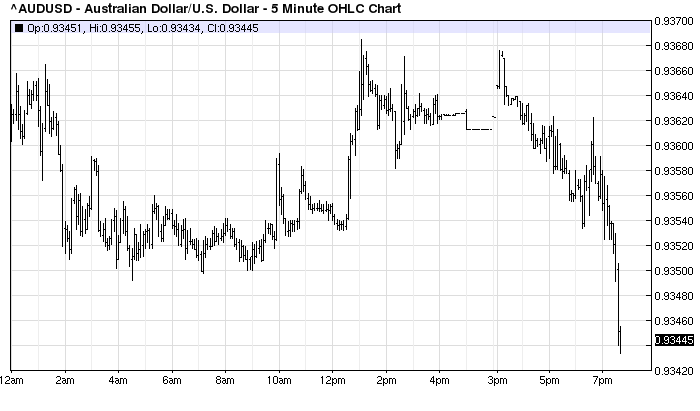

The Australian dollar has opened weaker today and appears to be threatening last week’s lows already:

The low last week was at $93.3 but as I wrote then, I don’t think that markets have fully absorbed the significance Captain Glenn’s speech. In it he declared openly for the first time that:

But lest there be any uncertainty about this, let me be clear, again, that the exchange rate remains high by historical standards. There is little doubt that significant parts of the trade-exposed sectors still find it quite ‘uncomfortable’: it continues to exert acute pressure for cost containment, productivity improvement and business model change. When judged against current and likely future trends in the terms of trade, and Australia’s still high costs of production relative to those elsewhere in the world, most measurements would say it is overvalued, and not by just a few cents. Of course, we live in unusual times, with interest rates at the ‘zero lower bound’ in several major jurisdictions. Nonetheless, we think that investors are under-estimating the likelihood of a significant fall in the Australian dollar at some point.

Some use the ‘B’ word, sometimes followed by calls for interest rates to be higher…The Bank has not seen developments in the housing market as warranting higher interest rates than the ones we have had, in the current circumstances.

This, and his reluctant endorsement of macroprudential after the speech, is as close to a Draghi moment – a commitment to do whatever it takes to get a market outcome – that we’re going to get from the laconic Glenn Stevens. It appears to have been well timed. A story today from the WSJ suggests that this week may see more downward pressure on the currency. The first is a take on recent rises in food inflation at WSJ:

…The consumer price of ground beef in May rose 10.4% from a year earlier while pork chop prices climbed 12.7%. The price of fresh fruit rose 7.3% and oranges 17.1%. But prices for cereals and bakery products were up just 0.1% and vegetable prices inched up only 0.5%.

The U.S. Department of Agriculture predicts overall food prices will increase 2.5% to 3.5% this year after rising 1.4% in 2013, as measured by the Labor Department’s consumer-price index.

The uneven rise points to disparate forces affecting food prices. Drought in Oklahoma and Texas is driving up cattle prices. A disease known as porcine epidemic diarrhea virus has killed millions of piglets and contributed to higher hog prices. A disease known as citrus greening is killing Florida’s orange and grapefruit trees, driving up citrus prices. Most of the shrimp eaten in the U.S. comes from Southeast Asia, where a bacterial infection has devastated stocks. Coffee prices have risen this year due to a drought in Brazil.

These are classic “look through” episodes of inflation and will not spook the Fed despite its favoured measure of inflation, the PCE, jumping to 1.8% recently. As Janet Yellen said recently:

GREG IP. Madam Chair, Greg Ip of the Economist… How would the Committee respond if inflation did temporarily move above target in the near term before you achieve full employment?Your colleague John Williams and the IMF have both suggested that the Committee might consider allowing inflation to temporarily overshoot because that might achieve a faster, larger improvement in employment.

CHAIR YELLEN. So with respect to the question of overshooting, let me start by saying that inflation continues to run well below our objective, and we’re still some ways away from maximum employment. And for the moment, I don’t see any tradeoff whatsoever in achieving our two objectives. They both call for the same policy—namely, a highly accommodative monetary policy. …

Now, quite some time ago, the FOMC adopted, and we reaffirmed just in January, a statement on our longer-run goals and policy strategy. And what that statement said is that, first of all, whenever either inflation or employment are away from their preferred or mandate-consistent levels, it will always be the FOMC’s policy to make sure that we get back to those target levels over the medium term. But a principle that’s embodied in that statement is that the Committee will follow a so-called balanced approach in deciding on its policies. And, essentially, that means that when we see some conflict between achieving the two objectives, that we would consider in deciding on a policy just how far we are from achieving each of the objectives. And if the distance from achieving an objective is particularly large, it would be consistent with a balanced approach that we would tolerate some movement in the opposite direction on the other objective.

However, it is enough for some senior market players to be tightening their horizons for the first rate hike. Goldman Sachs has today brought forward six months its forecast for the first tightening (if you can caall it that) to Q3 2015. Forexlive has more:

- Despite the striking weakness in the Q1 GDP report, we remain quite confident that the US economy is accelerating to an above-trend pace

- Our current activity indicator (CAI) is running at a healthy 3.5%

- The rapid growth in the CAI in June is particularly encouraging because the distortions from the cold winter should by now have mostly run their course

- The acceleration is most visible in the labor market – unemployment rate has continued to fall more rapidly than expected… the decline is now entirely due to faster job growth as opposed to lower labor force participation (unchanged since December)

- Inflation numbers have also surprised on the upside over the past few months

- Financial conditions have eased further: Treasury yields remain low, credit spreads remain tight, and equities continue to make new highs