The draft report of the Murray Inquiry into Australia’s financial system has taken aim at the efficiency, equity and sustainability of Australia’s superannuation system.

The first target is superannuation fees, which are far too high by global standards and are an unnecessary drain on Australia’s retirement savings:

Advertisement

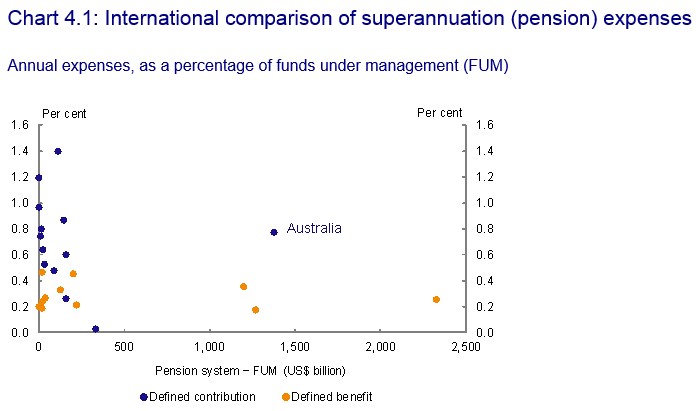

The operating costs of Australia’s superannuation funds are among the highest in the Organisation for Economic Co-operation and Development (OECD), and the Super System Review concluded superannuation fees were “too high”. The Grattan Institute estimates fees have consumed more than a quarter of returns since 2004. Although the Inquiry notes the difficulties of comparing costs or fees across funds, especially internationally, the evidence suggests there is scope to reduce costs and improve after-fee returns (see Chart 4.1).

Fees can significantly affect retirement incomes. The Super System Review found that reducing fees by around 40 per cent — or 38 basis points22 — for the average member would increase their superannuation balance at retirement by approximately $40,000 (or 7 per cent)…

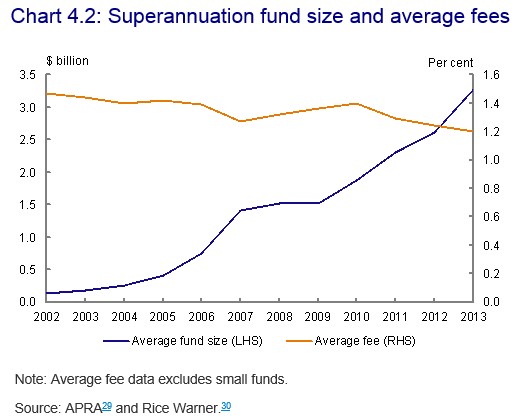

The Super System Review found that fees had not fallen in line with what could have been expected given the substantial increase in scale (Chart 4.2)…

The Inquiry’s criticism of superannuation fees is justified.

If superannuation was a well functioning and competitive market, average fees would have fallen as the value of funds under management has risen. After all, it should not cost ten times more to manage $1 billion of funds under management than it does to manage $100 million.

Yet, despite the huge explosion of superannuation balances since the superannuation guarantee (compulsory super) was introduced in 1993, average fees have barely changed.

Advertisement

All of which suggests that Australia’s superannuation funds are not just inefficient, but are gouging members – helped along of course by our system of compulsory contributions, which has provided the industry with a “sheltered workshop” within which to operate.

The Inquiry also warns about the strong growth of self-managed super funds (SMSFs) and leverage, which could pose risks to the financial system and retirement savings:

The use of leverage in superannuation funds to finance asset purchases is embryonic but growing. The proportion of SMSFs with borrowings increased from 1.1 per cent in 2008 to 3.7 per cent in 2012. The average amount borrowed increased over this period from $122,000 to $357,000. Total borrowings in 2012 were over $6.2 billion. More recently, Investment Trends research found that, over the year to April 2014, the number of SMSFs using geared products increased by more than 11 per cent to 38,000…

If allowed to continue, growth in direct leverage by superannuation funds, although embryonic, may create vulnerabilities for the superannuation and financial systems.

