AMP’s Shane Oliver likes what he sees in profit season:

Sure it’s not been easy for non-financial industrial companies and there is still another week of results left with poorer performers often reporting late in the season. But the bottom line is that the June half earnings results are nowhere near as bad as many feared.

In fact, the profit results overall are looking pretty good:

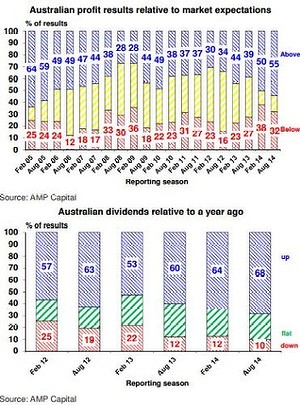

- 55% of companies have exceeded expectations (compared to a norm of 43%), which is the best result in nine years;

- 69% of companies have seen their profits rise from a year ago (compared to a norm of 66%);

- 68% of companies have increased their dividends from a year ago (up from around 60% in the last two years); and

- 59% of companies have seen their share price outperform the market on the day they released results, which is the best result in four years.

Key themes have been continued strength for resources (notably Rio, although BHP disappointed), banks doing well (with a good result from CBA), ongoing cost control making up for still soft revenue growth and strong growth in dividends reflecting investor demand for income and corporate confidence in earnings prospects.

Australian earnings growth for 2013-14 looks to be coming in around 12%, albeit down a bit from a few weeks ago as the BHP result saw a slight downgrade for resources. Resources are still leading growth though with a 27% gain, followed by banks up 9% and the rest of the market up around 5%.

Consensus expectations for 5% earnings growth in the current financial year look a bit low to me.

Good for you, Shane. I’d be prepared to bet you’re wrong. As iron ore undershoots market hopes, the margin squeeze for the major miners will turn much more serious.

Citi is more sober, from the SMH blog:

- There has been only a modest lowering in market earnings estimates from those a month ago, with FY14 earnings growth about 1% lower, and FY15 forecast growth little changed.

- For the companies that have reported, those with FY15 earnings downgraded by Citi analysts have exceeded those with earnings upgraded by more than 2:1, but for the larger companies estimates have been more stable

- Many companies have continued to find conditions relatively slow going, but forecast earnings have held up a little better, as some have pointed to signs of improvement (AMP, ORG, AIO), or progressed further on costs (AJZ, BXB, TOL, FBU), or flagged initiatives or transactions (asset sales, acquisitions, capital raisings) that should support earnings (QBE, WPL, AMC, ANN, ORG).

- However, against the modest downgrading of earnings, the market rise has taken the PE to ~15x forward earnings, a fuller valuation that might limit further gains in the near term, even though our end 2014 forecast for the ASX200 of 5750 would still seem achievable.

Yep, in the uber-stimulus world, so long as the S&P500 rises the ASX will just extend its price (as opposed to earnings) even if less so than the US bourse.