Super Retail cut profit guidance to $107 million from a consensus around $115 million because:

“This reflects the significant downturn in consumer confidence since the federal budget, particularly across the lower to mid income families who represent core customers.”

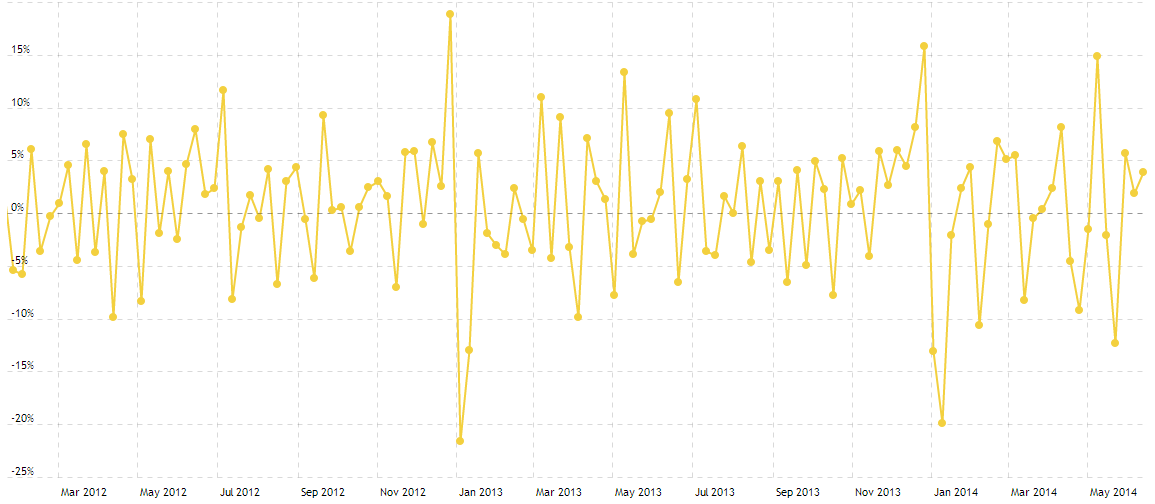

No new fluffy dice this year! The BDO fast retail index also continues to show shoppers tracking at around the pace of last year’s subdued second half after the early year splurge:

I’d say it’s an enduring shunt lower. Goldman agreed in its morning note:

Stay underweight consumer-exposed names; improved valuation support, but an FY15 sales recovery is unlikely in our view

- Profit warnings across a number of retailnames have put the sector back in focus.

- Bottom-up consensus expects the Consumer Discretionary sector to see a strong recovery next year with EPS growth accelerating from 3%/4% in FY13/FY14 to 13% in FY15 driven by a near doubling of sales growth (4% in F14 to 13% in FY15) and 50bps of EBITDA margin expansion.

- Given poor wage growth dynamics and severe fiscal contraction (tax increases,cuts in welfare payments in FY15) these forecasts continue to look overly optimistic to us. Despite increased valuation supportwe remain underweight the sector.

As I said early this year in my Dutch disease and asset allocation dissertation, discretionary retail is a trap in this cycle.