by Jordan Eliseo, Chief Economist ABC Bullion

Gold investors were looking forward to Q3 this year. After a solid start to 2014, with gold one of the best performing assets in the 6 months to June, more upside was expected.

At the time, gold prices were sitting around the USD $1315oz mark, with many predicting a price in and around the USD $1400oz mark by now, based off 40 odd years of data, which highlighted that Q3 was typically a very strong quarter for the yellow metal.

Alas – it was not to be, with the surging USD Dollar (the September monthly returns of which are plotted below – chart via Macrobusiness) the primary reason behind the weakness in the yellow metal of late.

General commodity price weakness hasn’t helped either, with oil plunging, alongside agricultural commodities too. Indeed the DB Commodities Tracking Index Fund is now 13% lower than where it was 3 months ago – testament to the weakness in the entire commodities complex right now.

For gold specifically, the fall in the price in the just completed quarter was one of the worst on record, coming in at -7.49% in USD terms. Since the late 1970s, there’s only been two times where Q3 has seen a bigger correction.

One of those times, the gold price had a 3.4% bounce in Q4, whilst the other time (in 1984), a Q3 correction of -7.8% was followed up with an even more harrowing fall of over 10% in Q4 that year.

Were something like that occur, we’d see gold back in the mid $1000-$1100oz USD range, which is more or less in line with where many see the market heading in this correction. As we discussed last week, we’re not convinced we’re going to see a drawdown of such extremity (in part because nearly EVERYONE is expecting it), but we are only averaging money into gold and silver right now – as that seems the most prudent course of action

Gold Sentiment

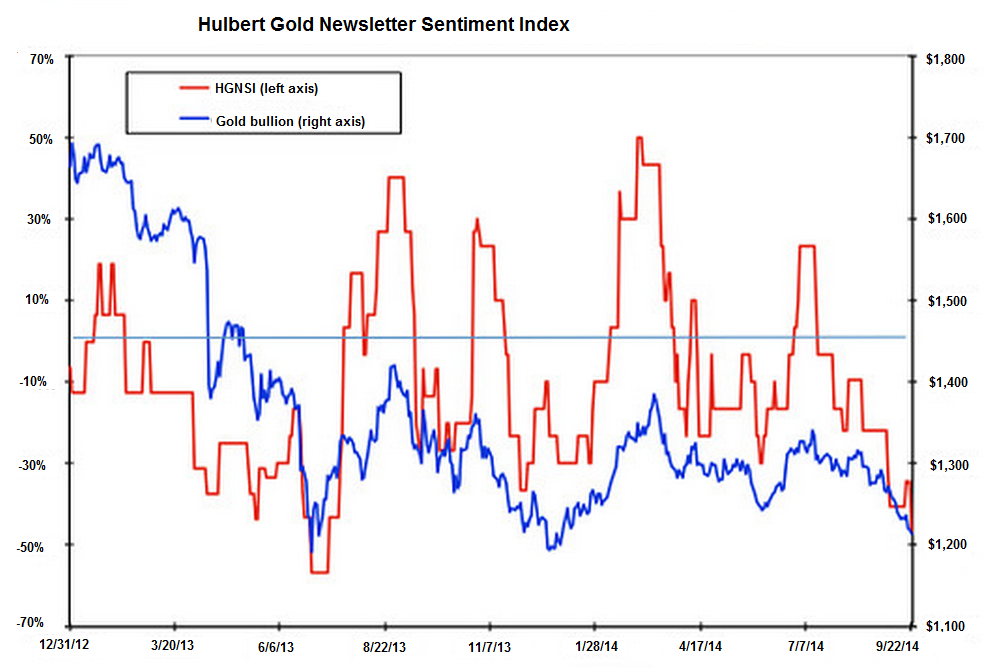

With the recent weakness in the precious metal market, and the onslaught of negative press towards the sector, its not surprising that sentiment towards the precious metal market is close to all time lows.

