Business Spectator’s Callam Pickering has written a good article today embracing MB’s long-held view that Australia’s obsession with housing, along with rampant immigration, is distorting the Australian economy, and risks lowering productivity and the nation’s living standards:

While businesses can borrow more to innovate, expand, acquire other companies or increase output, household lending typically result in simply paying more for an asset. Housing loans chase other housing loans – which is great for real estate agents and property developers but of little benefit to Australians or the businesses that employ them.

In addition, lending to the housing sector has effectively pushed land prices so high than many Australian firms struggle to contain costs or compete effectively against international players. Our wages may be high by international standards but land prices represent one of the major differences between Australian firms and their international competition…

Our national economic plan mostly involves a mixture of mining, house prices and immigration… The first has diminished, the second reduces productivity and business competitiveness, and the third is not an economic plan at all…

Instead we need a plan that puts productivity at the forefront, supports small businesses and encourages them to take risks and innovate. We need a plan that is based around improving our living standards rather than creating the illusion of growth. We need a plan that encourages resources to be allocated to where they can do the most good rather simply indebting a generation of Australians.

Callam touches on many issues that are at the heart of Australia’s politico-housing complex, and were a key pillar of MB’s presentation to APRA last week.

In a nutshell, resource allocation has for decades been channeled away from the tradable sector and infrastructure investment towards the financial sector, as home buyers have taken on ever-bigger mortgages as they chased house prices higher.

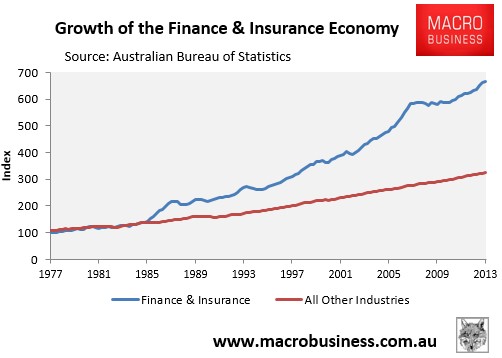

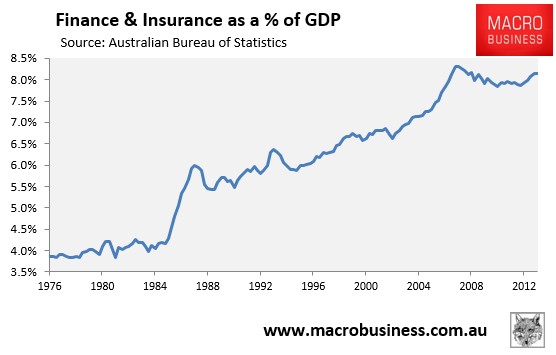

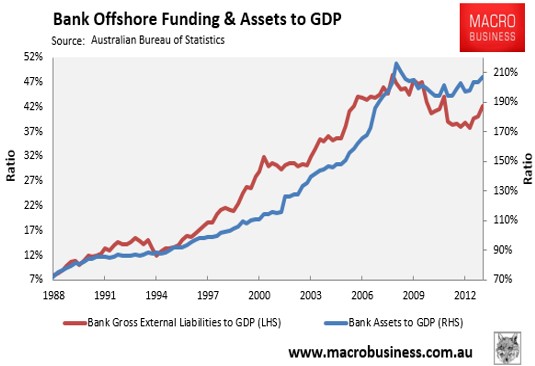

Since financial markets were deregulated in the mid-1980s, the finance and insurance industries – which are dominated by mortgage lending – have grown at more than twice the pace of the rest of the economy, due in part to the housing quango operated by the various levels of government (see below charts).

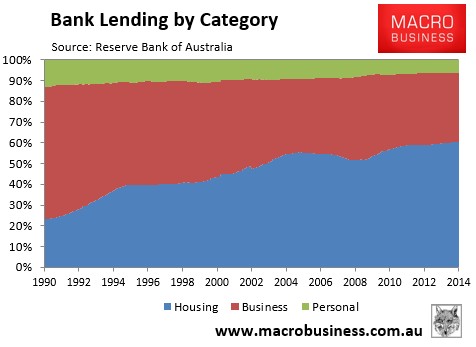

In turn, Australia’s housing obsession has starved productive sectors of the economy of credit. In the early 1990s, Australia’s banks lent nearly two-thirds to businesses, with the balance split between housing and personal lending. However, after the mid-1990s explosion of housing values, these ratios have reversed, with housing lending dominating at the expense of businesses (see next chart).

