From our old friend Chris Joye this arvo:

The elevated inflation results in the June quarter...demolishes the case for a near-term cut.

And with house price growth compounding at 9.5 per cent in 2014 (or triple wages growth)…the RBA is going to have to eventually normalise the cheapest borrowing rates in history. The curve-ball in this calculus is Australia’s currency, which has remained lofty despite declining commodity prices.

The interest rate implied by the 3-year government bond futures price jumped from 2.55 per cent to 2.65 per cent…the 50 per cent (pre-release) probability of an RBA cut by December priced into interbank futures was slashed to 30 per cent…

…UBS strategist Matt Johnson….believes the short end of the yield curve “appears mispriced in this context”…“CBA are now advertising a 5 per cent, five-year fixed-rate home loan product. As effective borrowing rates are eased this takes the onus off the RBA having to do more work.”

HSBC chief economist, Paul Bloxham, concurs that “with inflation firmly in the top half of the RBA’s target band and the housing market continuing to boom – and it is booming – the RBA is not going to be cutting rates further”.

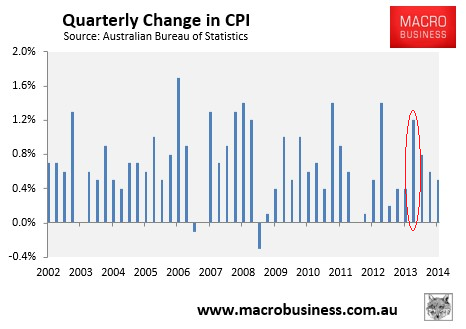

The hawks are back then. Am I moved? Nope. Look at this chart:

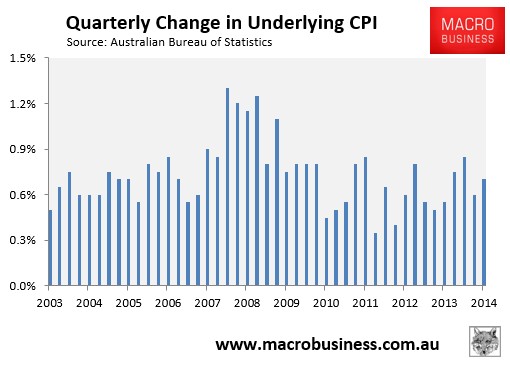

I’ve circled the next quarterly number that will drop out of the series in Q3. That’s a 1.2% spike in Q3 2013 that will be replaced by something more like 0.5% (or lower if the dollar bulls stay in control). The effects on the trimmed mean and weighted medians are not so obvious but they are still there. Here’s their average:

Now add the carbon price repeal. It added roughly 1% on the way up. It will be less coming down but still material. In short, barring a dark miracle, annual headline inflation is going to crash next quarter, the analytic measures will likely moderate and the context will be weakening price pressures (that I don’t deny are apparent).

As well, I’ve already illustrated today that in aggregate there are no out-of-cycle rate cuts happening at the banks. Yes, housing is bubbling and needs a lid, the quicker the better. But the RBA has made it clear that it is not going to provide it. APRA will have to.

The RBA may feel it needs to wait for the next CPI before it cuts again but there’s is no apparent need for it (within the context in which these debates transpire!) The short end is not mispriced. The dollar overreacted, largely because it’s already priced the cut and any doubt will send it north, as I said this morning.