From Stephen Walters at JP Morgan today comes a reasonable summary of the competitiveness challenge facing Australia. I obviously disagree on the dollar defeatism but aside from that it’s pretty right.

Australia has slipped in the rankings for global trade competitiveness. World Economic Forum (WEF) data show export-oriented Australia now ranking 21st on this scale, down from 14th in 2009—the first time in 34 iterations of the WEF’s report that Australia has finished outside the top 20. Australia now is less competitive than New Zealand, Singapore, Japan, Canada, the US, Qatar, Iceland, and a brace of EU countries, including Germany, France, and Belgium.So what has changed since 2009?

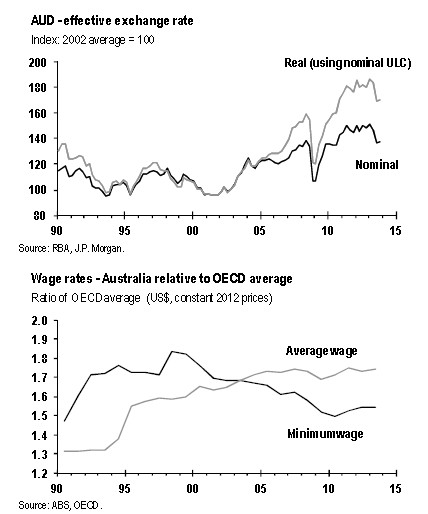

To start, Australia’s soaring terms of trade has led to persistently elevated AUD. And unit labor costs, which already were high, have risen faster in local currency terms than global averages, owing to sluggish productivity. Australia’s minimum wage, rising again this week, is the world’s second highest, behind only Luxembourg, while Australia’s average wage is70% above the OECD average. In addition, the profit share of GDP has risen for decades as local exporters, via margin expansion, unwittingly helped price themselves out of global markets.

AUD unlikely to provide much relief

The main avenue by which a country can restore trade competitiveness is via a lower real exchange rate, which we measure using nominal AUD and changes in local currency unit labor costs. The real exchange rate can go down in two main ways, one relatively easy, the other more difficult. First, the nominal exchange rate can fall, reducing the relative price of Australian exports in world markets. According to the RBA, the 50% nominal appreciation of AUD accounts for two-thirds of the deterioration in Australia’s competitiveness since 2001. AUD strength reflects rising commodity prices and faster capital inflows attracted by the mining investment boom and high relative returns on portfolio investment.

Our forecast, however, anticipates only modest exchange rate relief, partly because Australia is still an attractive destination for offshore investment—Australia’s sovereign bond market is part of the small group rated AAA by all three major rating agencies. Of these, Australia has the highest interest rate returns. Partly for this reason, and despite lower commodity prices, our forecast assumes nominal AUD merely drifts down from the current 94 US cents to 90 US cents by mid- 2015. A similar nominal depreciation in TWI terms would also damp the real exchange rate, but not likely enough to reverse the recent competitiveness decline.

Lower wages, anyone?

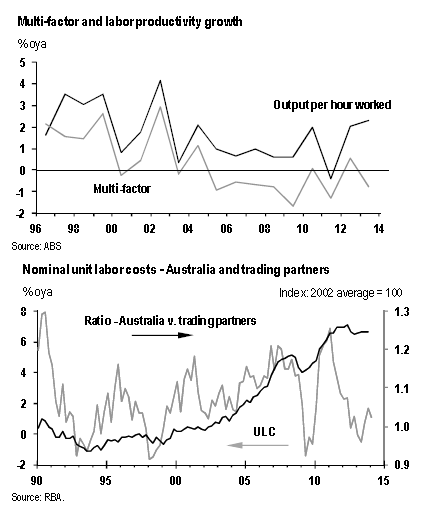

The second, more difficult, way to achieve a lower real exchange rate is via a sustained reduction in real unit labor costs. This can be achieved via slower nominal wage growth (or even falling wage levels), faster productivity growth, or a combination of both. The RBA estimates that higher unit labor costs have delivered the remaining one-third of the deterioration in Australia’s competitiveness over the last decade. In fact, the country’s ULC rose 25% faster than those of its trading partners in the decade to 2011 (first chart).

Growth in nominal wages in Australia has been sliding for some time as slack in the labor market has accumulated. In fact, annual growth in nominal wages now is below annual inflation, so real wages are falling for the first time since 2009. Unsurprisingly, the steepest falls in nominal wage growth have been in mining and related sectors, where previous gains were largest. Declines in real wages, however, including most recently during the great recession, when inflation spiked as AUD dived and nominal wage growth was weak amid rising joblessness, usually do not persist for long.

Indeed, our model of labor costs, based on the relationship between the employment to population ratio and nominal wages, indicates that wage growth probably is close to a floor.

With inflation set to drift lower, owing mainly to the persistence of high AUD and weak nominal wages growth, owing to a further modest rise in the unemployment rate as growth in the economy stays below potential, real wages are set to rise, not fall. This should act to partly offset the small competitiveness gain achieved via the expected modest decline in the nominal exchange rate.

What about falling wage levels?

There are pockets of the mining sector where nominal wage levels are reported to be being bid down by as much as 15%, and additional savings are being found in non-base salary arrangements like penalty rates and meal allowances. In these cases, trade unions apparently accept that lower wage levels may be in the longterm interests of their members exposed to surplus labor in mining-related industries. Workers’ tolerance of lower wages, though, is even more limited than of falling wage growth, particularly with the recent budget aiming to cut welfare payments and raise taxes.

Labor market flexibility compromised

During comparable terms of trade booms in the 1920s, 30s and 50s, Australia’s currency (the pound until 1966) was pegged variously to gold, sterling, USD, and/or a basket. This neutralized the potential pressure valve of depreciation when the boom ended, but led to broad-based wage increases and inflation, necessitating higher interest rates and fiscal austerity. With AUD unable to adjust, the result usually was a period of recession and rising unemployment.

In 1983, the Australian dollar was floated and earlier structural reforms meant the labor market had become more flexible. So, in the latest boom in the 2000s, rapid wage gains in mining didn’t spill into non-mining sectors. The previous Labor government’s re-regulation of the labor market from 2008, however, strengthened centralized wage fixing and buttressed the role of trade unions, as well as providing a more comprehensive safety net. Now, then, Australia ranks54th in terms of labor market flexibility in the WEF tables, down 12 places from 2009 and in the 130s (of 148 countries) for the rigidity of hiring and firing practices and rigidity of wage setting. This increases the risk of sector-specific wage gains spilling elsewhere, making it more difficult to sustain generalized wage restraint.

The answer, then, is higher productivity

The constraints posed by stubbornly high AUD and a floor for wage growth mean the answer to the competitiveness challenge lies in productivity, in our view, notwithstanding the new rigidity in the labor market. For most of the mining investment boom, labor productivity growth reached multidecade lows, so growth in unit labor costs accelerated.

Cyclical labor productivity growth at least has accelerated in the last year (first chart) as large mining projects have moved from the construction to production phase. This will continue as more mining projects move into production. In our view, however, Australia’s global competitiveness can only be improved through difficult reform that neither end of the political spectrum currently seems willing to risk. Indeed, policy-makers have not yet undertaken the difficult reforms needed to reverse the more virulent and persistent structural decline in multi-factor productivity. The current Coalition Government unwinding Labor’s re-regulation of labor market practices more quickly could be a great place to start.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.