For those in the know, Westpac’s Red Book is the bible of Australian consumer attitudes. The June edition executive summary follows:

The Westpac–Melbourne Institute Index of Consumer Sentiment rose 0.2% in Jun, essentially stabilising after the sharp post-Budget decline in May. At 93.2 the Index remains lodged firmly in pessimistic territory.

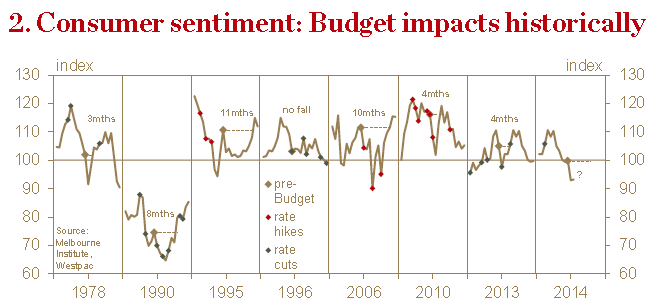

― The absence of a significant rebound from May’s sharp fall is disappointing. However, Budget impacts historically have often seen slow recoveries, with other factors such as interest rate moves often having a major bearing on the path of sentiment.

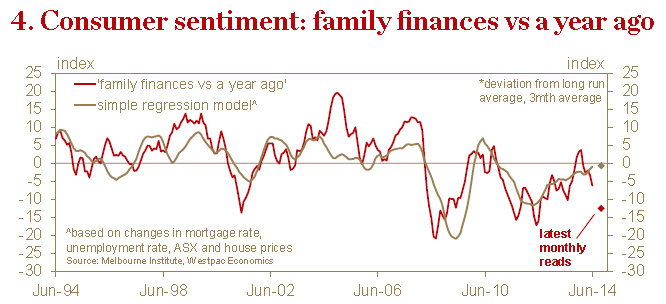

― Views on family finances remain particularly weak, with the sub-index tracking expectations for ‘family finances, next 12mths’ recovering just 5% from May’s alarming 23% slump and still the second lowest reading since the early 1990s.

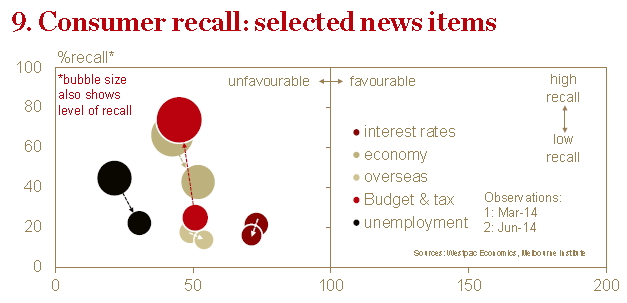

― Additional questions on news recall highlight the dominance of ‘Budget and tax’ issues, with record high levels of recall on this topic easily surpassing previous highs during the mining tax debate, the GST introduction and other major Budget events. News in general continued to be viewed as unfavourable.

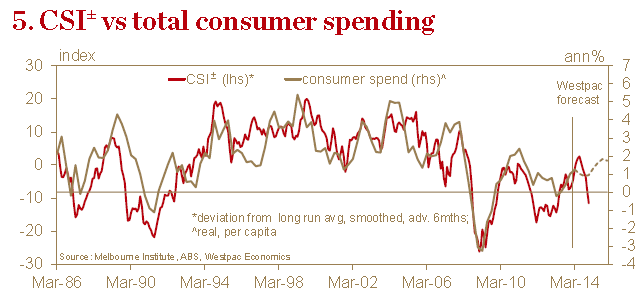

― CSI±, our modified sentiment indicator that we favour as a guide to actual spending, also posted a muted 0.2% recovery in Jun and is down 14% from its Nov high. Current readings are consistent with a slowdown in consumer spending growth from 2.8% in Q1 to around 1%yr by Q4.

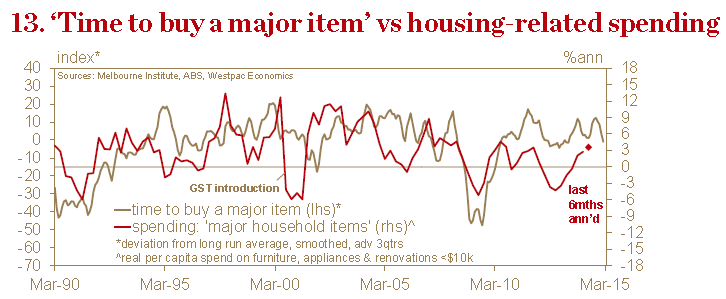

― The sub-index on ‘time to buy a major item’ has been much more resilient in recent months, edging up a further 1% in Jun. Readings suggest spending on durables and cars should hold up reasonably well.

