From Forexlive, Joe Hockey is quoted as saying about today’s GDP figures that:

- Says transition from mining is underway

- Says Australian economy is resilient

- Says iron ore prices lower than expected in budget

- Says investment in housing is positive

- He is confident will see business investment outside mining

I’m not sure which economy he’s looking at but it’s not Australia’s. From JP Morgan’s Stephen Walters:

Aussie GDP – growth is good … but it is anything but balanced

Today’s 1Q GDP report delivered an upside surprise on the headline growth figure, but the underlying details were much less impressive. Net exports bounced in line with expectations (consistent with yesterday’s published data) and growth in dwelling investment beat expectations but, outside mining, conditions remain pretty soggy. Household spending growth, for example, was weak (the elevated savings rate was unchanged last quarter), and government investment slumped. Growth is good, but it is anything but balanced.

Indeed, the GDP report showed that one rotation in the sources of growth in the economy is progressing nicely, the other not so well. In fact, the transition from mining investment to higher export volumes is going swimmingly – net exports soared last quarter, as resource sector investment fell away. The other much-needed rotation, however – in the drivers of domestic demand – remains a work in progress. GNE slipped another 0.3%q/q in 1Q and domestic demand (i.e. after adjusting for the large fall in inventories), rose only 0.3%q/q, after an even less impressive gain in the December quarter.

Still, the headline growth outcome looks decent enough. GDP expanded 1.1%q/q (J.P. Morgan 0.7%q/q, consensus 0.9%), which lifted growth over the year to 3.5%oya. This is a step up from the 2.7%oya rate of growth in the previous quarter, and is the fastest annual rate of expansion since 2Q 2012. Closer examination, though, shows that without the surge in export volumes, the rest of the economy would have barely been growing – annual GNE growth now has been less than 1% for five straight quarters.

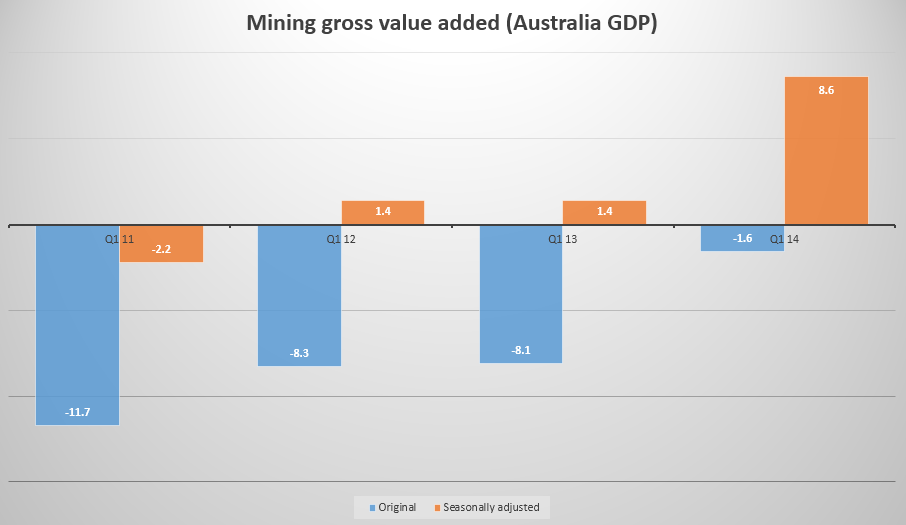

By industry, unsurprisingly, the biggest lift in output in the March quarter was in mining, which soared nearly 9% over the quarter, adding 0.9% points to the expansion in GDP. Other decent gains were in construction, accommodation, financial services, and real estate. Manufacturing output tumbled more than 3% over the quarter, and farm output also slipped. The messages here are consistent with the longer term narrative of the mining sector doing very well, other sectors slowly adjusting, and the industrial sector continuing to dwindle.

The bounce in net exports owed much to higher export volumes. Total export volumes surged an impressive 4.8%q/q, the biggest gain since 2000, and there was a 1.4%q/q fall in imports as the peak in mining investment, which is heavily import intensive, passed by. The net exports gain last quarter was the best since early 2009, but that result owed much to a slump in imports as the great recession worsened. Net exports now have been positive for the last two years.

Household spending grew only 0.5%q/q last quarter, much weaker than growth in the previous quarter, but we know there is more softness on the way. Retailers have reported that the unseasonably warm weather has depressed sales of apparel and footwear, and there has been a post-budget slump in consumer sentiment, which we expect to be a headwind for spending. Consumers already are cautious – the savings rate stayed high at 9.7%, albeit well below the peak of nearly 13% in 2009.

Business investment slipped slightly last quarter, albeit by less than we had expected, as miners cut back and there was insufficient lift elsewhere. Last week’s investment report at least showed there is modest improvement in that regard on the way. There was unexpected strength in dwelling investment, though, which bounced nearly 5% over the quarter.

Public spending was subdued last quarter, as RBA officials have been indicating. Government investment dived 5%q/q. We know there is a material rise in state government funded infrastructure spending on the way, financed largely by asset sales, and the recent federal budget announced new road funding. Outside these areas, though, government spending will be a drag on GDP growth, even if the government fails to have all of the budget measures passed by the Parliament.

Price pressures in the economy were a little elevated relative to reported inflation, with the deflator for household spending, for example, rising 0.8%q/q, compared with the CPI outcome of 0.6%. The current mix of growth, though, with household spending weak, implies price pressures in the economy should be subdued from here. The terms of trade dropped 1.2%q/q, reversing the rise in the previous quarter, but the fall extends the correction from the elevated peaks reached back in late 2011.

The FT, meanwhile, notes that some of the huge growth in exports was due to the good weather over the cyclone season. Here is the chart to prove it:

It’s a ripping one quarter result but shows rebalancing is lagging badly.