong either – the cut is not really a cut. The PBoC conveyed the same message in its communiqué following the cut, stating that the interest rate cut is a “neutral” operation and does not mean a shift in monetary policy stance.

This is all because, along with the rate cut, the PBoC also lifted the upper limit that commercial banks can offer above the benchmark deposit rates to 1.2 times from 1.1 times. That is, the maximum permitted rate for 1-year deposits was 3.3% (3%*1.1) and is still 3.3% (2.75%*1.2). Given that commercial banks have been losing deposits recently, they will probably choose to stick to the upper bound. Then, there will be really no change to deposit rates at all! As for lending rates, the lower bound to the benchmark lending rates was removed more than a year ago. In theory, there is no hard restriction stopping commercial banks from lowering loan rates anytime or by any amount. Therefore, the benchmark lending rate cut is also nothing more than a suggestion.

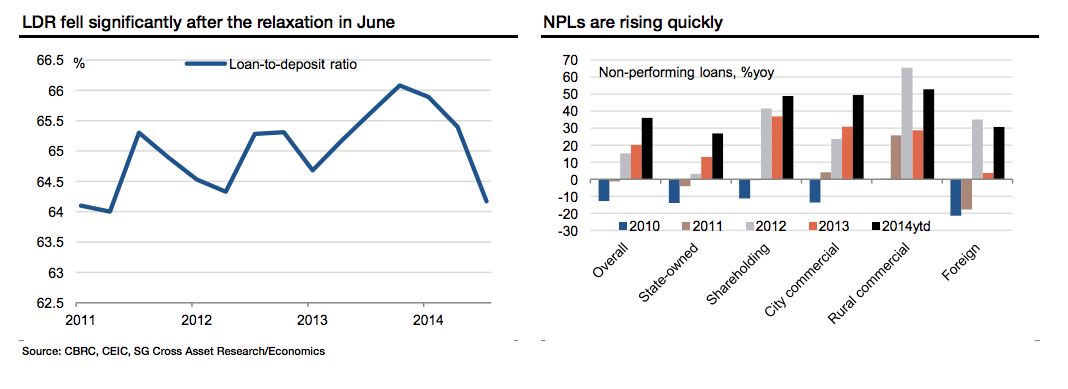

…The excess reserve ratio increased from 1.7% in Q2 to 2.3% in Q3. That was about CNY600bn of additional deposits set aside, which offset over 90% of the liquidity injection made by the PBoC over the quarter. It is not surprising that the transmission from liquidity conditions to credit conditions was frustratingly limited up to October. Interest rates on corporate loans averaged 7% in Q3, unchanged from Q2 and much higher than in 2009 and 2010. Mortgage rates continued to inch higher for the ninth consecutive quarter in Q3 to 7%.

Only entering Q4, the PBoC’s easing has started to work. The most notable sign is the decline in bond yields across the board. For instance, the yield on 5-yr CGBs (China government bonds) has dropped by 50bp quarter-to-date, after staying above 4% most of the time since mid-2013. Although the central bank’s liquidity injection has pushed commercial banks to buy bonds, the bank loan growth remains on a downtrend, sliding further to 13.2% in October from 14.1% at end-2013. However, this pace is still faster than economic growth. Also, given the already mind- boggling size of the outstanding, slower loan growth is inevitable and necessary. It is not convenient when the shadow banking system is going through deleveraging at the same time.

…In our view, commercial banks are reluctant to oblige policymakers’ easing request also because they see rising non-performing loans (NPLs). The gigantic size and the double-digit growth rate of bank loans have kept the NPL ratio at 1%, but the NPL stock has been growing at a 35% clip this year. Smaller banks have seen faster deterioration, with NPLs rising 50% yoy. The worse is still to come and banks know it. Chinese banks have doubled their loan loss provisions and quickened capital-raising via the issuance of preferred shares and convertible bonds.

Considering rising credit risk, it is quite normal for commercial banks to be cautious. If anything, Chinese commercial banks are still the most cooperative commercial banks in the world as they continue to grow lending at double-digit paces. If China wants to make a shorter cut from liquidity easing to credit easing, NPL write-downs and debt restructuring has to quicken.

Policymakers have issued a few measures in an attempt to help banks dispose of bad loans more easily. The ongoing local government debt restructuring may help free up banks’ balance sheets to some degree as well, but the bigger concern lies with state-owned enterprises (SOE). We estimate SOE debt at close to 100% of GDP, twice as much as private corporate borrowing. Given that banks have always preferred SOEs, a disproportionally large part of banks’ balance sheets is probably locked into low- to non-performing SOE loans. Without meaningful SOE reform, China’s private sector will continue to see difficult credit conditions.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.