Jago Dodson, Professor of Urban Policy at at RMIT University, has called on the Victorian Government to tax inner city residents so that infrastructure and amenities can be expanded in outer areas. From The Age:

The lack of access to services and jobs for people living in the outer suburbs contrasts with that found by those in the established inner areas…

Now may be the time to redress that by taxing inner suburban residents and businesses who reap the liveability rewards of decades of state services investment, to enable similar government investment in services for the developing outer suburbs…

The great concentration of jobs and services within inner-urban areas is based on nearly 160 years of colonial and state government decision-making and capital investment. The 16 rail lines and 30 tram lines passing through Melbourne’s CBD are just one example.

The strong growth in CBD employment and housing implies a considerable benefit accrues to private parties from this extraordinary sunk capital, of which government receives at best a minor share.

This surplus may offer a taxation opportunity to redress outer-suburban underservicing in zones that have seen less historic State largesse.

A “spatial accessibility tax”, levied progressively on metropolitan properties and based on a relative composite measure of spatial access to employment, infrastructure and services, could offer a solution.

Taxing the inner suburbs to help improve services in the outer could have two principal effects. First, it might fund new state investment in suburban servicing, particularly public transport.

Second, it would raise the marginal cost of location in inner-suburban zones, offering greater incentive for businesses to locate in less valuable locations, such as outer-suburban activity centres and clusters.

Such a scheme would target the economic rent received by businesses based on historical government infrastructure and service investment.

The tax would fall on those most able to bear it, while the fixed nature of landed assets means that it would be difficult to avoid. If spatial accessibility is too abstract a concept, then an expanded land or property tax regime might be a simpler substitute.

Professor Dodson makes some valid points.

Buyers of new housing estates are unfairly penalised through large upfront charges for infrastructure which, in many cases, is not provided for years after their initial purchase (if at all). Buy contrast, buyers (and owners) of inner city homes are typically taxed less, whilst enjoying infrastructure and amenities either paid for by prior generations, or in the case of public transport (e.g. rail lines), the broader community.

That said, the proposed “spatial accessibility tax” seems far too complicated, and a simpler broad-based land tax in exchange for the abolition of stamp duties, liberalising of planning constraints (e.g. urban growth boundaries and restrictive zoning), and upfront development charges would achieve similar outcomes.

Abolishing stamp duties would encourage labour mobility by enabling workers to relocate closer to employment without incurring tens-of-thousands of dollars in taxes. The improved labour mobility would, in turn, assist with the creation of new employment centres in outer areas, as advocated by Dodson.

Abolishing stamp duty would also remove the unnecessary penalty applied to people that move to homes that better suit their needs, such as downsizing baby boomers and young growing families upsizing to bigger family-friendly homes. Such disincentives inevitably lead to an inefficient use of the housing stock, such as empty nesters occupying large homes with multiple spare bedrooms.

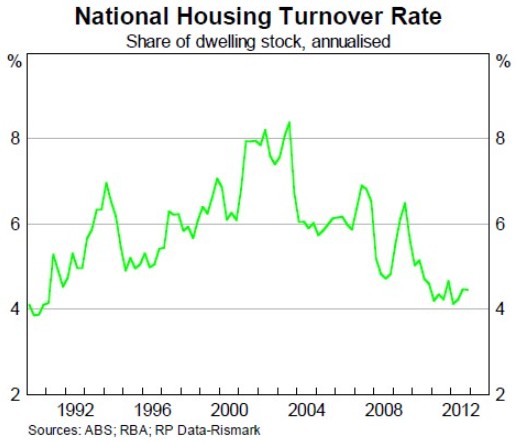

Stamp duties are also highly inequitable, unlike land taxes. As shown in the below RBA chart, between 4% and 8% of the housing stock is transacted annually. As such, we have a bizarre situation where a small minority of the population are paying taxes that support services for the whole community.

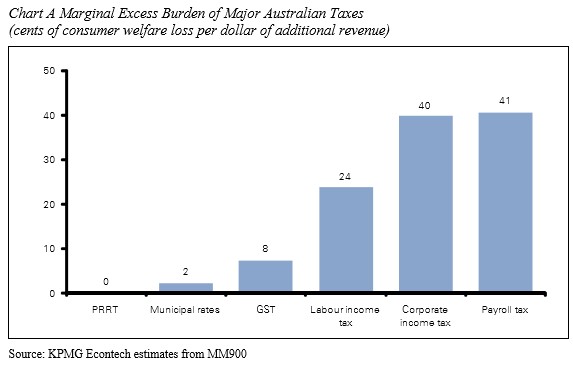

Taxes on land are also some of the most efficient going around, creating minimal “marginal excess burden” (i.e. a small loss in consumer welfare relative to the net gain in government revenue), according to the Henry Tax Review. This is because they are applied to a tax base that is completely immobile – land (see next chart). By contrast, the Henry Tax Review found the marginal excess burden of stamp duties to be a relatively high at 34%.

A broad-based land value tax (LVT) would also help make infrastructure investments self-funding for governments, since any land value uplift brought about through increased infrastructure investment (e.g. new roads, trains, etc) would be partly captured by the government via increased LVT receipts. Accordingly, governments would be more likely to facilitate development in outer areas, rather than act to restrict it in a bid to save on infrastructure costs.

Finally, an LVT would penalise land banking and vagrancy, effectively increasing the supply of land in the process and bringing new homes to market more quickly.

The options are there, and for the sake of both efficiency and equity, the federal government should work with the states through COAG to establish a timetable for reform to change the tax mix.