By Catherine Cashmore, a market analyst, journalist, and policy thinker, with extensive industry experience in all aspects relating to property. Follow Catherine on Twitter or via her Blog.

Nick Xenophon (along with other groups, such as the REIA,) is advocating a policy that will be responsible for making housing affordability worse.

He is using the Canadian “Home Buyer Plan” as an example to promote a similar idea in Australia. That is – allowing first homebuyers to raid their Superannuation account – ‘sold’ under the pretext of ‘helping them get onto the property ladder.’

The theory goes that to “progress” up this mythological ladder, buyers must bet their income and in this case, future savings, on a speculative process that translates into higher house prices, without thought for the next generation of required ‘property ladder’ participants, who will no doubt fall dependent on similar schemes, to keep the tide rising.

The procedure in Canada allows eligible buyers to withdraw up to C$25,000 tax-free from their retirement fund, on the condition that they pay it back over a 15-year period.

If they fail to do this, the amount withdrawn will be taxed as per the income earner’s tax bracket. Currently, 35 per cent of Canadians fall into this category however, according to the CRA, roughly one out of two – that is, 47 per cent – contributed less than the required repayment amount over the 2011 tax year.

These means, while the Government picks up the added income revenue windfall, buyers, buoyed on by a rent seeking culture that fools the public into believing such policies are designed to be ‘helpful,’ over stretch their budget, and in weak economic conditions, are left to carry the can.

In short – you borrow money from yourself at 0% interest and in doing so; lose 15 years of compounding ‘tax free’ interest with average returns in the order of 7%.

It’s notable that many low to middle-income individuals have inadequate funds to draw upon, therefore even assuming the scheme were to be effective, it’s limited in the difference it can make.

But the real ‘nub’ of the issue, which Nick Xenophon has failed to acknowledge, is that the Canadian Home Buyer Plan was never intended to aid affordability.

It was promoted by the real estate industry as a temporary measure, following the recession in the late 1980’s, to stimulate land values and benefit the FIRE sector, along with it’s economic offshoots – renovations, furniture, appliances, moving costs, tax revenue to government and so forth.

The FIRE sector has lobbied to keep in place ever since and also pushed for the threshold to be raised.

This is because most Western economies have constructed their tax and supply policies to reward real estate speculation over and above productive enterprise.

The process is assisted and abetted by a banking industry that seeks to lend against land as collateral, favouring the extraction of economic rent over and above extending loans for the purpose of productive enterprise.

Canadian residential real estate tripled from an estimated C$1.3 Trillion in 2000, to C$3.8 trillion in 2014. However, only C$550 billion of this was for renovation projects or new home building – the rest was pure inflation.

By the end of 2011, the Home Buyer plan had been used 2.6 million times, with total withdrawals adding up to around $27.9-billion – that’s $27.9 billion of additional credit, feeding into existing house prices.

Between 2005 and 2011, Canadian house prices rose 58%, while average income for 25-34 year olds, increased by just 6%.

The Royal Bank of Canada reports that detached housing now requires more than 80% of the median household income for mortgage payments in some of the country’s major cities.

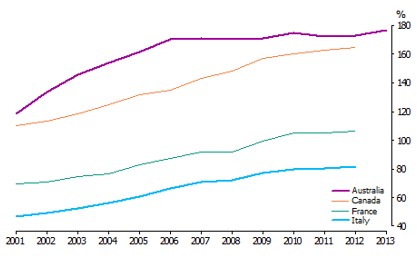

Household debt to disposable income in Canada is currently 163.2%, up from 129% at the peak of the boom in 2006 and sitting only a few degrees lower than the recorded level in Australia.

SIZE OF HOUSEHOLD DEBT COMPARED WITH ANNUAL INCOME in Australia, Canada, France and Italy. (ABS)

Mainstream economists like to focus on Government debt as a barometer of the heath of the economy. However, high and rising levels of private debt, as a consequence of such policies, constrain demand and eventually exceed the income and economic activity they helped create.

Nick Xenophon cites the Demographica Housing Affordability Report in his press release, however it’s clear he has not read it.

If he had, he would know that like Australia, Canada’s largest major markets are also rated as “severely unaffordable” – and by studying the ‘affordable markets’ such as Texas, or areas of Pittsburgh for example, Mr Xenophon would have a better understanding why these states avoided the harsh consequence of the GFC, and continue to generate healthy levels of economic growth.

Significantly, both cities have property/land tax and liberal supply policies that deter speculation – helping to keep real estate affordable, while investment is channeled into other areas of the local economy.

By contrast, Australia rewards speculation, allowing the geo-rent (the unearned gains) from rising land values to capitalise into the land price, year upon year, taxing income earners, instead of resource rents, which by design, distorts economic activity, housing supply policy, and subverts social justice.

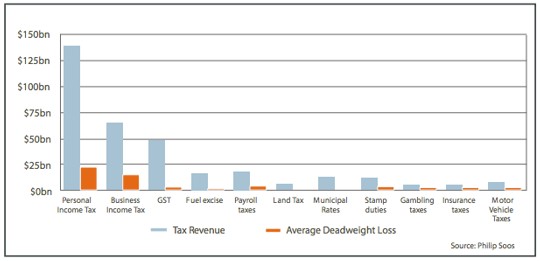

Ninety per cent of taxation revenue has distortionary effects, pushing up prices 23% higher than need be, while economic rents from land and natural resources have no such deadweight loss.

Never, throughout the course of history, has such a policy been sustainable.

At some point the productive capacity of the economy can no longer support the boom and the consequence, particularly for first homebuyers, can be particularly severe, as Australia’s history of land induced financial crises reveal.

However, when you appreciate how lucrative and wide spread this activity can be, it is very easy to see how policy fails us, and it’s additionally easy to see why a country with a plentiful supply of land like Australia submits its younger generation to a life time worth of debt slavery just to get onto the ‘property ladder.’