A bit of over-excitement has seized the SMH blog this afternoon as its fatal lack of context leads it to the usual conclusion: China is stimulating!

Meanwhile, China’s benchmark money-market rate fell the most in two months on signs the central bank will keep monetary policy loose enough to support an economic recovery.

The People’s Bank of China pumped 7 billion yuan into the financial system in the five days through yesterday, a fourth weekly injection.

China will allow listed property developers to sell bonds on the interbank market, Reuters reported yesterday, citing three unidentified people.

‘‘This new policy initiative suggests that Chinese authorities are keen to shift some financing demand to the capital market, with an intention to lower the overall cost of funds,’’ says Zhou Hao, a Shanghai-based economist at ANZ. ‘‘The market liquidity conditions are improving.’’

The seven-day repo rate, a gauge of funding availability between banks, dropped 16 basis points to 3.23 per cent this morning in Shanghai, according to a weighted average from the National Interbank Funding Centre. That was the biggest decline since July 3.

Relaxing the listed developer issuance rules will help boost property market sentiment and support risker assets, according to a report yesterday by Guotai Junan Securities. This is a further step in helping cash-strapped developers cope with a market downturn, Guotai Junan said in the report.

China’s yuan has hit a nearly six-month high on the back of a long-running rally.

The People’s Bank of China set the midpoint rate at 6.1666 per US dollar before the market opened, up 31 pips from the previous fix.

The spot market hit 6.1340 per US dollar, the highest level since early March, during morning trade. It closed at 6.1411 on Wednesday.

‘‘Risk appetite has improved on signs China’s economy is still holding up, while political risks in Ukraine are receding,’’ said Daniel Chan, a Hong Kong-based analyst at Brilliant & Bright Investment Consultancy. ‘‘The yuan is still on trajectory for a gradual, mild appreciation.’’

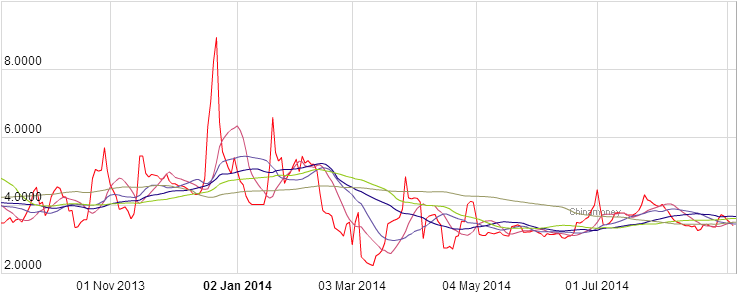

A few points. Monetary policy is neither loose nor loosening and PBOC injections and sterilisations are very unexceptional events. Here is repo, which remains above H1 rates:

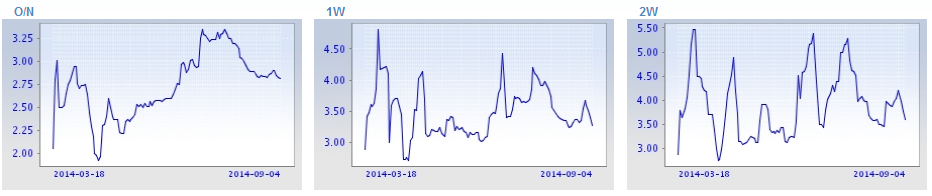

And SHIBOR is the same:

The rising yuan can mean credit is flowing better but still firm interbank rates suggest not and the rising currency is still a part of delivering greater purchasing power to consumers over time. That is, it is part of the structural adjustment.

There is no “recovery” either. This is a structural adjustment to different drivers, and lower levels, of growth supported by periodic fiscal stimulus.

I’m sure China will be doing what it can to prevent a total melt down in the developer sector but that’s a long way from renewed “risk appetite”. That the economy is holding up is true and good news, as evidenced by the non-manufacturing PMIs yesterday, but that’s reason for no more stimulus, hence the iron ore crash waltzing straight through it yesterday.