The second of the AIG monthly PMI series is out, the Performance of Services Index and it remains in contraction:

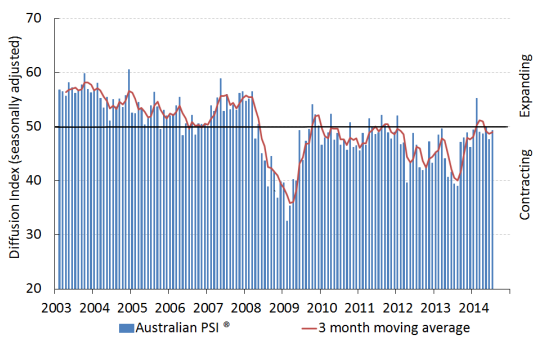

Sales and new orders growth drove a slight improvement in the seasonally adjusted Australian Industry Group Australian Performance of Services Index (Australian PSI®) in July. While remaining in contractionary territory for the fifth straight month, the index was up 1.7 points to 49.3 points. Readings below 50 points indicate contraction. The three month-moving-average for the Australian PSI® increased marginally, to 48.9 points.

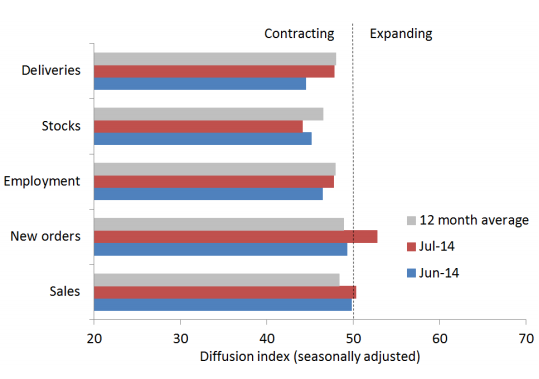

This month, both the sales and new orders sub-indexes in the Australian PSI® moved to slightly above 50 points, indicating a stabilisation or very mild expansion. In contrast, the supplier deliveries, stocks and employment sub-indexes all remained in contraction (below 50 points) in July, indicating that service businesses are still unwilling to commit more working capital or to hire more staff due to the relatively flat economic outlook.

Only three of the nine sub-sectors in the Australian PSI® expanded in July, as was the case in June. Growth remains concentrated in the health and community services (59.6 points), finance and insurance (64.0 points), and accommodation, cafes and restaurants (61.1 points) sub-sectors (three month moving averages). The other services subsectors all continued to contract this month.

The weakness of the local economy remains the key concern for respondents to the Australian PSI®. Ongoing uncertainties surrounding Federal Budget proposals for welfare, family payments and employment policy appear to be weighing on sentiment and dampening demand for both consumer and business services. The downturn in mining-related investment and construction activity this year has also reduced the flow of work to the business services sector.

The internal show a little more promise with new orders skipping into expansion:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.