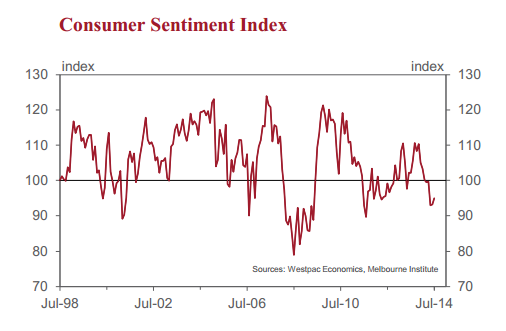

The Westpac Melbourne Institute Index of Consumer Sentiment increased by 1.9% in July from 93.2 in June to 94.9 in July.

The Westpac Melbourne Institute Index of Consumer Sentiment increased by 1.9% in July from 93.2 in June to 94.9 in July.

This is another disappointing result for the Index. We had expected a stronger bounce back in the Index following its 7% tumble in the aftermath of the Commonwealth Budget in May.

The Index is now only 2% above that recent low in May. It is also 14% below the recent high in November 2013 and 10% below the average print in 2013.

The Reserve Bank kept rates on hold for the eleventh straight month and continues to signal that rates will remain steady for time. Media speculation on rate hikes has dissipated. Markets are even factoring a 50% probability of a rate cut by early 2015. Consequently interest rates are unlikely to be a factor behind the slump in confidence.

For now, however, our best guide as to the driver of current sentiment remains the results from the June survey on news recalled. This part of the survey is only conducted quarterly. A record 74% recalled news on ‘Budget & taxation’, the highest ever recall rate for this issue, swamping other news items such as ‘economic conditions; ‘employment’; ‘interest rates’ and ‘international conditions’. The recollections last month were extremely unfavourable and are likely to have remained that way.

A significant number of the unpopular savings measures in the Budget appear to be opposed by the Opposition and the minority parties in the Senate. It may be some time before households get some clarity around the final state of the Budget. We have seen a 0.5% contraction in retail sales in the March–May period and this uncertainty may be a key reason for that slowdown.

While the July result was disappointing overall, there were some encouraging signs amongst the components of the Index.

Views around family finances improved. The sub-index tracking assessments of ‘family finances relative to a year ago’ improved by 1.9%. The sub-index on the ‘one year outlook for finances’ posted an even stronger 12.3% rise although that still did not compensate for the record low reading post Budget for that component which plunged 23% in May. The sub-index tracking views on the ‘economic outlook over the next 12 months’ improved by 3.9% although the five year outlook sub-index deteriorated by 3.8%. Durable goods retailers will be disappointed that the sub-index tracking views on ‘time to buy a major household item’ fell by 2.1%.

A significant negative from the immediate post Budget response was the wide 19.1 point margin between the current conditions index and the expectations index, indicating that consumers were expecting a sharp deterioration in their finances and the economy.

The margin has now contracted to 12.2 points indicating that households are not as stressed about a deteriorating economy and finances as they were immediately post budget.

Confidence in the labour market remains stubbornly weak. The Unemployment Expectations Index registered a modest fall of 0.3% – lower reads indicate reduced concern around the labour market. The index has held within a narrow range all year and although it is 5% below its March peak, it remains 6% above the average for 2013. Despite a marked improvement in jobs growth since the start of the year and ongoing low interest rates, confidence in the labour market remains weak and fragile. The concern here is how businesses respond with their employment plans to the recent loss of momentum in spending.

Views on housing are mixed with a clear tension between the outlook for house prices and assessments of ‘time to buy a dwelling’. The latter showed a promising 11.4% bounce last month but fell back 8.3% in. Meanwhile the Westpac Melbourne Institute House Price Expectations Index has shown opposite moves over the last two months with a sharp 11.1% fall in June followed by a 12.1% rebound in July. Both Indexes are down sharply from the highs late last year and are pointing to a housing market slowdown, although the extent to which price growth and demand softens is clearly uncertain.

Overall a solid recovery in confidence is still the most likely prospect over the course of 2014 as concerns over the Budget gradually fade. We expect that high savings rates; strengthening household balance sheets; and a surge in residential building will all support a solid lift in spending as the recovery in consumer confidence comes through.

The Reserve Bank board meets on August 5. Barring any unexpected economic shocks the Board is certain to hold rates steady. However, markets have responded to the weak run in data and confidence by now pricing in a 50% probability of a rate cut by early next year. That stands in contrast with our own forecast of a rate hike by the September quarter next year. Clearly the issue for rates will be the prospects for the consumer over the course of 2014.

Ongoing weakness in the consumer is likely to see businesses scaling back investment and employment plans. Equally, a resumption of the solid trends in consumer spending that we saw through the second half of 2013 and into 2014 will boost investment and employment plans from business. The slowdown in retail sales and housing markets suggests the recent weakness in the sentiment is already affecting activity to some extent.

In this note we have indicated an expectation that confidence will recover through 2014 as anxieties around the Budget ease. In time, those trends, along with a gradually improving global economy will lay the foundation for higher rates later in 2015. Westpac expects rates to remain on hold for the next year or so prior to a first hike in August next year.

I was expecting a better bounce too. I no longer think it’s coming unless Clive Palmer can unwind the Budget completely. Even then I expect the grind higher will be slow. Faith in the government and its solutions for the last few year’s of household’s struggle has been shattered.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.