Slowly but surely, the Coalition is beginning to see the light on superannuation, and acknowledging that the current make-up of the system is unsustainable for Australia’s long-term finances and ripe for fundamental reform.

Today, Coalition MP, and former advisor to Peter Costello, Kelly O’Dwyer has penned a worthwhile piece in The AFR, arguing that raising compulsory superannuation (the “superannuation guarantee”) to 12% would only compound the deep structural flaws already present in Australia’s super system, making the whole retirement system even more expensive and less effective:

If you knew there were weaknesses in the foundations for a building, would you make sure the foundations could be fixed and repair them before increasing its size by more than 25 per cent?..

Under Labor’s timetable for an increase in compulsory superannuation, the Commission of Audit concluded that there was unlikely to be an increase in the proportion of Australians who were fully self-sufficient… [T]he proportion of people eligible for an age pension would remain constant at about 80 per cent for the next forty years. That’s the same proportion of the population that received the pension in the late 1970s…

The Commission of Audit and Henry Tax Review each canvassed reforms to the eligibility tests for the pension…

Australia’s superannuation system is [also] unusual by world standards in allowing Australians to withdraw their entire superannuation as a lump sum…

Research cited in the Inquiry’s Interim Report highlights that approximately 44 per cent of retirees who take a lump sum use it to pay off housing and other debts, to purchase a home or to make other home improvements. A further 28 per cent use the lump sum to purchase a holiday or new vehicle…

The system effectively encourages Australians to over-capitalise on their homes, spend all or some of the balance on other forms of consumption, and then turn to the age pension…

Naturally, the situation is exacerbated by yet another quirk in the system, where the access age to superannuation (60, if you are retired and were born after July 1, 1964) differs from the eligibility age for the age pension (currently 65, rising to 70)…

Then there are other issues: like the level of competition in superannuation and whether it is resulting in fees which truly represent the value delivered, rather than blatant rent seeking…

O’Dwyer is correct on all counts.

It makes absolutely no sense to raise the superannuation guarantee to 12% until the swag of structural flaws in Australia’s super system are fixed. To do so would blow an even bigger whole in the Budget: the 2009-10 Budget estimated that cost to revenue from raising super to 12% would grow “to $3.6 billion per annum in 2019‑20, due to the increase in the level of concessionally taxed contributions”. It would also reduce lower income earners disposable income, since super contributions are ultimately paid for by employees, and low income earners’ contributions are not concessionally taxed (more on this below).

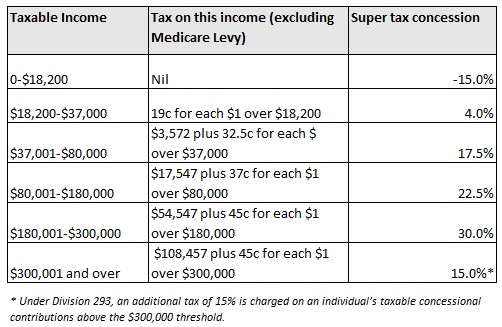

There is one blatant omission from O’Dwyer’s article, however. And that is the failure to even acknowledge that the current 15% flat-tax on super contributions are highly regressive and overwhelmingly favour higher income earners (see below table).

The Henry Tax Review agreed and recommended making superannuation concessions more progressive:

The structure of the existing tax concessions is inequitable because high-income earners benefit much more from the superannuation tax concessions than low-income earners…

Based on the 2008–09 tax rates, around 1.2 million individuals do not receive a personal income tax benefit from their concessional superannuation contributions. An additional 1.2 million people receive a concession of only 1.5 percentage points (Treasury 2008). This compares with around 200,000 taxpayers (those earning more than $180,000) who receive a concession on their superannuation contributions of 31.5 per cent…

Superannuation contributions should be taxed at a progressive but concessional rate. This would be achieved by treating employer superannuation contributions as income in the hands of the employee, taxed at marginal personal income tax rates. A flat-rate refundable tax offset, payable to the individual, would apply to these contributions to ensure that investing in superannuation retains its preferential tax treatment over other types of saving…

If raising ordinary workers’ retirement savings is the key objective of super, thus reducing reliance on the Aged Pension, then surely the first best option is to replace the 15% flat tax with a flat 15% concession (rebate for those earning under $18,200)?

This way, everyone that contributes into superannuation receives the same tax benefit, thus maintaining the progressiveness of the income tax system. It also means that lower income earners – those that are most likely to rely on the Aged Pension in retirement – would be better placed to build a retirement nest egg. Of course it would also limit the damage to the Budget – by both avoiding the need to raise the superannuation guarantee and lowering dependence on the Pension.

As I have argued previously, raising the superannuation guarantee to 12%, before fixing the underlying structural flaws, will merely heighten inequities already present in Australia’s retirement system. It will rob younger (and poorer) workers of much-needed disposable income and worsen the long-term sustainability of the Budget.

About the only winners from such a policy would be the superannuation industry, which would get to ‘clip the ticket’ on more funds under management and earn fatter profits. Perhaps this is why they are so strongly support raising compulsory superannuation and often lobby against fundamental reform. They smell easy money.