HSBC’s Paul Bloxham has nice report out today looking at the Asian integration trends that are a “key reason for our continued optimism about Australia’s growth prospects”:

- In the past six years, Australia’s economy has grown 16%. By comparison, the US has grown 6%, while the British economy has not grown at all and Europe’s is 2% smaller. China’s economy has grown by 65%.

- No other OECD economy has a larger export exposure to Asia than Australia and the largest part of this is to China.

- Around 73% of Australia’s exports go to Asia, and we expect this to rise to 80% by 2020e.

- Three Asian economies alone – China, Japan and Korea – account for 54% of Australia’s exports.

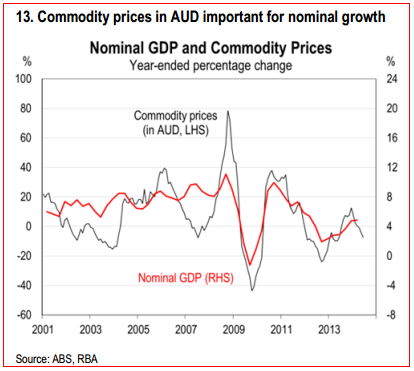

- Much of what Australia exports are commodities, which account for 57% of total exports.

- Over the next six years the value of iron ore exports is expected to rise 54%, coal by 41% and LNG by 330%, as newly built capacity comes on line.

- Other goods and services account for 40% of Australia’s exports, which include agricultural

- products, manufactured goods, and tourism and education services.

- Chinese tourist visits to Australia have increased by 110% in the past four years.

- 28% of Australia’s population was born outside the country.

- Of the more than 5m foreign-born individuals living in Australia, 2m were born in Asia.

- Thanks to strong migration, Australia’s population growth has averaged 1.4% y-o-y over the past decade, compared to an average of +0.7% y-o-y amongst the OECD economies.

- Australia’s financial ties are still mainly to Western markets, with 56% of FDI and 57% of ODI with the US and Europe, although links to Asia are growing.

This is all fair enough and Bloxo is right that our Asian proximity is a huge opportunity. Strip this report back, however, and what you find is the usual material, dressed up in a pleasant vision of Asian engagement. For instance:

- Australian exports to Asia are completely dominated by primary materials

- manufacturing is shrinking and Australian services don’t invest in Asia, meaning that education and tourism is all that is left

- incoming investment remains primary material oriented. Other forms, such as property, have deep political consequences that touch upon the still dominant person-to-person failure to integrate;

- the Australian population tolerates not embraces higher Asian immigration and is kept in that state by a political elite that balances targeted integration with xenophobic reassurances and a strategic commitment to the United States.

In realty, Australia’s Asian integration is far less widespread than Bloxo suggests. It is highly targeted and politically fraught, surprisingly shallow given the mutual dependence and will eventually founder on strategic competition.

None of that is say that Bloxo’s opportunity isn’t real, it is, but the most likely outcome is an ongoing suspicion that leaves us very much dependent upon resources as the key plank in the relationship. As such, the best chart in the pack is this one:

Given commodity prices will likely fall right through to 2020, that looks like a long and difficult decline ahead in nominal growth, because of the peculiarities of Asian engagement. As MB keeps saying, GDP may look OK but it won’t feel very good as Australian standards of living keep falling.

Full report here.