Indeed the Hulbert Gold Newsletter Sentiment Index (HGNSI), which measures the percentage newsletter writers recommend to allocate to gold related investments, either on the long or short side, is currently sitting at -46.9%, the second worst reading in 30 years!

All this (and more) is covered in an excellent article by Pater Tenebrarum of Acting Man, which you can read here.

The only time the HGNSI was lower was in June 2013, right before gold started a circa USD $200oz rally, which if repeated, would again put gold in the USD $1400oz range we approach Christmas 2014

You can see how low HGNSI readings tend to correlate with gold price rallies in this chart here.

The bearishness in the sector is all pervasive right now, with Sentiment Traders industry group table also showing that there is literally zero percent bullishness towards the sector, just like the readings in June and December of 2013.

You all know what happened in the months following that.

Bottom line to this is that whilst there is the potential for gold to go lower in Q4, we’re already at attractive buying levels for long-term investors, and sentiment is unlikely to get much worse.

As such, a small rally into year-end shouldn’t be ruled out, and I fully expect to see gold prices comfortably higher by this time next year.

How about Silver!

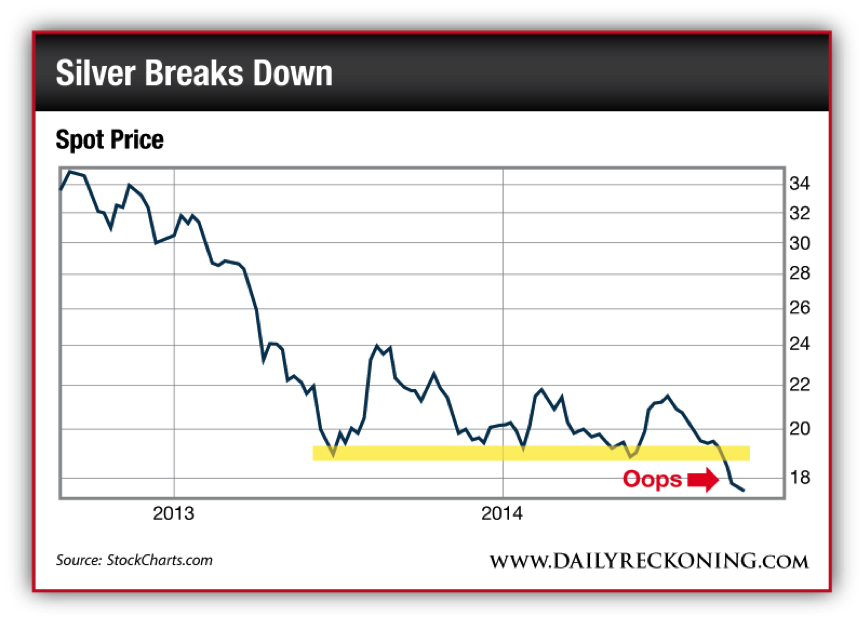

If the last 3 months have been disappointing for gold investors, they’ve been even worse for those invested in the silver market. Starting the new financial year at just shy of USD $21oz, silver has shed nearly 20% of its value in the past quarter, and is currently sitting just above USD $17oz.

More importantly, silver has broken through support, as the following chart from the Daily Reckoning highlights.

Whilst this is obviously troubling a number of investors (I’ve taken more than a few calls and emails on the subject of late), in reality this is exactly the kind of behaviour you see when a market is bottoming, or very close to doing so.

It is of course exactly what happened in the 1970’s, with both silver and gold, as this article from King World News (which focuses on silver), attests too.

Whether or not we see the kind of rally we did in the late 1970’s this time around remains to be seen, but we are either at or likely close to a incredible buying opportunity in the silver market.

Long-term investors should be encouraged by this capitulation type selling, rather than frightened, as it is only in markets that are hated like this that one can find the most incredibly mid to long term money making opportunities.