Coalition finance minister, Mathias Cormann, has today announced details of the float of Medibank Private, claiming that the sale would raise between $4.3 billion and $5.5 billion for the federal government. From The Guardian:

Cormann said this would place the business among the top 100 companies on the ASX. About 2.7bn shares are expected to be sold in the float, to be finalised by December.

The government intends to sell down its entire shareholding and use the funds on its asset recycling scheme aimed at encouraging infrastructure construction. More than 750,000 Australians pre-registered their interest in receiving a share offer prospectus…

Cormann said there was no compelling policy reason for the government to continue to own Medibank, which he described as “a commercial business operating in a well-functioning and competitive private health insurance market with 34 competing funds” .

“The sale will also remove the current conflict where the government is both the regulator of the private health insurance market and owner of the largest market participant,” he said.

The sale of Medibank Private is one of the few current privatisations that I broadly support.

As noted by Cormann above, Medibank competes directly with a wide range of private health insurers. And because there is already significant competition in the marketplace, there would not appear to be any competition concerns arising from Medibank’s sale, since the new private owner would not be able to unnecessarily raise premiums and gouge consumers for risk of losing market share to its competitors. As such, it is unlikely to break the first rule of privatisation: that it does not materially lower competition in the marketplace.

The sale of Medibank also appears to be reasonable from a financial perspective. Generally speaking, whether a privatisation is beneficial financially depends upon whether the upfront funds received by the Government will outweigh the expected net present value of future dividends.

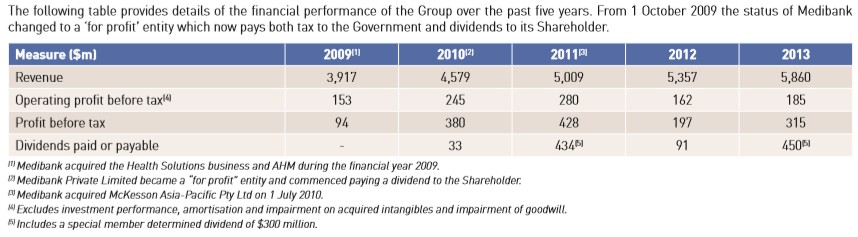

A quick analysis of Medibank’s 2013 annual report (the latest available) shows that Medibank averaged profit before tax of $330 million over the past 4 years, implying an average net profit after tax of $231 million (assuming a 30% tax rate).

Given dividends can only sustainably be paid out of post tax profits, selling Medibank for between $4.3 billion and $5.5 billion infers a foregone yield of between 4.0% and 5.5%, which seems reasonable in light of the potential economic and social returns from the alternative infrastructure investments funded from the sale.

Balancing the above considerations, there appears to be reasonable grounds for privatising Medibank, which is more than can be said for the spate of natural monopolies for sale by the various state governments.