There are arguably few better businesses to be in than Australian superannuation.

Thanks to compulsory contributions, set at 9.5% of employee wages currently, along with a largely fixed cost structure, the superannuation industry continues to rake it in, earning fat fees on everyone’s retirement nest egg.

Last night, ABC’s The Business aired an interesting segment revealing that Australians paid super funds $20 billion in fees last year, up 8% and equating to around $2,000 per member.

It wasn’t all bad news, however, with average management fees declining, courtesy of reforms under the My Super and Freedom of Financial Advice (FoFA) schemes. Although fee reporting is opaque, which makes changing funds more difficult.

Advertisement

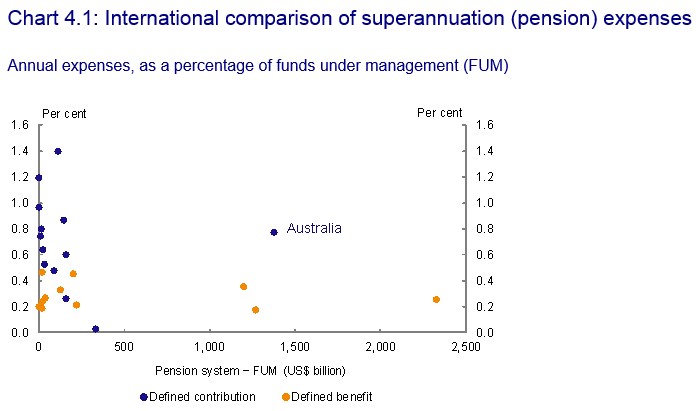

The Draft report of the Murray Financial System Inquiry was particularly scathing of Australia’s superannuation fees, noting that we have amongst the most expensive system in the world:

The operating costs of Australia’s superannuation funds are among the highest in the Organisation for Economic Co-operation and Development (OECD), and the Super System Review concluded superannuation fees were “too high”. The Grattan Institute estimates fees have consumed more than a quarter of returns since 2004. Although the Inquiry notes the difficulties of comparing costs or fees across funds, especially internationally, the evidence suggests there is scope to reduce costs and improve after-fee returns (see Chart 4.1).

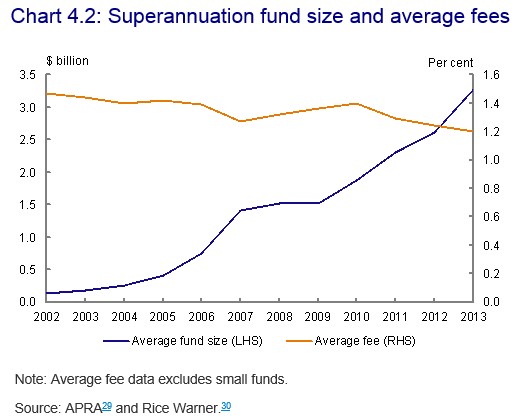

The Draft Report also found that fees had not fallen in line with what could have been expected given the substantial increase in scale, which will dramatically reduce consumer’s retirement nest eggs:

Advertisement

Fees can significantly affect retirement incomes. The Super System Review found that reducing fees by around 40 per cent — or 38 basis points — for the average member would increase their superannuation balance at retirement by approximately $40,000 (or 7 per cent)…

As I have noted previously, in a well functioning and competitive market, average fees would have fallen as the value of funds under management has risen. This is because superannuation is largely a fixed cost business, and it should not cost ten times more to manage $1 billion of funds under management than it does to manage $100 million.

However, despite the huge explosion of superannuation balances since the superannuation guarantee (compulsory super) was introduced in 1993, average fees have barely changed, as clearly illustrated above.

Advertisement

All of which suggests that Australia’s superannuation funds are not just inefficient, but are gouging members – helped along of course by our system of compulsory contributions, which has provided the industry with a “sheltered workshop” within which to operate.

While there has been some recent progress superannuation on fees, they need to fall much further to bring Australia’s retirement system in line with global best practice. And until this occurs, along with reforms to superannuation concessions to make the system more progressive, the Government should definitely not raise the superannuation guarantee to 12%, as this would only further feather the nest of the superannuation industry.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.