Following his proclamation earlier this month that Australia is facing a “jobs boom”, Adam Carr appears to be in damage control and seeking to play-down the significance of this month’s poor labour force report from the ABS. From Business Spectator:

The fact is, we are witnessing a transition phase. A move away from the pre-GFC period from 2003-2008 which was characterised by a number of booms — a global growth boom, credit boom, housing booms, a consumption boom etc. That period was not the norm or the benchmark for comparison and I get the sense that policymakers and many commentators have forgotten this.

…moves in the unemployment rate and participation which are not driven by job-shedding are usually harmless. Seen in this context, a temporary lift in the unemployment rate is of little consequence — the unemployment rate is still historically low and jobs growth is robust — and set to surge following the spike in construction, business conditions and confidence.

Where the participation rate settles is anyone’s guess, but it is pointless fretting over the unemployment rate until trends in participation become clearer… we need more workers to replace baby boomers as they retire. It should be unanimous: unemployment is not the problem of today or tomorrow — finding sufficient workers is.

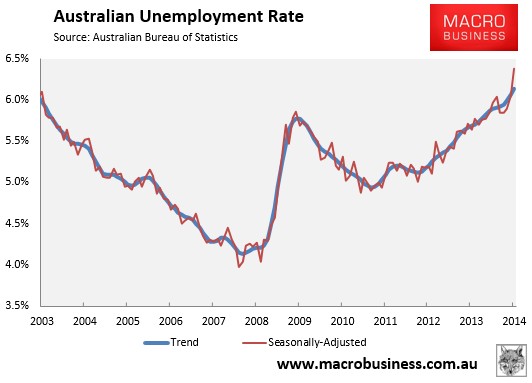

Let me state from the outset that I agree with Carr that last week’s large headline jump in the unemployment rate to a 12-year high of 6.4% was likely ‘noise’. As noted in my detailed report on the release:

Advertisement

Personally, I wouldn’t put too much emphasis on the large jump in the headline unemployment rate. The seasonally adjusted figures are subject to massive sampling error (see below table), which makes the results incredibly volatile. Better to focus on the trend data, which registered only a slight increase in the unemployment rate but a rising trend.

That said, I disagree that July’s unemployment data should be dismissed. Trend unemployment is also rising and hit the highest level since November 2002 in July, which warrants concern (see next chart).

Advertisement

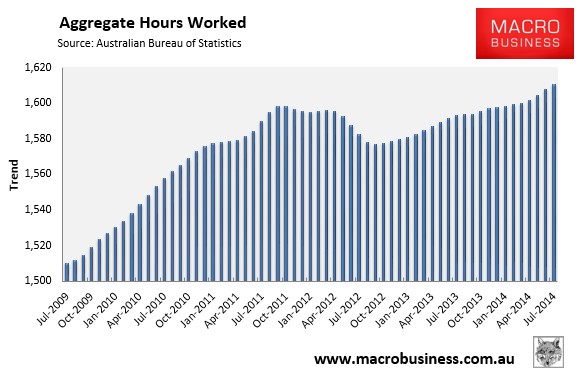

Aggregate hours worked have also recorded minimal growth since late-2011, despite strong growth in the labour force due to ongoing high immigration (see next chart).

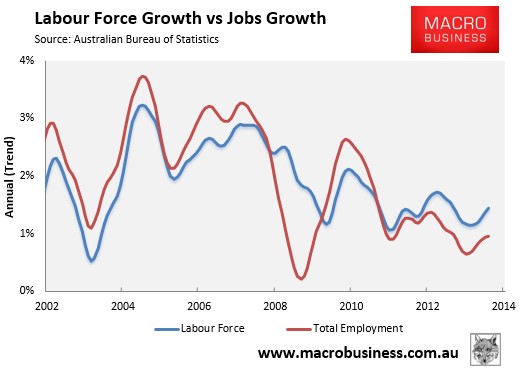

Most importantly, since the GFC, the economy has been too weak to generate sufficient jobs to offset the growing population – a stark contrast to the corresponding period prior (see next chart).

As a general rule, our adult civilian population grows by around 1.6% every year (although it has been slightly higher than that for most of the past eight years). If employment doesn’t grow faster than population, unemployment is likely to rise…

In the past year employment grew by just 1%, and it has now been 36 months since annual employment growth was above 1.6% – the second longest streak ever behind the 40 consecutive months between August 1990 and December 1993.

Advertisement

If that’s not a weak labour market, and cause for concern, I don’t know what is.

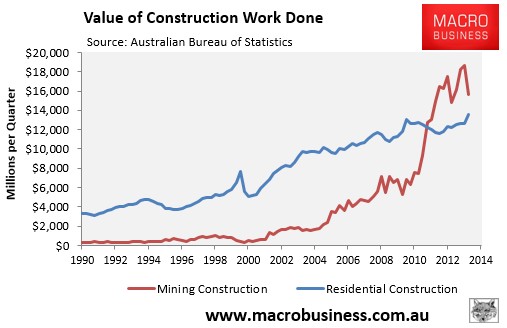

Carr’s claim that employment is “set to surge following the spike in construction, business conditions and confidence” is also dubious. Again, he might like to look at the below chart comparing mining construction against residential construction, and then think long and hard about whether his so-called ‘construction boom’ will be enduring:

Advertisement

I should once again highlight the report released last year by the RBA, which revealed that mining-related activities accounted for 10% of total employment in 2011-12, with mining-related employment rising sharply since the mid-2000s:

“We estimate that the resource economy accounted for around 18 per cent of gross value added (GVA) in 2011/12, which is double its share of the economy in 2003/04. Of this, the resource extraction sector – which we define to include the mining industry and resource-specific manufacturing – directly accounted for 11½ per cent of GVA. The remaining 6½ per cent of GVA can be attributed to the value added of industries that provide inputs to resource extraction and investment, such as business services, construction, transport and manufacturing. This ‘resource-related’ activity is significantly more labour intensive than resource extraction, accounting for an estimated 6¾ per cent of total employment in 2011/12, compared with 3¼ per cent for the resource extraction sector…

The share of total employment accounted for by the resource economy is estimated to have doubled since the mid 2000s. Around two-fifths of this growth reflects the expansion in resource investment, which has increased demand for labour in resource-related construction and other industries that provide inputs to these investment projects…

As noted above, roughly two-thirds of mining-related employment in 2011-12 was investment-related – jobs that will mostly disappear once the large resource projects are finished. Viewed in this light, residential construction appears hopelessly outgunned by the pending sharp drop-off in mining investment, which will intensify once the large LNG projects in Gladstone, Western Australia and the Northern Territory are completed over the next few years, taking with them many thousands of jobs.

Advertisement

And then there is the shuttering of Australia’s automotive assembly industry by 2017, which will likely cause the loss of tens-of-thousands of assembly and component manufacturing jobs.

One thing I do agree with Carr on is that the pre-GFC economy was inherently unsustainable, and that “those unemployment rates we saw around 4 per cent to 5 per cent can’t be viewed as rates consistent with sustainable growth”. However, this view works against his whole “jobs boom” thesis. With mining and manufacturing employment set to decline, what will fill Australia’s jobs void if a “credit boom, housing booms, a consumption boom etc” are not viable options?

This is precisely why Carr’s panglosian view on jobs is not justified.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.