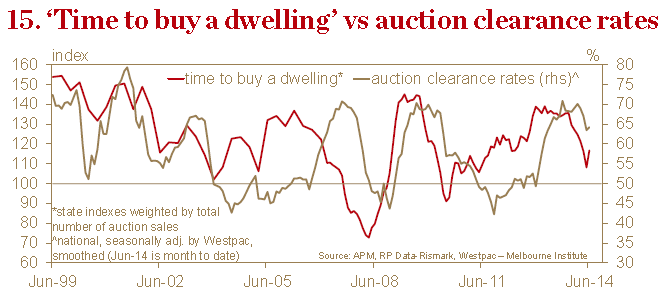

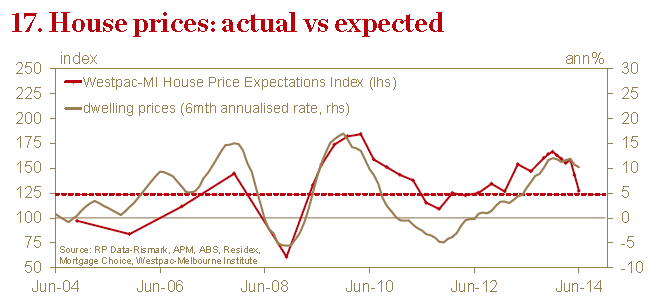

― Consumer views on housing showed an intriguing shift in Jun. The ‘time to buy a dwelling’ index rebounded sharply, reversing much of the sharp slide in the previous 3mths. However consumers also significantly marked down expectations for prices. The Westpac Melbourne Institute House Price Expectations Index fell a further 11.1% in June after a 9.8% decline in May. The combined message points to a somewhat softer landing in housing markets with finance approvals flattening out and price growth slowing to around 5%yr.

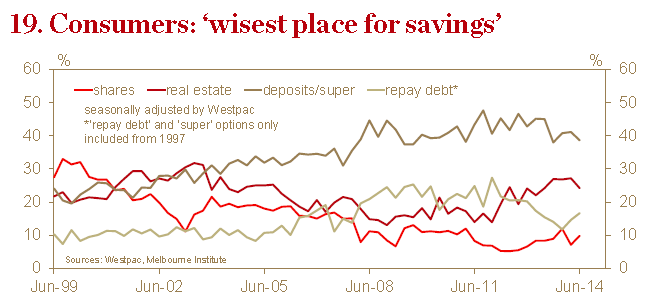

― The Jun survey included an update of questions on the ‘wisest place for savings’ used to construct the Westpac Consumer Risk Aversion Index. The results show little change, with a very slight tilt towards risk aversion following a bigger rise in Mar. Attitudes are still much more relaxed than in early 2013.

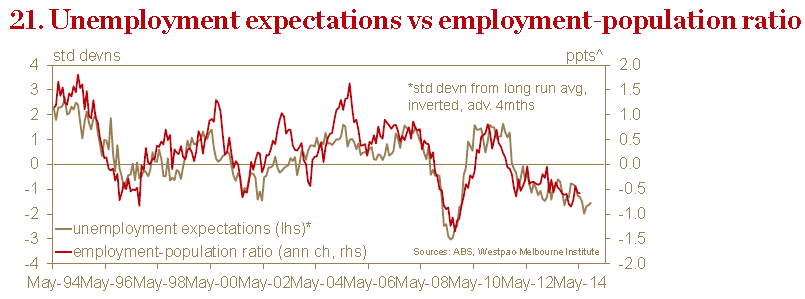

― The Westpac-Melbourne Institute Unemployment Expectations Index registered a marginal decline, falling 1.1% from 158.3 to 156.5. That is a significant improvement on the peak in unemployment fears back in Mar, when the index hit 164.4, but still significantly ‘worse’ than the 144.7 reading in Nov (recall that higher readings mean more consumers expect unemployment to rise over the next year).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.