From Westpac comes the below analysis of today’s TD Securities/Melbourne Institute (MI) Inflation Gauge for May, which is pointing to rising inflationary pressures:

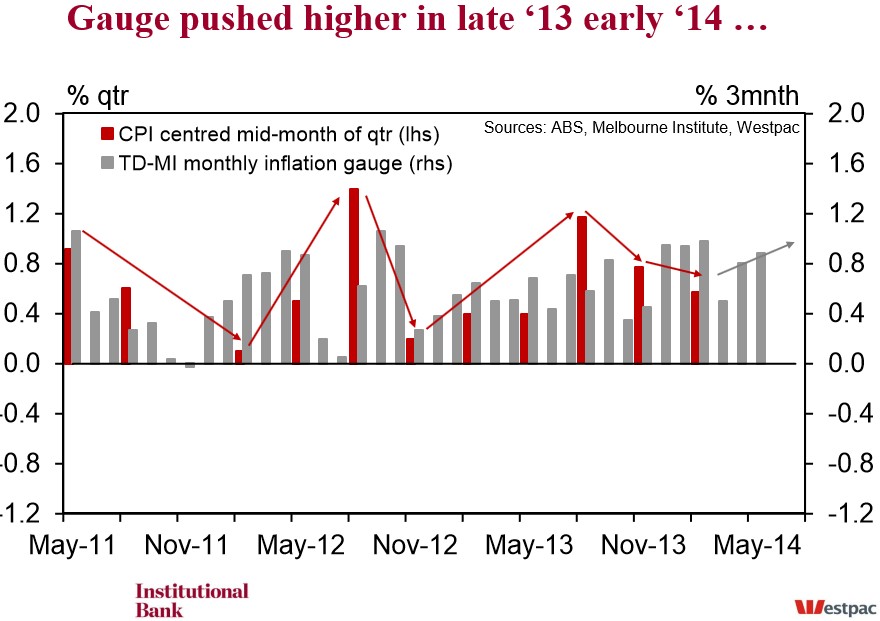

The Gauge rose 0.3% in May following 0.4% increase in Apr and a 0.2% rise in Mar and Feb. The annual pace has accelerated to 2.9%yr from 2.8%yr in Apr, continuing to build on the reported 2.5%yr pace in Jan. The most recent low was 2.1%yr in Oct 2013.

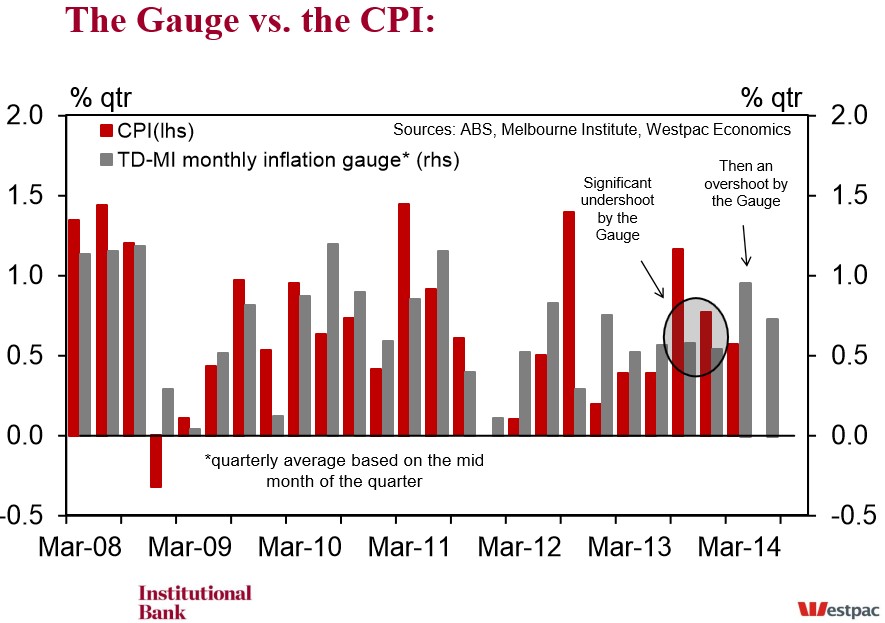

The Gauge is now well into the upper half of the RBA’s inflation target band and threatening to breach it. Westpac had been forecasting inflation to pick up in late 2013/early 2014 but this gathering momentum is something to watch closely.

The annualised three monthly pace had dropped to 2.0% in Mar, from 4.0% in Feb and 3.8% in Jan. However since then, it has accelerated again to 3.2% in Apr and now 3.6% in May. Westpac estimates there is no significant or reportable seasonal effect in May.

The trimmed mean of the Gauge rose by 0.2% in May, following an increase of 0.5% in Apr. In the three months to May, the trimmed mean increased by 0.8%, a similar rise for the three months to April. In the year May, the trimmed mean rose 2.9%.

TD-MI reports that contributing to the overall change in May were price rises for fruit & vegetables (6.1%), furniture & furnishings (4.0%) and tobacco (2.3%). Partially offsetting this was holiday travel & accommodation (–3.7%), health (–0.8%), and footwear (–0.9%). Automotive fuel prices fell 1.1% in May.