Advertisement

It also recommends removing the ability of super funds to leverage:

The general prohibition on borrowing in superannuation was introduced for sound reasons. Although levels of direct leverage in the superannuation sector are low, they are increasing. Removing direct leverage in superannuation is consistent with the concept that superannuation tax concessions should apply to funds that have been saved and not borrowed. There are ample opportunities — and tax benefits — for individuals to borrow outside superannuation.

This is another sound observation and a worthwhile reform. Superannuation is supposed to be a retirement savings system, not a speculative vehicle. Funds should not be allowed to gear-up into assets, period.

Advertisement

The Inquiry also rightly questions the sustainability and equity of superannuation concessions, which will become an increasing drain on the Budget over time:

As the population ages, the cost to Government of the current retirement income system is likely to be a major source of pressure to change policy settings.

…evidence raises questions about whether the current policy settings are efficiently targeted and robust.

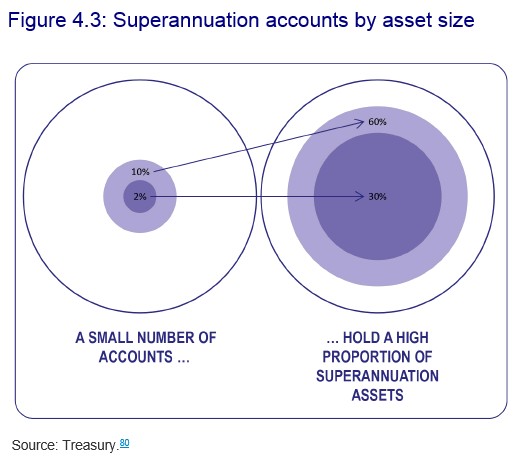

For example, the large number of individuals with very large superannuation balances suggests the superannuation system is being used for purposes other than providing retirement incomes (Figure 4.3). The large number of accounts with assets in retirement in excess of $5 million could each receive annual tax concessions more than five times larger than the single Age Pension.

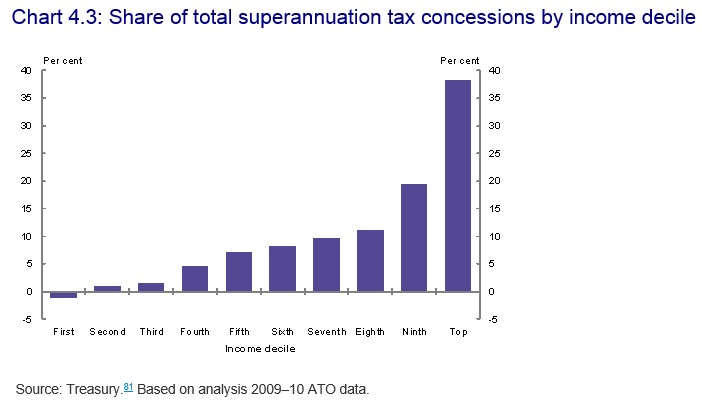

Furthermore, the majority of superannuation tax concessions accrue to the top 20 per cent of income earners (Chart 4.3). These individuals are likely to have saved sufficiently for their retirement, even in the absence of compulsory superannuation or tax concessions. Some stakeholders question whether this is equitable. It is not clear that superannuation tax concessions for this income cohort will significantly reduce future Age Pension costs…

The combination of population ageing and the projected growth in superannuation assets increases the urgency and importance of getting the right policy settings in place. Policy settings should be designed to minimise the need of future governments to change them to maintain confidence and trust in the system. Some of the settings could be considered as part of the Tax White Paper process.

