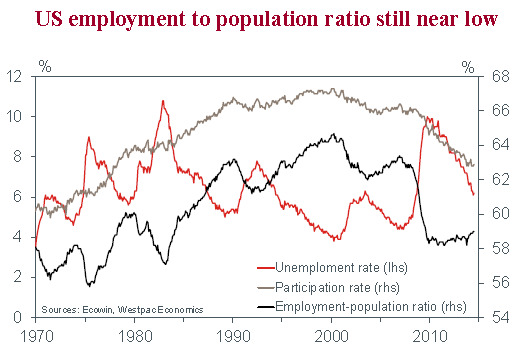

With the unemployment rate now having declined from 10% to 6.2%, the July 29–30 meeting saw the FOMC adjust their labour market benchmark from a (now not) elevated unemployment rate to the much more amorphous concept of “underutilization” or labour market slack. This shift highlights the degree of unease amongst FOMC participants over the quality of the labour market recovery and the potential consequences for inflation.

These two factors were the focus of Chair Yellen’s Jackson Hole address. Overall, Chair Yellen and the FOMC are willing to allow cyclical healing subject to inflation remaining benign, but are cognisant that there may be little they can do to heal some deficiencies.

It is clear the FOMC sees there as being three primary components to the labour market slack debate: the trend decline in labour force participation; the prevalence of part-time (and temporary) workers; and the relationship between different labour market flows, specifically job vacancies, hires and quits. What matters in each instance is whether the weakness is being driven by cyclical factors which can be healed through accommodative policy, or secular, structural trends outside of the FOMC’s remit.

On labour force participation, Chair Yellen made clear that, while the decline in participation started well before the recession and was in part the result of the ageing population, there were clearly other factors at play: i.e. the drive for further education, increased disability claims and ‘other’, read (cyclical) worker discouragement. While increased years in education and higher rates of disability (owing to ageing) could be regarded as structural trends, Chair Yellen saw them as having significant cyclical components, with both impacted materially by the recession. The expectation is that, as prospects improve, participation will rise, boosting capacity and dampening inflationary pressures.

On the prevalence of part-time employment, again Chair Yellen highlighted that this was partly due to unfavourable structural trends: the move away from goods to services production where part-time work is more prevalent; and the loss of “middle-skill” jobs, replaced by low-skill (part-time) positions. These are not necessarily phenomena the FOMC believe it can set right. Rather, they are focused on the potential inflationary consequences of more limited productive capacity. Here the 5% of the labour force that is employed part-time for “economic reasons” (reported by Chair Yellen as abnormally high) is the critical factor for policy. On this metric, there remains cause to maintain accommodation in pursuit of healing.

A great deal of information on the health of the labour market can also be gleaned from labour market flows. The continued rise in job vacancies and the ‘quit rate’ have both been seen as notable positives for the health of the labour market – the former points to a greater hiring appetite amongst employers, the latter alludes to more confidence amongst employees. But, against these positives, the pace of hiring remains depressed by soft aggregate momentum.

All told, one gets the feeling that Chair Yellen and ‘most’ FOMC members continue to believe there is a substantial degree of cyclical weakness in the labour market which could be healed with time and momentum, subject to the prevalence of inflation and wage pressures.

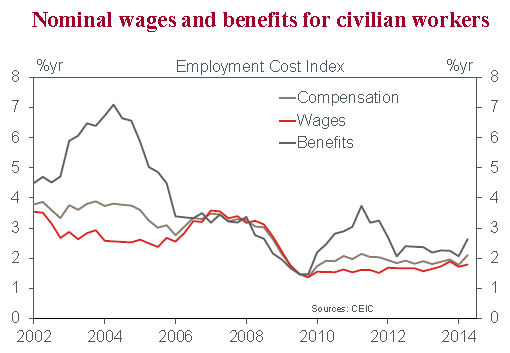

While the wages discussion opened with a nod to apparent weakness, Chair Yellen went on to highlight three reasons as to why this weakness could (at least in part) be dismissed. The inability of firms to cut wages as much as they would have liked during the recession and a secular decline in real unit labour costs (driven by globalisation and a greater corporate profit share) were both seen as factors outside of the FOMC’s control, which could be biasing down wages growth and misrepresenting labour market slack. In addition, there is a concern that reduced participation could (albeit in a transitory manner) see inflation pressures develop, even if slack remains present.

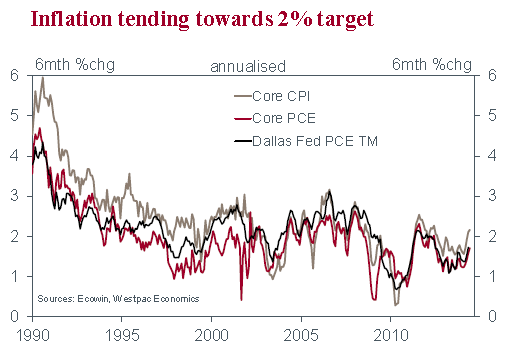

Reading between the lines, it becomes apparent that the FOMC is decidedly uncertain over the outturn. But, whereas in the past they have given signs of weakness the benefit of the doubt, the cumulative improvement in the level of jobs and activity is progressively leading to a more balanced, inflation-dependent approach. This is not to say they will not permit further healing if inflation pressures remain obviously benign; but if inflation (actual and expected) trends to the 2% target or above, a tightening in the stance of policy will quickly come into frame. This is regardless of the growth performance of the economy, and any enduring secular deficiencies in the underlying health of the US economy.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.