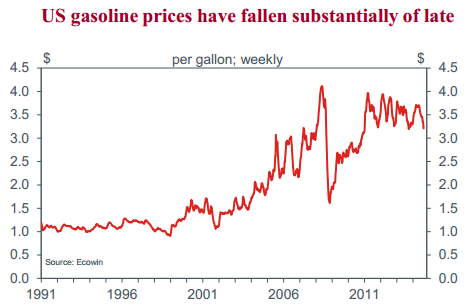

Since mid-June 2014, the oil price has fallen by over 20% and gasoline and heating oil futures have followed suit. The price which consumers pay for gasoline at the pump is down a more modest (but still substantial) 13% from its late-June peak.

The impact this decline has had on inflation and consumption is noticeable through July/August. The energy CPI and PCE subindexes have fallen around 3.0% over this time; and, based on the fall in the price of retail gasoline through September, a further material drop in this component of inflation is to be expected.

For consumption, the decline in energy prices has been the primary cause of the 4% drop in nominal spending on energy goods & services, with prices contributing 3ppts of the fall over the two months to August (as above) and volumes around 1ppt. Available retail sales detail for September indicates this trend will continue to the end of Q3, with gasoline sales down 0.8% in the month.

A question then arises: are the dollars households are saving on the cost of fuel likely to support stronger discretionary spending?

In assessing whether this is likely to occur, we need to consider the overall price change, not just energy prices. On an annual and 6-month annualised basis, there has been little change in the pace of PCE headline inflation: the annual inflation rate ticked down from 1.6%yr to 1.5%yr between June and August; and the 6-month annualised pace edged down from 2.0%yr to 1.8%yr.

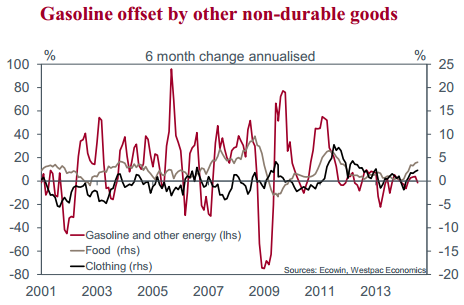

If the material decline in gasoline prices has not (to date) significantly lowered the pace of headline inflation, then what has been the offset? Because of their high weights in the consumption basket, the rise in the cost of food and housing are particularly key.

Total nominal consumption of energy goods and services stands at about 5.5% of total personal consumption. In contrast, food has a weight of about 7.5%, while housing (rent and imputed rent of owner occupiers combined) makes up around 15% of consumption.

Whereas the cost of energy has declined by 3% between June and August, the cost of food and housing has only risen by 0.6% and around 0.5% respectively. However, owing to their larger weights, these gains have offset more than half of the fall in energy prices.

That leaves a marginal improvement in discretionary incomes after food, energy and housing costs are accounted for over the two months to August. But two months is a very brief period of time; to assess the evolving welfare of US households, we need to consider a longer time frame.

Over the year to date, the price gains experienced for food and housing have well and truly eclipsed the small decline in the price of energy. Specifically, in annualised terms, the price of food has risen 3.4% while the price of housing has increased 3.1%; against these gains, the energy index has declined by just 0.6%.

So, in contrast to the two months to August, over 2014 as a whole, the combined effect of the price movements for these key non discretionary items has been to crimp disposable income and, all else equal, restrict households’ discretionary consumption.

Given the above as well as the historically soft household income growth that the US continues to experience, it is not that surprising that we have seen a deceleration in retail sales momentum of late.

One month does not make a trend, but the broad-based weakness apparent in the September report speaks to an unwillingness/ inability amongst households to continue to increase their discretionary spending. While direct holdings of equities by US households are limited, the recent decline in the stock market will arguably add to this trend; and, from a confidence perspective, so too could fears over Ebola.

It also bears remembering that the experience of each household is not homogenous. Those lower down the income spectrum (who make up the bulk of the population) will feel the effect of these price gains the most. Further, those who rent are also likely to be worse off on a discretionary income basis than those who own their own home as rent inflation for tenants continues to accelerate (currently 3.5% annualised) back towards levels last experienced in the pre-GFC period. The net effect of the above trends is likely to be a continued soft-to-modest pace of household consumption growth through the end of the year and into early 2015.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.