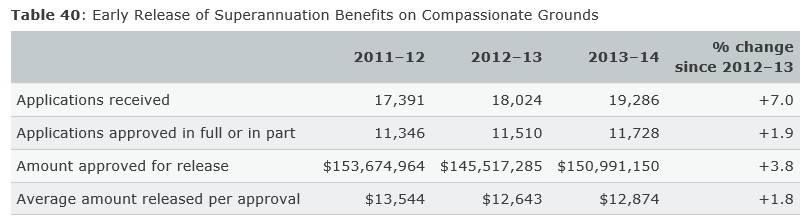

The Department of Human Services (DHS) has released its 2013-14 Annual Report, which revealed that the number of Australians seeking to access their superannuation early jumped 7% over the financial year to 19,286, which was the highest level since the Global Financial Crisis (see next table).

The Early Release of Superannuation Benefits program allows eligible people to draw on their superannuation benefits under specified compassionate grounds in a time of need.

As shown above, around three in five applications to release super early were approved by the DHS, totaling nearly $151 million and averaging $12,874 per successful applicant.

According to News Limited, which reported on the release over the weekend, much of the growth in applications to access super early went to paying-off mortgages.

unconventionaleconomist@hotmail.com