It’s RBA week and the Shadow RBA is shifting to rate rises:

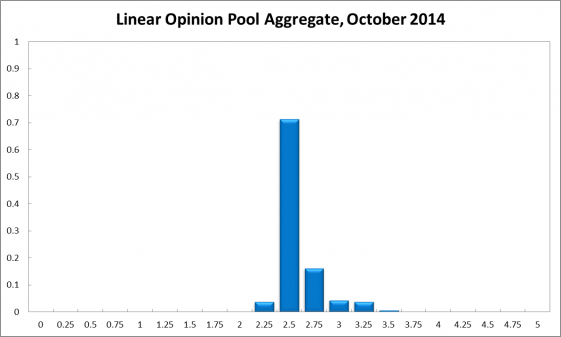

After lingering around the US¢93 mark for several months, the Aussie dollar recently depreciated by approx. US¢5, while other domestic and international economic data continues to be mixed. This fall should help stimulate and rebalance the domestic economy but the extent is uncertain. The CAMA RBA Shadow Board recommends that the cash rate remain at its current level, yet there is growing confidence that it ought to be raised in 6-12 months. The Board attaches a 71% probability that the cash rate ought to remain at 2.5% in October. The confidence attached to a required rate cut equals 4%, while the confidence in a required rate hike has increased to 25%.

The aberrant spike in Australia’s unemployment rate in July 2014 has been reversed but slack in the labour market remains. (The unemployment rate equals 6.1%.) Wage pressure is thus no serious concern. There is no new inflation data available. However, should the Aussie dollar’s relative weakness persist, this will add inflationary pressures to the domestic economy. Business indicators are weaker, with the NAB Business Confidence, the Manufacturing PMI, and the Westpac consumer confidence index all deteriorating slightly. Estimates of GDP growth are largely unchanged. The construction industry is still responding positively to the housing boom. Increased military and security expenditures will put pressure on the federal government’s bottom line while key budget measures have yet to secure passage through the Upper House.

The foreign exchange market has come out of hibernation during the past few weeks. The Aussie dollar lost US¢5, partly due to the relative strength of the US dollar, partly due to retreating commodity prices. A weaker dollar ought to help boost non-mining exports; however, weaker commodity prices will hurt the mining sector.

The global economy is not faring as well as hoped. US GDP growth looks solid but falling inflation expectations raise the spectre of deflation and may point to future economic weakness. The Chinese economy is slowing; this is acknowledged by Chinese policy makers, along with the need to restructure and rebalance the Chinese economy. Uncertainty about Chinese growth and official announcements to aim for more ambitious CO2 emission reductions point to sustained weakness of commodity prices and Australia’s terms of trade. News of Europe’s economies is not good as several Euro-zone countries are flirting with recession. The military efforts in the Middle East, along with heightened security measures, will likely drag the global economy down.

The consensus to keep the cash rate at its current level of 2.5% is 71%, down 3 percentage points from September. The probability attached to a required rate cut equals 4% (6% in September) while the probability of a required rate hike has risen to 25% (21% in September).

The probabilities at longer horizons are as follows: 6 months out, the probability that the cash rate should remain at 2.5% fell considerably, from 49% in September to 38% in October. The estimated need for an interest rate increase rose to 56% (42% in September), while the need for a decrease equals 7% (9% in September). A year out, the Shadow Board members’ confidence in a required cash rate increase is up 10 percentage points to 71%, the need for a decrease ticked down to 9%, while the probability for a rate hold dropped to 20% (29% in September).

The individual comments are worth a look:

PAUL BLOXHAM

The major development this month has been a substantial decline in the Australian dollar. Last month this was the key tension for the monetary policy outlook. The combination of a high currency and falling commodity prices was squeezing local incomes and the high Australia dollar was also constraining local competitiveness. The Australian dollar has fallen due to both US dollar strength and further declines in commodity prices. Assuming the lower level of the currency is sustained, it should be expected to support a further lift in local demand over time, as it helps to improve competitiveness and supports local incomes. At the same time, the lower currency will add upside risk to the inflation outlook, which supports the case for lifting interest rates, at some point, particularly given that the housing market is continuing to show signs of exuberance. However, given the current looseness of the labour market and the likely dampening impact that this will continue to have on wages growth, I expect that the upside risks to near-term inflation are still only modest. I recommend the cash rate is left unchanged this month. Looking further forward, I continue to expect that the cash rate may need to be lifted in the next 6-12 months, partly to prevent a housing bubble from inflating.

What, is this 1999? The bubble is now. Yet there is nothing else going on so if the RBA raises rates the economy will come apart. Some can see it:

BOB GREGORY

I am still not moving much on interest rates. Six months ahead I am changing slightly I think but the housing market is confusing me a lot. I favour some short run intervention of some sort but very unlikely that RBA will be able to put something together quickly.

Macroprudential in other words. Others are all for the bust:

JAMES MORLEY

The forecast for the Australian economy is mixed. The collapse of the iron ore price and a generally weaker outlook for China will be a clear drag on the Australian economy going forward. However, the lower Australian dollar and a more robust recover in the United States could help offset weakness in the export sector. Domestically, it seems clear now that negative short-term real interest rates have fuelled excessive growth in residential and commercial real estate prices. Combined with inflation running at the top end of the RBA’s target range, there is a strong impetus for the RBA to begin a tightening cycle soon, especially since the large increase in the unemployment rate in July has been reversed. The main risk to the domestic outlook remains over exactly how contractionary an implemented budget will turn out to be. On balance, then, the RBA should consider starting a tightening cycle before the end of the year, especially if the housing market continues to overheat and in the absence of a more sustained large upward movement in the unemployment rate.

One more has his head in the sand:

JOHN ROMALIS

Little has changed since last month, with the most notable change being a slightly weaker dollar and lower prices of some key commodities. The Australian economy still seems to be slightly soft, with some slack in labour markets contributing to low wage growth. Looking forward, rising housing construction should help offset the negative effects of declining mining investment. While a slightly weaker dollar will contribute to a modest increase in inflation, weaker commodity prices will crimp the domestic economy somewhat. Economic and financial conditions in our main trading partners appear to be increasingly robust, which should help restore domestic confidence and keep commodity prices at reasonable levels. So while rates should remain constant for now, there is a greater likelihood that the target cash rate should rise later in the forecast horizon.

Err…hello…China? Finally, confusion is probably the winner on the day:

GUAY LIM

Getting the stance of monetary policy right is difficult at the moment. Keeping interest rates low may encourage further rises in house prices but hiking the cash rate may dampen further falls in the Australian dollar. On balance, it might be better to leave the cash rate unchanged this month as the outlook for growth and employment remains weak.

I remain of the view that the next move in rates is down as the income shock combines with the capex cliff and slowing housing at some point.