I noted on Tuesday how the Western Australian Government’s iron ore forecasts were far too optimistic, and risked blowing a big hole in the state Budget.

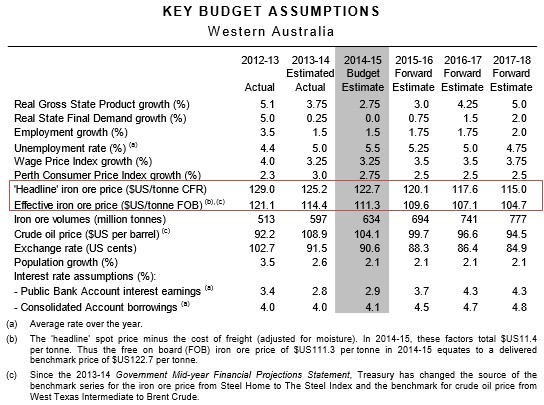

The problem is highlighted in the below table taken from the Budget papers, which shows a forecast spot price of $122.70 over 2014-15, and only minor downward adjustments in the out years:

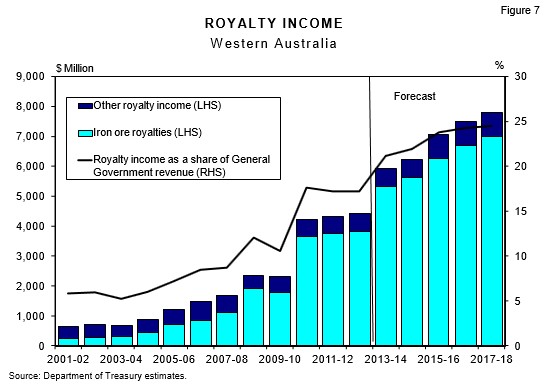

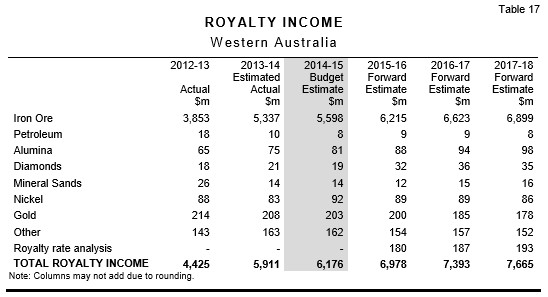

When combined with surging iron ore volumes – which may also prove heroic in the face of lower than forecast steel demand from China – Western Australia has forecast massive growth in royalty revenue, both in absolute terms and as a share of total revenue (see below chart and table).

Yet, in the face of an iron ore price that has slumped to under $US95 a tonne, the Western Australian Government is clinging to its optimistic view, sticking to Treasury’s bullish price forecast and predicting a strong rebound:

While WA Opposition Leader Mark McGowan has called on the state government “to provide a full explanation” as to why its projections are higher than those of analysts, Treasurer Mike Nahan says treasury estimates are credible and there is no reason to panic…

“It varies quite a bit”…

“We’re not trying to predict the variations in it – we’re looking at the long haul”.

“You just have to hold your nerve on these issues. There is volatility in this”.

“If we react to every downward trend by immediately taking drastic actions, we could not govern well”.

“I’m not going to slam on the brakes in any way.”

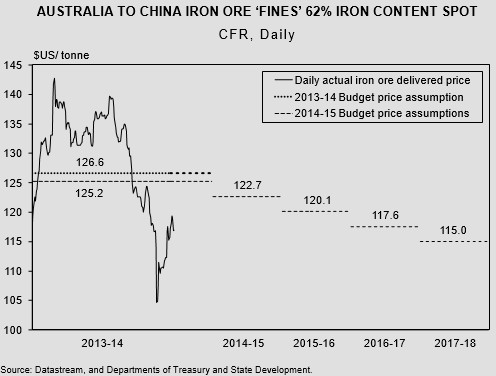

While it makes sense not to react to short-term price movements, ignoring the structural adjustment underway in the iron ore market (i.e. rapidly rising supply in the face of sluggish demand growth), and clinging to Treasury’s bullish 2014-15 forecast and gentle moderation in price over subsequent years (see next chart) makes absolutely no sense. The Treasury has misread the market dynamics, pure and simple.

The Government would appear far more credible if it just admitted that its price forecasts are too optimistic, and undertake to provide new forecasts and revised revenue projections by some future date.

It should also enunciate that the Budget has a built-in safeguard – namely that the state’s GST share will likely be adjusted upwards to compensate for the falling mining royalties.

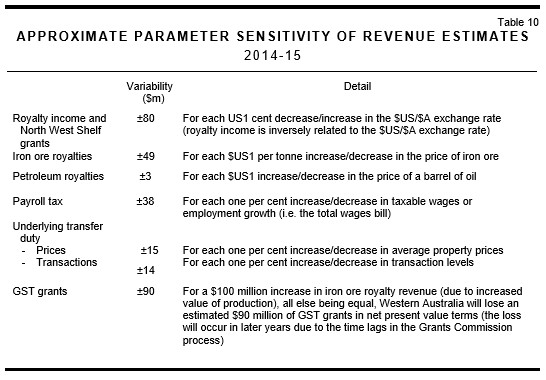

Indeed, while the sensitivity analysis contained in the Budget papers noted that every $US1 fall in the iron ore price reduces Budget revenues by some $49 million, it also stated that GST grants would be adjusted upwards to cover 90% of the lost revenue (see below table).

Hence, in reality, most of the Budget pain from the falling iron ore price will likely be borne by all of Australia’s state and territory governments via reduced GST payments. This is the message that the Western Australian Government should convey.