Stephen Koukoulas (“the Kouk”) has today continued his shift into bear territory, arguing via his blog that the Australian economy is slowing and moving to an easing bias on interest rates:

It is staggering the slowdown in the Australian economy that is unfolding before our eyes.

I was slow to realise this, but the recent run of news has now converted me to interest rates on hold with a renewed bias to cut and I am now bearish on the Australian dollar. Indeed, a couple of low inflation numbers, a faltering GDP growth rate through to the September quarter and a touch more downside on commodity prices will likely see the RBA cut interest rates.

So there.

Here is what I am now seeing. In the last month or two, some slightly disconcerting signs have emerged about the pace of economic growth with a number of key economic indicators stalling or indeed, reversing.

The Kouk then provides a useful breakdown of “some important (and not so important) indicators for the economy which suggest that growth may be faltering” (read here), and concludes with the following:

Sure, some of these trends may be temporary, there could be noise in the data, or there may be unusual seasonal patterns or something else that will prove to be temporary. Let’s hope so and the path to 3 per cent plus GDP is maintained.But as I crunch the numbers taking account of the new news, it is getting harder to see that strong growth momentum in the first quarter of 2014 being sustained.

I obviously agree with the Kouk’s sentiments. However, I am less concerned about headline GDP growth and more concerned about national income, gross national expenditure (GNE), and domestic final demand (DFD).

As noted last week, I do not consider GDP to be a particularly useful tool to gauge the economy’s underlying strength or the wellbeing of the Australian people.

In particular, headline GDP is only concerned with the volumes of goods and services produced and completely ignores prices. Yet, the growing export volumes have occurred (and will continue to occur) in concert with falling export prices, which means that actual national income – a far more important measure of welfare – will rise far more slowly than the growth in GDP.

The below stylised example of iron ore exports, which we have used previously at MB, highlights the point more clearly, and shows that even if volumes rise by the same amount that prices fall, the end result for Australia is still much worse:

- assumed an average cost of production of $60 per tonne

- 2013 average iron ore price price: $130 per tonne

- 2013 volume (example only) 500 million tonnes

- Total profits: $35 billion

Assume in 2014:

- export volumes grow 20% to 600 million tonnes

- average iron ore price falls 20% to $104 per tonne

- Average cost of production still $60 per tonne

- Total profits = $26.4 billion

Under this example, despite volume growth fully offsetting price falls, profits from iron ore exports actually fall by $8.6 billion (24.5%), other things equal.

Again, real (headline) GDP, which only measures volumes, would record big gains under the above scenario, whereas national disposable income – the more important metric – would record a fall.

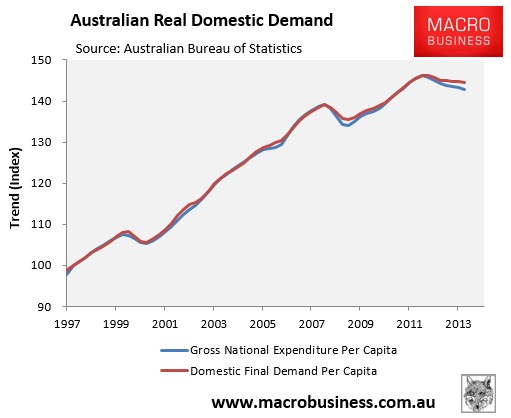

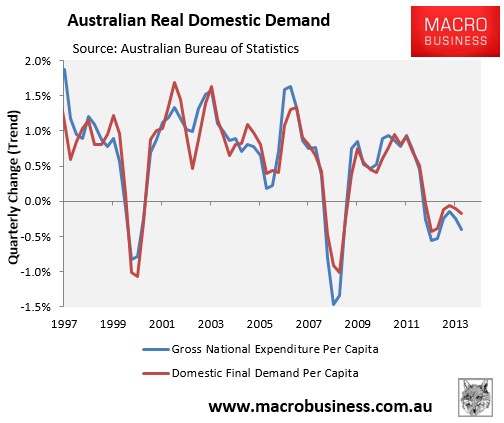

Moreover, as highlighted in another article last week, per capita GNE and DFD have also been falling, suggesting the domestic economy remains weak, propped-up by both strong immigration and rising export volumes (see below charts).

These small differences aside, the Kouk is right to be concerned.