Moody’s has a nice description of the re-inflating Australian housing bubble today:

Australian Banks Resilient to Housing Stress, But Tail Risks Are Rising

Concerns Over Sustainability as Australian House Prices Rise. Residential house prices have been rising rapidly in recent quarters, increasing by close to 14% since May 2013 (Exhibit J in the Appendix). The recent rise resumes the upward trend in home prices seen over the past two decades. While a further acceleration in prices could over time become credit-negative,2 housing market developments on their own are unlikely to cause significant losses for Australian banks. Bank Residential Mortgage Portfolios are still Healthy. An accelerating housing market presents a medium-term risk for the Australian economy, and, consequently, household balance sheets and the quality of bank mortgage portfolios. Nevertheless, the housing market is not a significant source of potential losses for Australian banks in the immediate future because:

HOUSE PRICE INCREASES NOT FUELLED BY A CREDIT BOOM.

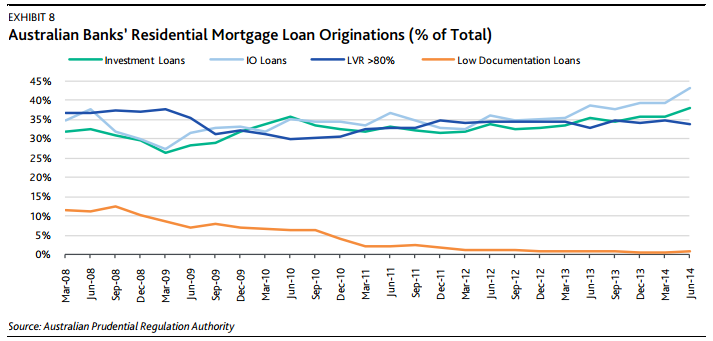

House price increases have thus far not been accompanied by the rapid credit expansion and sharp loosening of lending standards that characterize historical examples of credit boom-and-bust cycles. Overall credit growth at around 6% per annum remains at levels significantly below those recorded before the global financial crisis of 2008-09. Similarly, although there are some signs of increased higher-risk lending, overall lending standards have remained relatively stable. The proportion of mortgages with a high loan-to-value ratio (LVR) has remained broadly similar to long-run averages, and the percentage of low documentation loans is negligible (Exhibit 8). At the same time, the increased proportion of investment and interest-only loans is a notable negative development: at 37.9% and 43.2% of all newly written mortgages, this type of higher-risk lending is at historical highs.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.