“Mad” Adam Carr is back, once again slamming the notion that Australian housing is overvalued and opposing the need for the RBA to implement macro-prudential controls in a bid to cool rising house prices:

…property as a long-term investment is simply a no brainer: It isn’t that risky over the medium to long-term and it’s baseless to suggest it is, both historically and with reference to current fundamentals…

For a start, property investors account for only 38 per cent of the value of total loans. Much is made of the fact that this highest rate since 2000, but such comments are highly misleading. These are rates not much above the average (around 33 per cent). Indeed the RBA notes that the proportion of the population who are property investors actually remains very low — rising from 8 per cent in the mid 1990’s to only about 10 per cent in 2011/12. Maybe that’s 11 per cent now…

That macroprudential regulation will fail is obvious when you look at these metrics – investors will be able to side step them with relative ease…

Property is and will remain extremely attractive even as macroprudential controls are introduced — this is clear. Indeed the fact is the debate has already been lost by property doomsayers. All the arguments they present as to why property prices can’t possibly go higher and why investors have made a huge mistake are already wrong. Property prices are pushing higher — in real time and rapidly. Investors have made a lot of money. All the theorising about why they shouldn’t, and why they won’t, doesn’t change the reality that they have — and will…

Seriously, you can’t make this stuff up.

In Mad Adam’s world, property prices can only rise and it represents a largely risk-free investment – both to the investors themselves and the macro-economy more generally. Never mind the fact that Australian housing values are already at or near their all time-high valuations relative to incomes and GDP, with prices also growing at around four times the rate of incomes and mortgage debt approaching a record high share of income. Or that these record highs will likely be breached just as the Australian economy goes through its biggest adjustment in decades as the largest commodity price and mining investment boom in the nation’s history unwinds, along with the shuttering of the local car industry.

No worries. It’s all good according to Mad Adam.

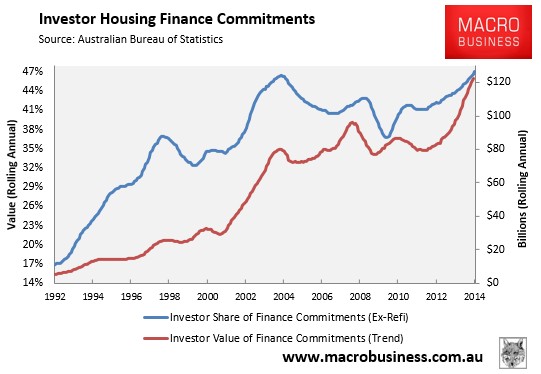

As for Carr’s claim that investor mortgage demand is not that extreme – he cannot be serious. The below chart tells the story, and shows the share of investor mortgages (excluding refinancings) rising from 17% in the early 1990s to 47% currently:

Similarly, his claim that “the proportion of the population who are property investors actually remains very low” at “only about 10 per cent in 2011/12” is delusional. Seriously, what would constitute a ‘high’ level of investment property ownership in Carr’s world? 30%? 40%? 50%?

The beauty of the RBA’s/APRA’s proposed macro-prudential controls, which would increase interest rate buffers on mortgages (from say 2% to 3%) is that it would affect both owner-occupiers (first home buyers) and investors alike, removing some higher risk loans from the market. Sure, it’s no panacea, and reforms to taxation (including negative gearing) and the supply-side are also warranted. But it is far better than merely letting prices and debt balloon, risking a bust down the track.

Finally, Mad Adam’s argument that because home prices are rising strongly justifies property investors’ actions, and proves that macro-prudential measures are not needed, is back-to-front. Strong house price growth, which is not based on economic fundamentals, is precisely why macro-prudential controls are needed.

Put simply, there are more than enough risks on the horizon to counter Carr’s panglosian view that Australian housing is a one-way bet. Valuations are already at or near near all-time highs and housing is getting riskier by the day as prices continue to rise in the face of the slowing economy. Authorities need to act now to ward off a damaging correction down the road.