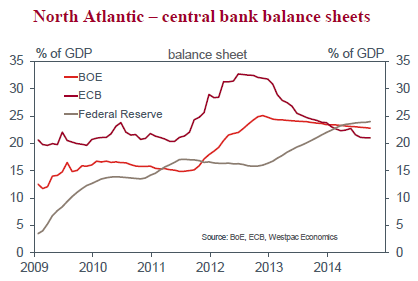

As we come to the end of October, we find ourselves facing a new state of affairs. Not only will an end to tapering in the US halt the provision of new liquidity to the US financial system, but the Fed’s balance sheet will also start to shrink relative to the size of the economy – a trend apparent in Europe and the UK for some time.

What does this mean for the global economy and equity markets?

For the US economy, the impact of this policy shift is unclear. This is because US banks are largely yet to put the liquidity afforded to them to work. Relative to the end of 2008, commercial bank lending to businesses (including securities lending) is up $400bn; but lending to households remains $550bn lower six years on.

With the liquidity provided by the Federal Reserve in times of distress remaining available to the banks post tapering, what matters for lending to the real economy is not the loss of marginal liquidity provision but rather confidence in the sustainability of the recovery. The move towards policy normalisation should give households and businesses greater confidence in the outlook and banks cause to intermediate credit. (Note, we omit here the many structural difficulties US households and firms still face).

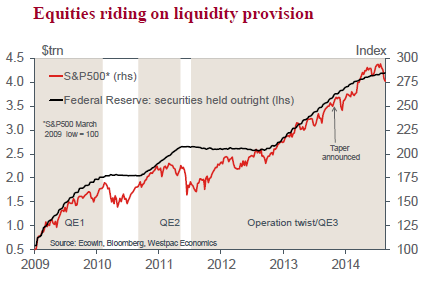

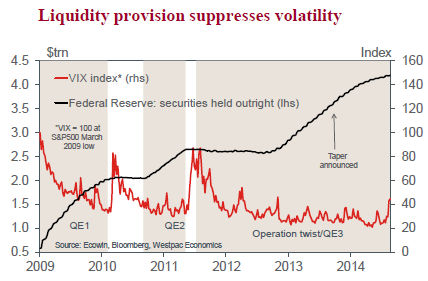

For equity markets, there has been a very clear relationship between the confidence that QE has instilled and stable, enduring market gains. Evidence from the end of QE1 and QE2 speak to a material risk of market declines and/or heightened volatility following the end of QE3, as do the recent market ructions.

To see recent equity market highs retaken and further gains thereafter will require increasing confidence in the earnings outlook sans QE, arguably driven more by revenue growth than efficiency and cost repression. An aside: here is cause for a protracted period of ‘rates on hold’ before the normalisation process begins.

With ‘QE’ (i.e. the announced asset purchase programs for covered bonds and ABS and TLTROs) getting underway in Europe, there is a further point to consider. Will liquidity accommodation there offset the loss of liquidity provision in the US, thereby providing additional support/ stability to global growth and/or financial markets?

With respect to growth in Europe, while it is fair to argue that the ECB’s actions will support the existing level of activity, it is hard to justify an expectation that it will lead to materially stronger growth.

This is because, on the evidence we have to hand, European lending conditions remain tight and demand for credit is weak. The consequence is a continued absence of positive credit growth and little additional support for the real economy.

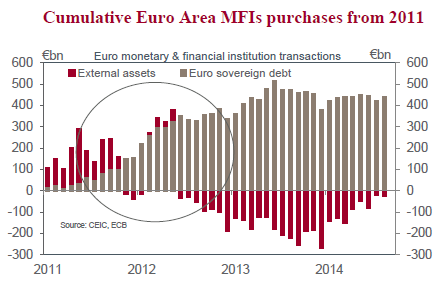

Outside of Europe, what matters is the scale of the ECB’s liquidity injection as well as where the funds end up. On the first point, given that over €300bn in LTRO funding needs to be repaid to the ECB early next year and the difficulties the ECB is facing operationalising its purchase programs, it will take considerable time for their balance sheet to expand. We expect that the balance sheet won’t see a meaningful increase in scale until the second half of 2015.

Second, if history repeats, then these funds are most likely to find a home in liquid, safe domestic assets like sovereign government bonds – absent active support for foreign bond purchases from the ECB. US and global markets are hence unlikely to benefit significantly from the ECB’s actions, even as scale is attained.

Overall, an end to QE in the US is likely to see greater volatility return to global financial markets and put the onus for further market returns more onto revenue growth. This is despite ‘QE’ in Europe, with its implementation likely to prove problematic and the net liquidity it provides largely quarantined to Euro sovereign bonds and other ‘safe’ domestic assets.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.