by Chris Becker

ECB President Mario Draghi failed to provide two solutions last night following the ECB’s monthly rate meeting, where the refinancing rate was kept at 0.05% and deposit rates in the negative.

First, no real solution to the ongoing European deflation/unemployment quagmire and secondly, no pumping of the asset markets with liquidity to keep the speculators in The City and elsewhere happy.

As a result, European stocks fell, led by the embattled Italian banks, but all across the continent major and minor bourses were sold off as the ephermal gains for 2014 were wiped out. In related markets, the Euro staged a small rally against the USD while the varied bond market saw sell offs in the peripheral Spanish and Italian ten years (yields up to 2.14% and 2.35% respectively), Greek bonds saw a small bid while the German 10 year Bund was bid.

What did Mario come up with that made the market ditch it like 5 day old fish?

Another round of quasi-purchases, that is, a two year program to scoop up covered bonds (starting this month) and other asset-backed securities later this year. Although expectations were for an epic 1 trillion euro size program, the ECB President threw cold water on that target and ruled out any purchase of government bonds.

There was speculation that not wanting to lock in a definite number probably came from the German side (centre – ok, vice like grip) who wanted to limit such purchases. The problem is the covered bond/securities markets they are targeting, even with a massive price tag, are way off from where any targeted stimulus needs to be.

Here are the Austrians (lowest unemployment in the EU) complaining:

Austrian Central Bank President Ewald Nowotny opposed today’s decision on concerns over the risks it adds to national central bank balance sheets, according to euro-zone officials who asked not to be identified because the discussion was confidential. Bundesbank President Jens Weidmann opposed the whole package including the ABS program at the September meeting, officials said last month.

In the press conference immediately afterward – not as boring as usual – Draghi was really on the back foot, staunchly defending his actions in what he sees as his rock/hard place:

- The economy is still fundamentally weak. The recent weakening in the euro area’s growth momentum, alongside with heightened geopolitical risks, could dampen confidence and, in particular, private investment.

- I find this description of the ECB as the guilty actor here needs to be corrected. Other policy areas need to contribute decisively.

- We are going to gear our action according to how the medium-term outlook of our inflation expectations will develop in the coming months. Not coming years. Coming months.

Mario sounds peeved. And why wouldn’t he with the core, low unemployment and highly indebted banking nations like Austria and Germany dictating to the rest of the continent that austerity should rule amid near record high unemployment and ridiculous scares about inflation.

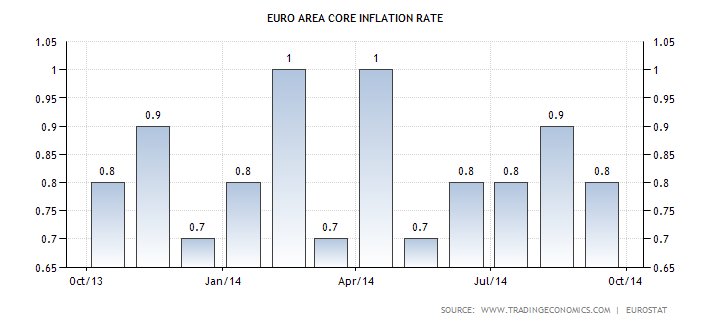

This is a continent teetering on the edge of a Japanese style deflation, with core inflation below 1% and dropping, with the five year forward breakeven rate falling below 2% from earlier in the year and now at 1.9% even after the ECB cut rates and pre-empted the current plan.

There is probably only one more card the ECB can play – if allowed – and that is sovereign bond purchases. Because there is time running out going down the austerity path, as the demonstrations in Naples overnight show a (southern) continent seething again – Naples has a local unemployment rate of 25% while Italian youth unemployment is running at 44%!