Geopolitical tensions and continued supply outages in the Middle East prompted a spike in Brent oil to USD115.71/bbl in June, a nine-month high. Half of the world’s oil is consumed in Asia (including Australasia).

Furthermore, Asia consumes 76% of the Middle East’s oil exports, compared with just over 10% for both Europe and the US. Figure 1 clearly illustrates that Asia is much more exposed to any disruption to oil supplies in the Middle East than anywhere else in the world. Within Asia, oil dependence varies markedly, however. We look at the winners and losers of a supply side oil price shock among Asian currencies.

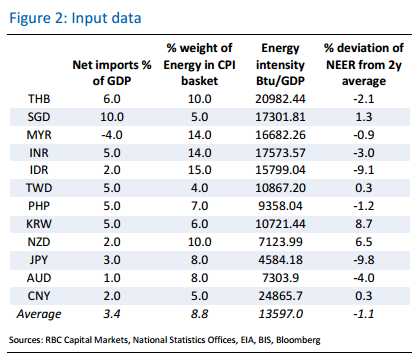

Typically, such analysis tends to only consider whether an economy is a net oil importer or net oil exporter, but there are additional factors that impact the extent of an economy’s sensitivity to oil price volatility. Some important factors to also take into account are:

(1) The domestic oil production-consumption ratio;

(2) The pass-through into inflation; and

(3) Whether the exchange rate is appreciating or depreciating.

Why do these factors matter?

(1) The domestic oil production-consumption ratio. A mismatch between domestic crude production and imports can impact an economy’s import bill and the size of its trade deficit. The lower the ratio of imported crude to total consumption, the better it is.

Energy intensity is a measure of the energy efficiency, calculated as units of energy per unit of GDP. High energy intensity indicates a high price or cost of converting energy into GDP. The lower the energy intensity, the better it is.

(2) The extent of inflation pass-through from higher oil prices. This represents the inflationary threat. Inflation is directly influenced through the weight of oil products in the CPI basket. The lower the weight, the less sensitive an economy is likely to be to higher oil prices.

(3) A rising (nominal) effective exchange rate will offset both (1) and (2) to a certain extent as the purchasing power of domestic income over imported goods rises.

Australia is definitely well placed in isolation but if Asia is hit hard then there will be flow though to our export demand.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.