by Chris Becker

UBS is out with a research note today that spells all will be fine with Megabank, the four bank oligopoly, post the Murray Financial Inquiry (FSI), which is considering a raft of measures to actually put some lead in the thin line called banking stability. UBS contends that any such additional costs to “gold plating” the system will likely be passed on to customers in the form of lower deposit rates, cuts to discount mortgages and of course, lowered business lending, while scarcely effecting bank ROE or ROA and hence profitability.

We estimate that even if the FSI took a more conservative approach to Major banks’ capital (eg 20% minimum mortgage risk weights & 3% D-SIB) and the major’s responded by increasing NIM (net interest margin) by 15bp over time, the banks would still be able to generate an ROE of ~15%.

However, we believe the impost from holding higher levels of capital is likely to be partially passed onto customers. Over the last thirty years, the Australian banks have shown an ability to absorb significant change, while maintaining their profitability. This is the result of a very supportive industry structure and an ongoing drive for efficiency.

Ain’t that the truth – having the politico-housing complex at your back for this “private” sector has been a dog-send. Although I’m not as sanguine as UBS are at what is effectively half a rate hike for mortgage holders.

More on how these costs can be passed on to society, instead of by the banks:

The banks have been easing rates on Term Deposits for some time as funding markets have thawed and wholesale funding costs have improved. We would expect the banks to further reduce deposit rates post capital raisings;

The banks have been undertaking fierce competition for new mortgages over the last two years. This has led to a significant increase in the discount rate offered off the Standard Variable Mortgage Rate upon approval. During this time discounts offered have increased from around 70-80bp to as much as 120-140bp.

Post capital raisings we would expect these levels of discounts for new mortgages to be pulled back. Similarly, we would expect fixed rate mortgage offerings to be increased slightly.

Business customers are also likely to see some widening of spreads offered on some facilities. This is similar to the wider spreads endured post the financial crisis as the banks passed on higher funding costs. That said the impact from holding higher levels of capital is likely to be much less significant.

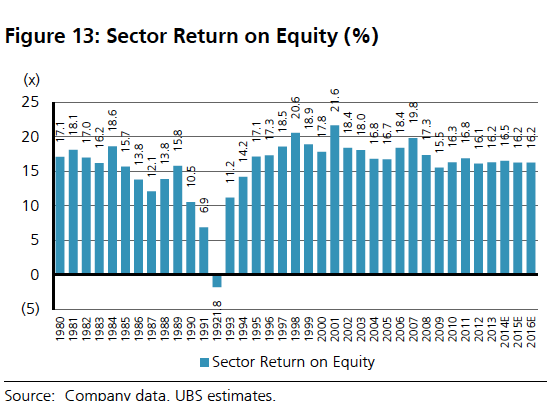

UBS are right to mention that simply inching the SVR up by 10-15 bps independent of the RBA is not going to be as easy compared to the post-GFC recovery period, particularly with the smaller competitors able to maintain lower SVRs with their lower capital requirements. It will be a delicate balance but UBS are very optimistic forecasting stable return on equity in the years ahead:

This points to a re-confirmation by the mainstream analysts that banks will remain a good investment and the current market correction (where fully franked yields on banks are headed again for double digit territory) gives credence to buy the dip. In fact, UBS point to a recent precedent in Sweden where a tripling of risk weighting saw their banks directly pass on costs to customers, while at the same time take some heat out of the credit market and cause the retail bank share prices to surge.

That the same “silver lining” scenario is on the cards for Megabank is a bit of a stretch, given the completely different macro factors that are and will impact the oligopoly in a post FSI world including falling national income, rising unemployment and a reversing carry trade.

So-called “gold plating” a banking system that is at its heart as fragile as ever will come at a cost but at least it’s in a good a cause.