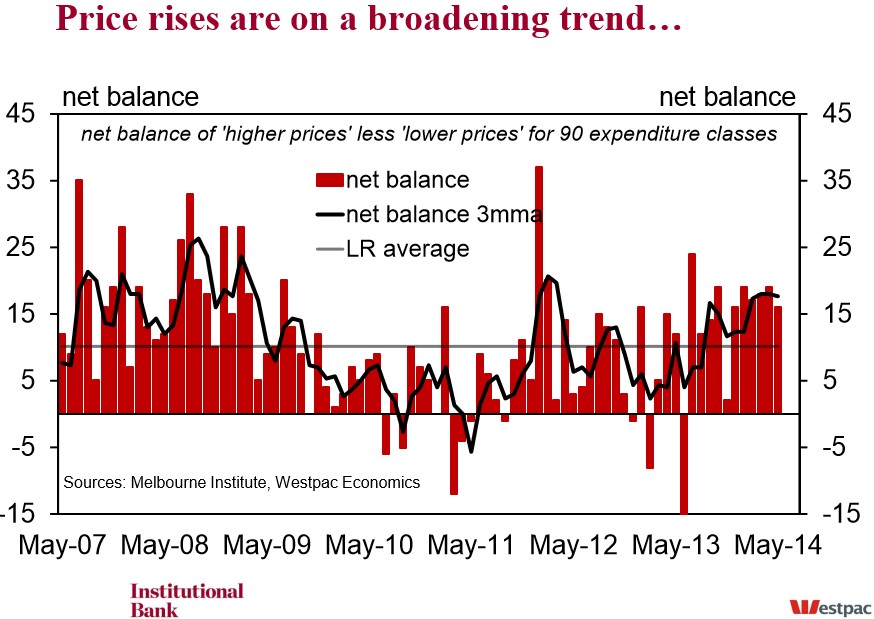

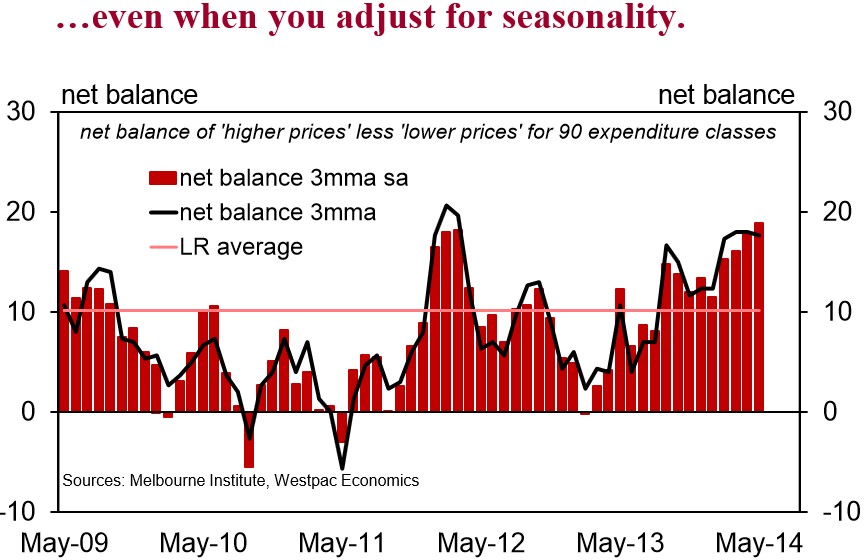

The net balance (number of price rises less number of price falls) did moderate to 16 in May from 19 in Apr and 18 in Mar. Nevertheless, it is still above the long run average of 10 and the 2013 average of 9. Westpac estimates a negative seasonality in May, the adjusted net balance was 19 in May compared to 18 in Apr.

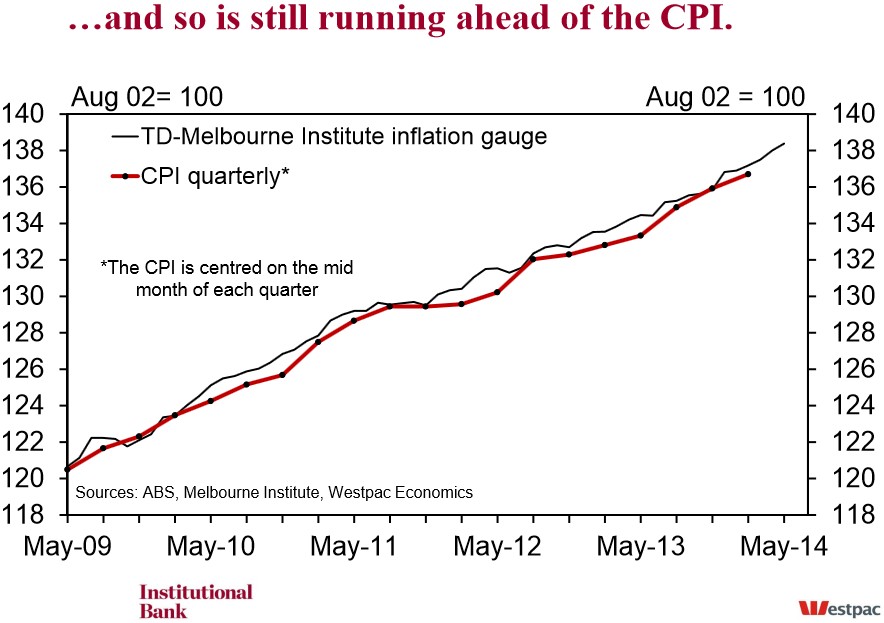

The Q2 CPI surprised with a modest 0.6%qtr and as such, left the Gauge tracking well ahead of it. The May Gauge report suggests this momentum continues which, if history repeats, points to some near term upside risks via a short-term “catch-up” by the CPI.

Westpac is currently conducting a full review of the Q2 CPI forecast. As it stands, our forecast is for a 0.5%qtr rise.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.