By Chris Becker

The re-education of the Australian community of sell-side analysts, investors, and bureaucrats – that commodity booms always end with busts – continues with iron ore.

Let us further the education and see what happens on the periphery, not just the travails of the underlying price of a commodity, but rather the stock price performance of the miners themselves.

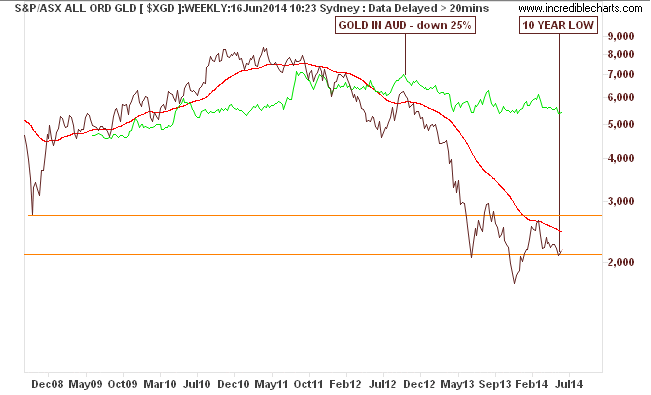

A fantastic comparison can be seen with gold which had its own “super-boom” in the 2000’s before the so-called safe haven was abandoned towards the end of 2011. Whilst gold, priced in Australian dollars, has only fallen some 25% and has remained range-bound for over a year, the All Ords Gold Index (effectively Newcrest Mining (NCM) which has sucked up all of the other major listed players) has declined nearly 70%:

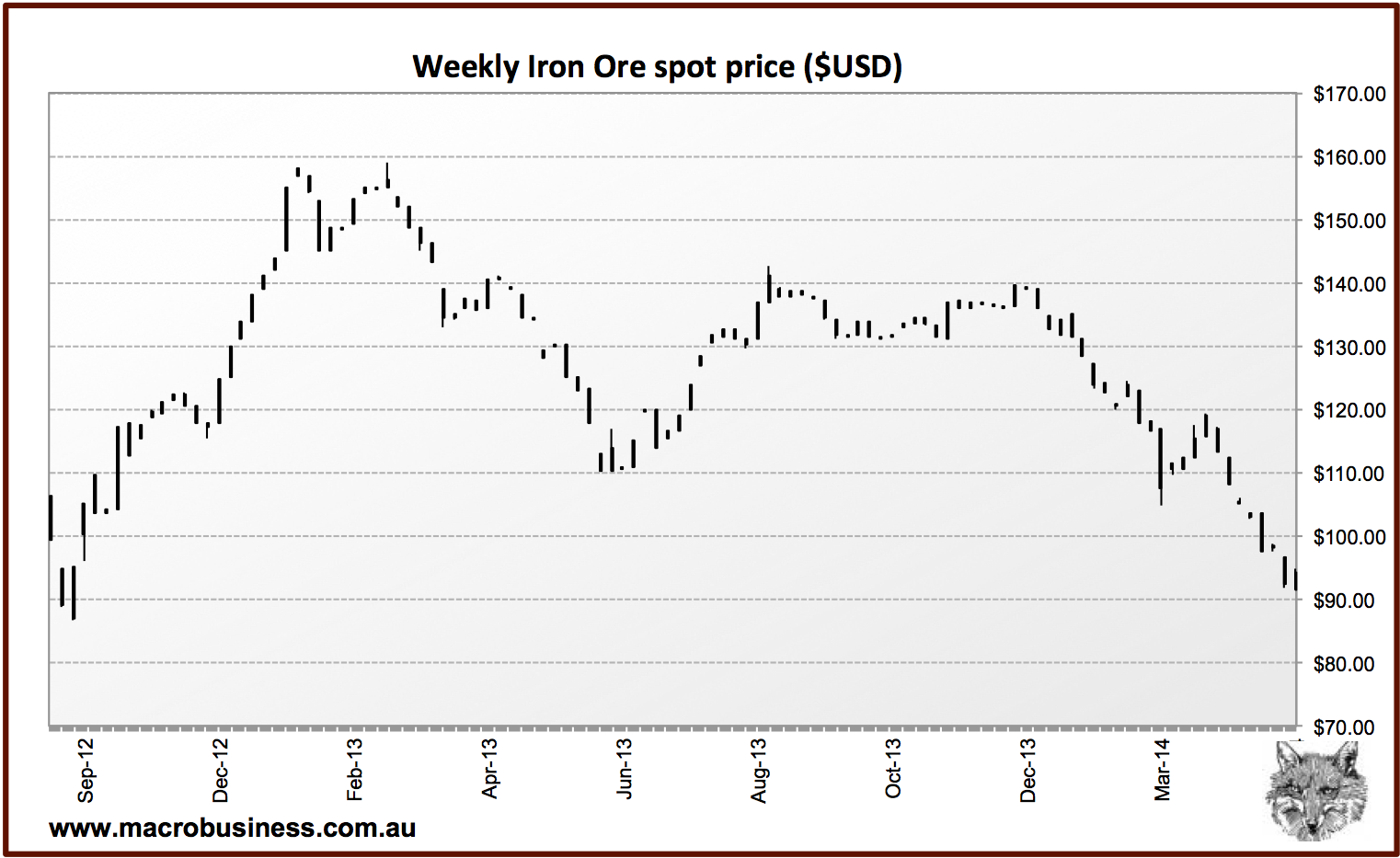

So far we’ve seen spot iron ore fall nearly 40% from its recent high (ca. $153 to $91):

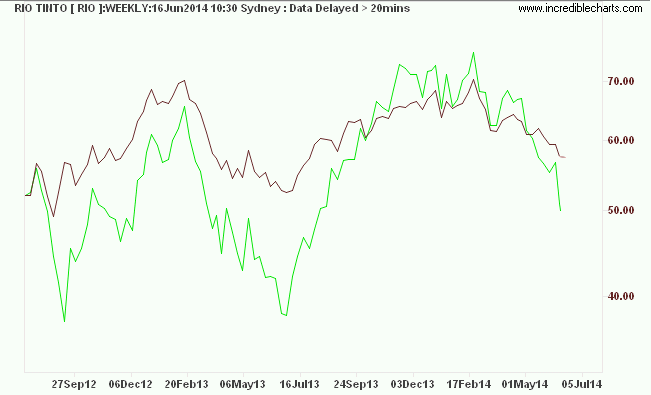

Yet the iron ore “index” – let’s say Fortescue (FMG) and Rio Tinto (RIO) – have only fallen ca. 33% and 20% respectively:

Of course the juniors are tumbling even faster as their cost margins are much tighter: e.g. Atlas Iron (AGO) – down over 50%, Mt Gibson Iron (MGX) – down over 40%, just like gold miners, all iron ore stocks – senior and junior – are likely to accelerate there falls from here on in.

The lesson here: don’t be fooled into a linear relationship between a commodity price and the underlying mining stock.

Whilst the quick-footed few maybe able to make good on the inevitable dead cat bounces that regularly occur in terminal declines (Newcrest went up 70% in a recent counter-rally before resuming its decline), the best risk to take is to stand aside as the storm passes.