To add insult to injury, much of the boom in mortgage lending has been funded by heavy offshore borrowing by Australia’s banks, in turn driving-up Australia’s net foreign debt:

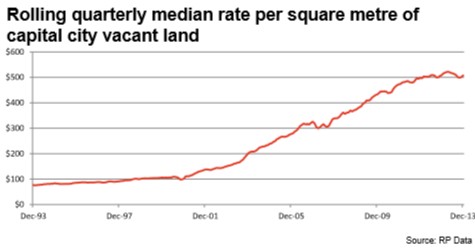

Central to the problem are Australia’s unique mix of tax concessions, such as negative gearing, and the constipated supply system. The former has increased the relative attractiveness of housing investment, boosting demand, whereas the latter has materially dampened the supply response. The end result has been escalating urban land prices, which according to RP Data has increased 564% over the past two decades:

Indeed, fellow MB blogger, Cameron Murray, has estimated that a considerable slice of Australia’s declining multi-factor productivity has resulted from escalating land prices.

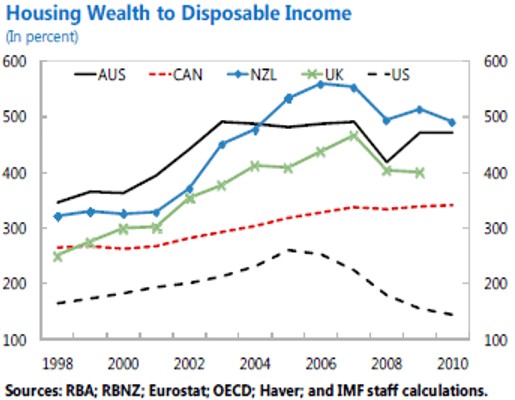

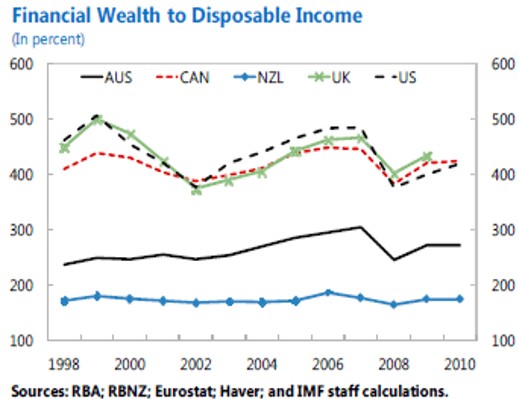

It has also meant that too much of Australia’s capital/wealth has been tied-up in housing, as illustrated by the below charts from the IMF (note: New Zealand shares essentially the same banking system as Australia):

Combined, Australia’s politico-housing complex has chocked-off productive areas of the economy, whilst leaving Australian households – particularly those that arrived late to the party (i.e. the younger generations) – drowning in debt.

Australia’s world-beating immigration program is of course the final ingredient that has contributed to the illusion of growth. Despite dubious economic arguments in favour of high immigration, Australia’s intake was ramped-up significantly in the mid-2000s, further increasing demand for housing in the face of choked supply, diluting our fixed endowment of minerals resources, heightening infrastructure bottlenecks, and arguably failing to raise the living standards of the existing population.

One can only wonder how Australia would have looked if the billions of dollars of excess capital that had been poured into pre-existing housing had instead been funneled into businesses and infrastructure, as occurs in places like Germany. Instead, Australia has been left with non-mining companies that are struggling to compete and an infrastructure deficit that former Treasury secretary, Ken Henry, has claimed is hindering Australia’s ability to provide goods to Asia.

As argued by Callam, Australian policy must become focused on raising productivity and boosting Australia’s international competitiveness. This requires changing the tax system so that it rewards productive investment, a wide-spread program of micro-economic (structural reform), as well as liberalising the myriad of constraints on land supply and planning that have forced-up urban land prices, raising business costs and wages.