Finally, the Inquiry suggests that retirees should be required to take their super as an annuity income stream rather than a lump-sum, decreasing longevity risk:

Advertisement

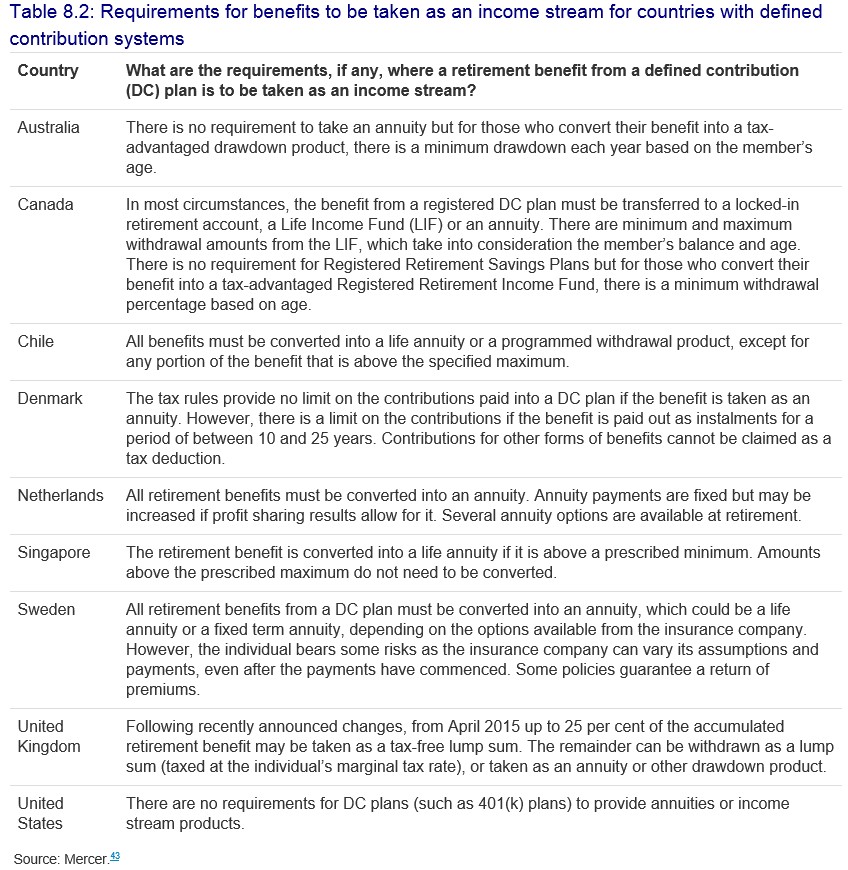

Australia is unusual in neither mandating nor encouraging the use of income streams with longevity protection in retirement (Table 8.2). Information provided to the Inquiry by Centre of Excellence in Population Ageing Research (CEPAR) notes that Australia “is the only developed economy with mandatory retirement saving to have no decumulation structure”…

Policy settings should ensure that retirees can manage their accumulated balances in a way that improves retirement income and risk management, without transferring an excessive amount of longevity risk to the Government…

It may be appropriate to have policies that discourage lump sums. Several submissions recommend restricting or discouraging lump sum benefit payments. For people with very small superannuation balances, lump sums may be the most appropriate way to draw down their benefits.

To be effective, the tax and social security implications of decisions may need to be significant. The fiscal costs of additional incentives would need to be appropriately targeted and offset by savings elsewhere to avoid increasing the overall cost of the retirement income system to Government.

Again, hard to disagree. The exclusion of the family home from the assets test for the aged pension, combined with the ability to withdraw one’s super as a lump-sum (instead of an annuity), creates an incentive for households to borrow to purchase an expensive home in the lead-up to retirement, retire at 60, withdraw their super tax-free as a lump sum, use the money to pay-off their mortgage or to fund consumption, and then go on the aged pension from 65 years of age.

In such instances, the taxpayer is left wearing the cost of superannuation concessions throughout the individual’s working life, and then again once that same individual goes on the aged pension. It is a strategy that, while making sense for the individuals concerned, compromises the integrity, fairness and sustainability of the retirement system which, after all, was supposed to relieve pressure on the Budget, not exacerbate it.

Advertisement

Overall, the Murray Inquiry has made some sensible observations and comments about Australia’s superannuation system.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.