The Reserve Bank of New Zealand (RBNZ) this morning released its monetary policy statement for September, which has left the official cash rate (OCR) unchanged at 3.50%, but also lowered its forward guidance for rate rises. The RBNZ also warned on the New Zealand dollar “remains unjustified and unsustainable” and faces “further significant depreciation”.

The economy appears to be adjusting to the policy measures taken by the Bank over the past year. House price inflation continues to ease, despite strong net immigration. CPI inflation remains moderate, reflecting subdued wage increases, well-anchored inflation expectations, weak global inflation, and the high New Zealand dollar. However, spare capacity is being absorbed, and annual non-tradables inflation is expected to increase. Risks also remain around how strongly net immigration will affect housing demand, and the extent to which pressures in the construction sector will impact broader inflation.

In light of these uncertainties, and in order to better assess the moderating effects of the recent policy tightening and export price reductions, it is prudent to undertake a period of monitoring and assessment before considering further policy adjustment. Nevertheless, we expect some further policy tightening will be necessary to keep future average inflation near the 2 percent target mid-point and ensure that the economic expansion can be sustained.

Advertisement

Specifically on housing, the RBNZ notes that price growth is weaker than would normally be expected given interest rates and migration flows, suggesting its macro-prudential limits on mortgage lending are working:

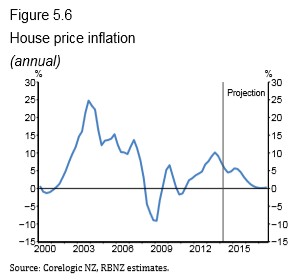

Annual house price inflation is projected to moderate over the medium term from current rates of around 6 percent (figure 5.6), as mortgage interest rates increase, migration flows normalise and increased dwelling construction alleviates supply shortages. As chapter 2 notes, house price inflation is weak compared with what past relationships with net immigration, interest rates and other factors would suggest, and the projection assumes that this weakness continues.

The RBNZ also lowered its forward interest rate guidance by 0.5% and now expects the OCR to peak at 4.8% by 2017.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.