Tim Toohey on the SoMP:

The August Statement of Monetary Policy was an interesting mix of significant shifts in the RBA growth and inflation forecasts and more incremental shifts in the tone of the accompanying text. Our approach has historically been that the RBA’s real intent in the Statement of Monetary Policy is signaled by its forecast changes rather than its text. The key question is does this add up to a reinstatement of an easing bias? We think the answer is that it is another step along that path, however, wewould prefer to see the RBA Governor confirm this in coming weeks. From a GDP perspective, the downgrade of annual economic growth of 25ppts through December 2014 through to December 2015 may not appear too meaningful in isolation, however, the RBA downgrade of non-farm GDP growth of 50ppts in 2015 and a 50ppts reduction off the high end of the June 2016 range is meaningful. From an inflation perspective, downgrade in underlying inflation by 50ppts by mid-2015 will be the key focus, and takes the RBA’s underlying inflation forecast into alignment with our forecasts. The larger downgrade in headline CPI of 75ppts in the year to December 2014 and June 2015 in addition to a 25ppt reduction in the year to December 2015 indicate that not only does the RBA expect the full impact of the Carbon tax removal to be passed on, it expects general inflation pressures to be subdued. In short, the RBA has outlined a growth and inflation profile that enables it to lower interestrates in 2H2014. We continue to hold our forecast of a September cut, and note that it is historically unusual for the RBA to undertake meaningful shifts in its key forecasts and leave interest rates unchanged in the subsequent meeting. We will continue to assess the risks to this view in coming weeks, however, we continue to believe an interest rate easing is likely through 2H14.

It could come in September. The meet is the day before Q2 national accounts which are likely going to show a growth wipe out. I still say they’ll move to an easing bias first and then cut the month after so my bet remains October or November. Q3 CPI is out late October so November also has that to recommend it given the release will likely show inflation falling fast. A little longer pause to let housing slow will help too.

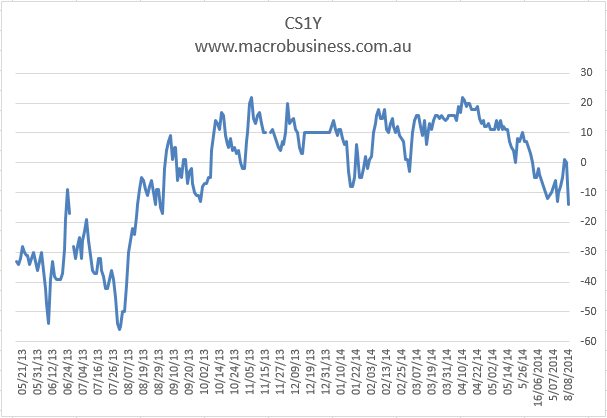

Interest rate markets priced in 14bps in cuts in the next 12 months on Friday, a new low.