Last Tuesday, the Australian Prudential Regulation Authority (APRA) released its latest statistics on Australian authorized deposit-taking institutions’ (ADIs) exposure to residential property, which showed an increase in the proportion of higher-risk loans underwritten by Australian banks, including investment loans, interest-only (IO) loans and loans written outside normal serviceability criteria. The increase in higher-risk lending is credit negative for Australian banks because it weakens the credit quality of their portfolios.

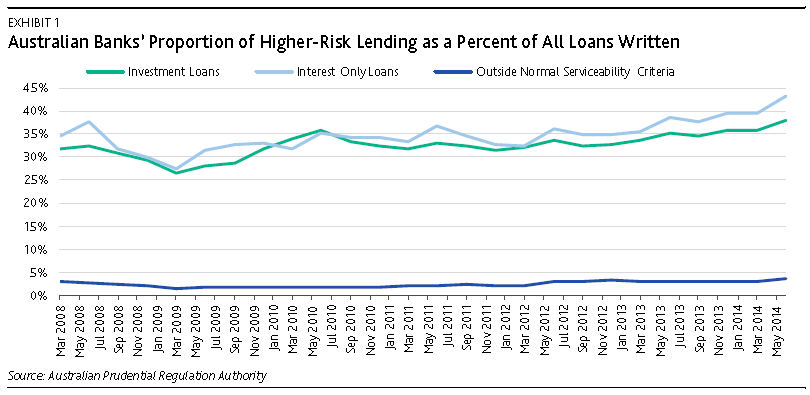

APRA’s data show three notable negative developments during the June quarter (Exhibit 1). The proportion of investment loans written by Australian ADIs as a percent of all newly written loans rose to 37.9%, compared with a 2008-14 average of 32.6%. Over the past 12 months, the total value of outstanding mortgages to investors increased by 10.9%, versus a 7.5% growth rate for loans provided to owner-occupiers. The proportion of newly written IO loans rose to 43.2% in the quarter, and now comprises 35.7% of all outstanding loans, the highest percentage on record. The proportion of loans approved outside normal serviceability criteria8 – where the lender makes an exception to its policy – rose to 3.7%, again the highest proportion in ARPA’s 2008-14 sample.

Although investment and IO loans performed well during the global financial crisis, they inherently carry higher default probabilities and severities, and a larger proportion of such loans risks leading to higher delinquency levels for Australian banks at times of stress. Investment loans typically have higher loan-to-value ratios (LTV): our data indicate that the average LTV for investment loans is 60.2%, versus 57.8% for owner-occupier loans. In addition, since the underlying properties are not the primary residence, they are more sensitive to changes in house prices and borrower employment status and thus are more likely to default if the borrower’s conditions change. IO loans are more exposed to rising interest rates than principal-and-interest loans. Our expectation that interest rates in Australia will rise over the next 18 months means there is an increased likelihood of a payment shock for these borrowers at the end of the initial IO period.

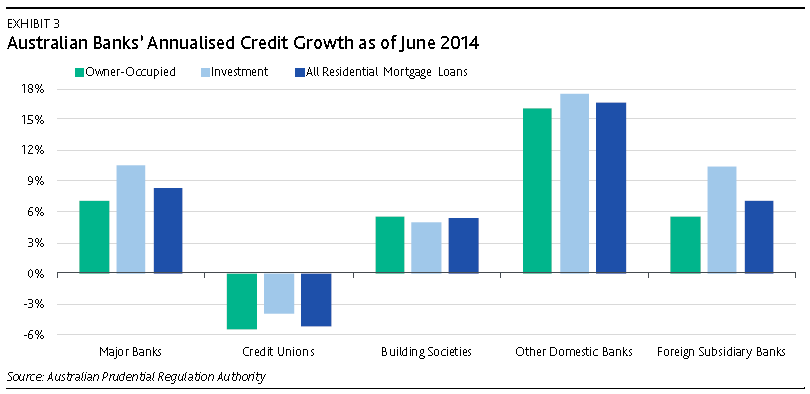

…Higher-risk lending is particularly negative for banks whose credit growth has significantly outpaced system growth.

Looks like it’s snouts in the investor trough across the banking sector to me and it is quite right of Moody’s to warn. It will be very interesting to observe when the downgrades flow.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.