ANZ Chief, Mike Smith, has once again warned that Australia’s Big Four banks risk becoming globally uncompetitive if they are required to raise capital levels to withstand external shocks. From The Canberra Times:

In a market briefing on Friday, Mr Smith argued Australian banks were already well capitalised compared with peers. Tougher capital rules would push up the cost of credit across the economy, he said.

“We need to think very carefully about importing other people’s solutions to other people’s problems, and frankly, Australia deserves a better debate on this issue than we have seen to date,” Mr Smith said.

“We need to understand that there is a real cost to regulation and policy settings that are too conservative and too restrictive.”

“Higher capital costs will come at a cost to customers who will pay more for home lending. It will come at a cost to business who will pay more for loans to grow their business. And it will come at a cost to the economy through lower growth, fewer jobs and lower tax revenue.”

“There are those who dispute these impacts – but frankly, these are simple economic facts.”

Advertisement

I hate to repeat myself, but Smith’s contention that Australia’s banks are “well capitalised” is highly contestable.

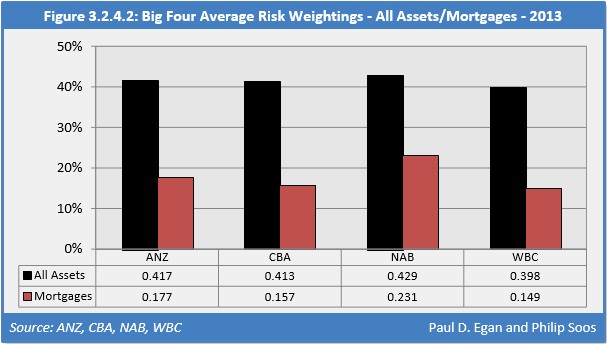

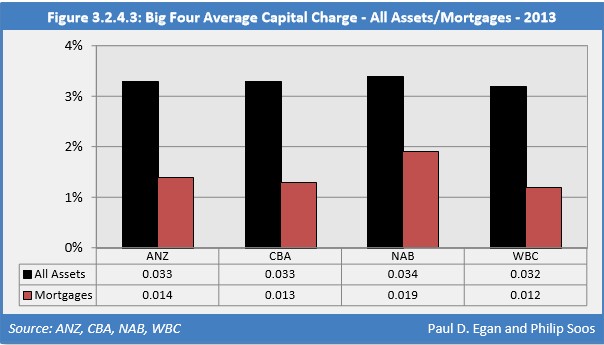

As shown in the below charts, which come from Phil Soos’ and Paul Egan’s book Bubble Economics, the average risk-weight applied to mortgages ranges from a pitiful 15% to 23%, with the average capital charge against mortgages a meager 1.2% to 1.9%, with ANZ holding just $1.40 of capital per $100 of mortgages on its book:

Advertisement

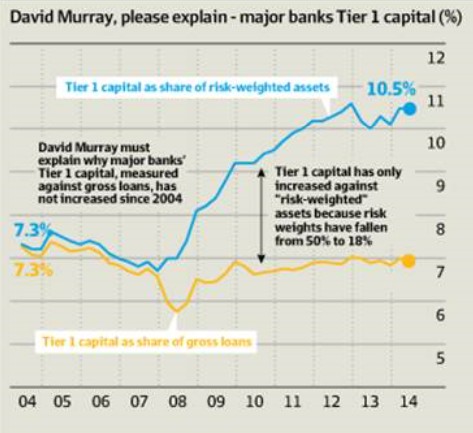

Further, as noted recently by The AFR’s Chris Joye, the actual level of capital held against the banks’ gross loans has fallen over the past decade:

The defining question Murray must focus on is this: “Why are the majors holding less equity capital and more leverage than they were a decade ago, which runs contrary to the universal belief the banks are better capitalised than they were before the global financial crisis?”.

…thanks to the crazy reduction in the major banks’ risk weightings on home loans from 50 per cent before 2008 to 18 per cent today, it looks like equity capital has increased when it really has not…

Advertisement

Given the above facts, raising bank capital levels is entirely appropriate in order to safeguard the safety and stability of the financial system, along with Australian taxpayers, who would ultimately be called upon to bail-out the banks if there was a financial crisis.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.